Why AI Fails in Banks; Examining Card Issuing Value Chains in the UK; Agentic Payments Impact on the Pass-through Payment Model

Video of the Week

Deep Dive of the Week

Unwrapping FIS’s Technology Stack and Architecture

FIS is building a banking platform that treats the bank like a set of interoperable services, not a monolithic core. The stack is structured in layers: cloud-native infrastructure, a common data and AI layer, componentized product modules, and a unified API access layer that abstracts the underlying cores. The architectural goal is simple: decouple channels from processing, decouple products from the core, and make integration the default state. If you want to understand where FIS is going, ignore product names and follow the mechanics: a universal ledger and orchestration layer, reusable platform services for account opening and money movement, a marketplace for third parties, and delivery tooling designed to ship changes safely at a global scale.

This week’s reports

2️⃣𝐏𝐚𝐲𝐦𝐞𝐧𝐭 𝐭𝐫𝐞𝐧𝐝𝐬 𝐚𝐧𝐝 𝐢𝐧𝐬𝐢𝐠𝐡𝐭𝐬 𝐟𝐨𝐫 𝟐𝟎𝟐𝟔 𝐛𝐲 𝐃𝐞𝐥𝐨𝐢𝐭𝐭𝐞

3️⃣𝐓𝐡𝐞 𝟐𝟎𝟐𝟔 𝐀𝐈 𝐗 𝐁𝐥𝐨𝐜𝐤𝐜𝐡𝐚𝐢𝐧 𝐜𝐨𝐧𝐯𝐞𝐫𝐠𝐞𝐧𝐜𝐞 𝐫𝐞𝐩𝐨𝐫𝐭

4️⃣𝐇𝐨𝐰 𝐛𝐚𝐧𝐤𝐬 𝐜𝐚𝐧 𝐦𝐞𝐚𝐬𝐮𝐫𝐞 𝐀𝐈 𝐢𝐧𝐯𝐞𝐬𝐭𝐦𝐞𝐧𝐭 𝐬𝐮𝐜𝐜𝐞𝐬𝐬

5️⃣𝐅𝐢𝐯𝐞 𝐌𝐲𝐭𝐡𝐬 𝐀𝐛𝐨𝐮𝐭 𝐄𝐦𝐛𝐞𝐝𝐝𝐞𝐝 𝐅𝐢𝐧𝐚𝐧𝐜𝐞 𝐢𝐧 𝐏𝐫𝐨𝐜𝐮𝐫𝐞𝐦𝐞𝐧𝐭

6️⃣𝐀 𝐑𝐞𝐚𝐥𝐢𝐭𝐲 𝐂𝐡𝐞𝐜𝐤 𝐟𝐨𝐫 𝐂𝐅𝐎 𝐒𝐭𝐚𝐜𝐤 𝐅𝐢𝐧𝐭𝐞𝐜𝐡𝐬

7️⃣𝐁𝐮𝐢𝐥𝐝𝐢𝐧𝐠 𝐏𝐚𝐲𝐦𝐞𝐧𝐭𝐬 𝐟𝐨𝐫 𝐀𝐠𝐞𝐧𝐭𝐢𝐜 𝐂𝐨𝐦𝐦𝐞𝐫𝐜𝐞, 𝐍𝐨𝐭 𝐃𝐞𝐦𝐨𝐬

This week’s insights

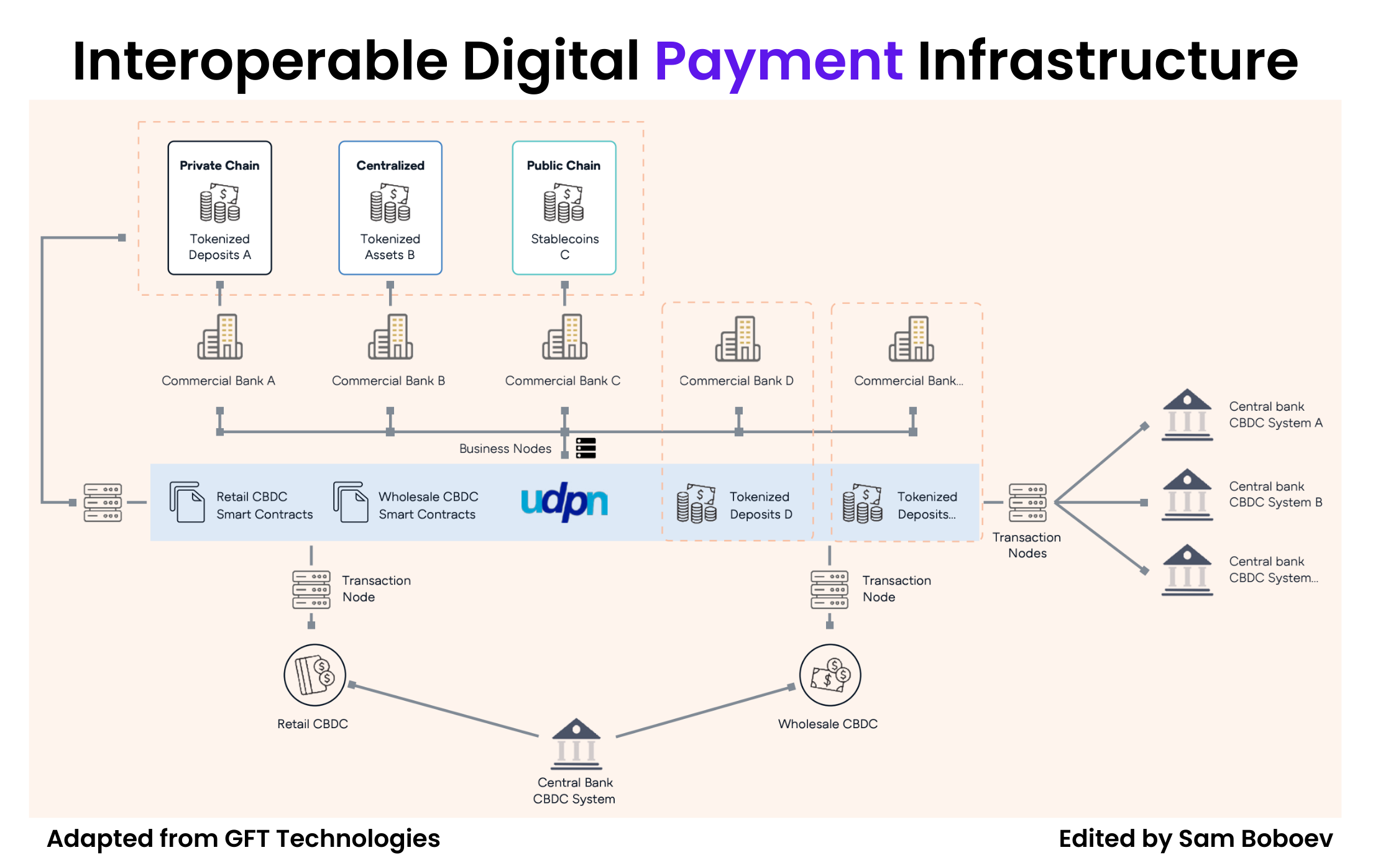

1️⃣𝐇𝐨𝐰 𝐭𝐨 𝐃𝐞𝐬𝐢𝐠𝐧 𝐈𝐧𝐭𝐞𝐫𝐨𝐩𝐞𝐫𝐚𝐛𝐥𝐞 𝐃𝐢𝐠𝐢𝐭𝐚𝐥 𝐏𝐚𝐲𝐦𝐞𝐧𝐭 𝐈𝐧𝐟𝐫𝐚𝐬𝐭𝐫𝐮𝐜𝐭𝐮𝐫𝐞

2️⃣𝐖𝐡𝐲 𝐀𝐈 𝐅𝐚𝐢𝐥𝐬 𝐢𝐧 𝐁𝐚𝐧𝐤𝐬

3️⃣𝐀𝐠𝐞𝐧𝐭𝐢𝐜 𝐏𝐚𝐲𝐦𝐞𝐧𝐭𝐬 𝐈𝐦𝐩𝐚𝐜𝐭 𝐨𝐧 𝐭𝐡𝐞 𝐏𝐚𝐬𝐬-𝐭𝐡𝐫𝐨𝐮𝐠𝐡 𝐏𝐚𝐲𝐦𝐞𝐧𝐭 𝐌𝐨𝐝𝐞𝐥

4️⃣𝐊𝐞𝐲 𝐡𝐚𝐧𝐬𝐡𝐚𝐤𝐞𝐬 𝐢𝐧 𝐭𝐡𝐞 𝐚𝐠𝐞𝐧𝐭𝐢𝐜 𝐜𝐨𝐦𝐦𝐞𝐫𝐜𝐞 𝐣𝐨𝐮𝐫𝐧𝐞𝐲

5️⃣𝐓𝐡𝐞 𝐍𝐞𝐨 𝐅𝐢𝐧𝐚𝐧𝐜𝐞 𝐌𝐚𝐫𝐤𝐞𝐭 𝐌𝐚𝐩

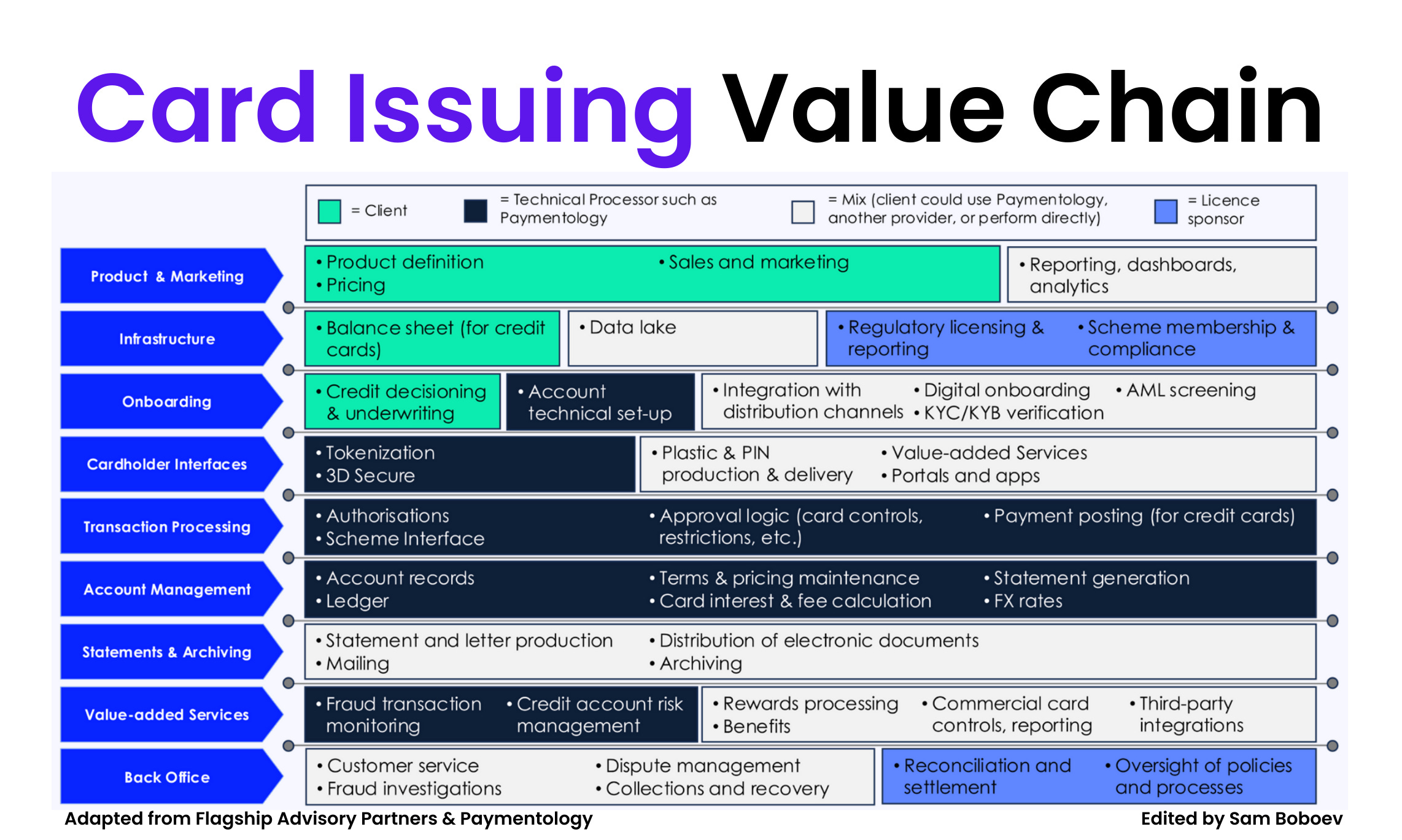

6️⃣𝐄𝐱𝐚𝐦𝐢𝐧𝐢𝐧𝐠 𝐂𝐚𝐫𝐝 𝐈𝐬𝐬𝐮𝐢𝐧𝐠 𝐕𝐚𝐥𝐮𝐞 𝐂𝐡𝐚𝐢𝐧𝐬 𝐢𝐧 𝐭𝐡𝐞 𝐔𝐊

7️⃣𝐓𝐡𝐞 𝐃𝐞𝐩𝐨𝐬𝐢𝐭 𝐓𝐨𝐤𝐞𝐧𝐬 – 𝐓𝐨𝐤𝐞𝐧 𝐜𝐫𝐞𝐚𝐭𝐢𝐨𝐧 & 𝐫𝐞𝐯𝐨𝐜𝐚𝐭𝐢𝐨𝐧 𝐩𝐫𝐨𝐜𝐞𝐬𝐬𝐞𝐬

𝐇𝐨𝐰 𝐭𝐨 𝐃𝐞𝐬𝐢𝐠𝐧 𝐈𝐧𝐭𝐞𝐫𝐨𝐩𝐞𝐫𝐚𝐛𝐥𝐞 𝐃𝐢𝐠𝐢𝐭𝐚𝐥 𝐏𝐚𝐲𝐦𝐞𝐧𝐭 𝐈𝐧𝐟𝐫𝐚𝐬𝐭𝐫𝐮𝐜𝐭𝐮𝐫𝐞

I’ve been studying how institutional stablecoin infrastructure is actually being built, not marketed.

GFT’s work on the Universal Digital Payments Network (UDPN) is a clear signal of where the real problem sits: interoperability, not token issuance.

The stablecoin market is fragmented by design. Different chains. Different regulatory regimes. Different compliance requirements. UDPN does not try to force convergence at the asset layer. It tries to standardize coordination instead.

____

Key observations.

UDPN treats interoperability as a messaging problem, not a bridging problem. Assets stay on their native rails. A standardized messaging backbone coordinates settlement, compliance signals, and transaction intent across stablecoins, CBDCs, and tokenized deposits. This removes cross-chain security risk and operational complexity.

____

Compliance is embedded, not bolted on. On-chain AML, jurisdiction-specific rules engines, and lifecycle management are part of the stablecoin management stack. A single stablecoin adapts to multiple regulatory regimes without being reissued or re-engineered.

Keep reading with a 7-day free trial

Subscribe to Fintech Wrap Up to keep reading this post and get 7 days of free access to the full post archives.