What is PAR? How Does It Work?; (Gen)AI Tech Architecture for Banks; Why B2B Payments Remain Fintech’s Biggest, Most Complex Opportunity;

Welcome to this week’s edition of Fintech Wrap Up—your quick dive into the biggest fintech stories

Insights & Reports:

1️⃣ What is PAR? How Does It Work?

2️⃣ Monzo’s Business, Explained

3️⃣ The trends in Open Banking and Open Finance adoption across the APAC region

4️⃣ (Gen)AI Tech Architecture for Banks

5️⃣ Case Study: Chainlink, Kinexys by J.P. Morgan, and Ondo Finance

6️⃣ Why Generative AI Initiatives Stall in Fintech—And How to Course-Correct

7️⃣ Why B2B Payments Remain Fintech’s Biggest, Most Complex Opportunity

8️⃣ The State of Multichain Development: Benchmarking Across Ecosystems

9️⃣ Starling Bank weighs US listing as it expands into American market

Hey everyone, I really appreciate each and every subscriber to my newsletter.

Today, I wanted to reach out and ask for a small favor.

If you find value in my newsletters, could I kindly ask you to do the following? It’ll help ensure you continue receiving these updates without interruption:

- Reply to the latest email with any thoughts or simply a quick “received.”

- Check your spam folder for any past emails.

- Mark Fintech Wrap Up as “important” and move it out of the Promotions tab (if applicable).

Thanks so much for your support! 🙌

TL;DR:

Welcome to this week’s edition of Fintech Wrap Up—your quick dive into the biggest fintech stories.

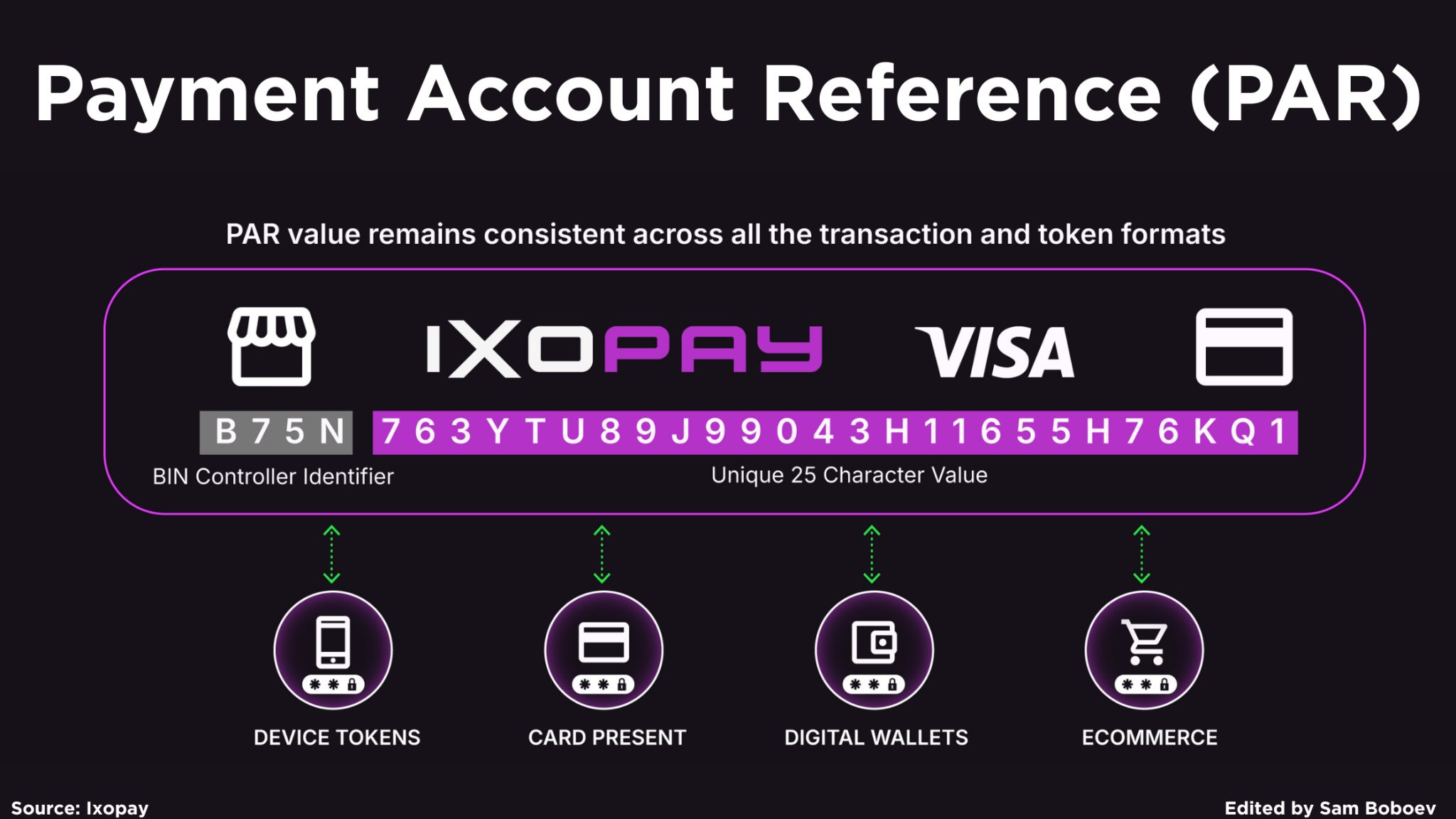

Let’s start with Payment Account Reference (PAR), a 29-character ID that links a customer’s transactions across channels, wallets, and processors—without revealing sensitive data. For merchants, it means unified customer views, smarter loyalty programs, better fraud detection, and reduced PCI burden. PAR is quietly becoming a must-have for omnichannel success.

Monzo’s rise is another standout. With over 12 million users, a +70 NPS, and full-year profitability, Monzo proves that customer obsession and solid tech can fuel both growth and margin. It’s one of the rare fintechs balancing mission and monetization.

In APAC, Open Banking is evolving with a market-driven flavor. Unlike Europe’s regulation-heavy model, countries like Singapore and Japan prefer soft guidance, while India and Indonesia follow stricter rules. The takeaway: without regulatory support, even agile models can struggle to scale.

AI in fintech still stumbles. McKinsey finds most GenAI pilots stall due to weak infrastructure and unclear governance. The fix? Build modular platforms with compliance baked in to unlock real, scalable innovation.

On the blockchain front, J.P. Morgan’s Kinexys, Chainlink, and Ondo executed a first-of-its-kind cross-chain DvP transaction—settling tokenized treasuries and payments atomically. It’s a blueprint for future institutional crypto rails.

And don’t overlook B2B payments: at $135T annually, they’re huge—but riddled with inefficiencies. Embedded fintech is stepping up to modernize flows from procurement to reconciliation using APIs and automation.

Until next time—thanks for reading Fintech Wrap Up!

Reports

Insights

What is PAR? How Does It Work?

📢 Are you grappling with fragmented customer data across different sales channels?

Tokenization protects your customers. But it limits visibility into customer behavior.

Different channels, wallets, and processors mean the same customer can look like 10 different people.

That makes it nearly impossible to link purchases, personalize loyalty offers, or even flag repeat fraud.

Enter: Payment Account Reference (PAR).

🔍 Imagine gaining a unified view of your customer's journey, regardless of whether they purchase:

🔹 Online

🔹 In-store

🔹 Via mobile app

👉 PAR is a game-changer for modern merchants.

It’s a 29-character alphanumeric ID that acts like a tracking number for a payment card. It links a single card account across all tokens, issuers, and channels. All without exposing sensitive card data or expanding your PCI scope.

👉 Why it matters:

Unify customer profiles across platforms, even when they check out as “guests.”

Run smarter loyalty programs without extra steps for your customers.

Spot fraud faster, like recurring chargebacks from the same card, even under different names.

Reduce PCI risk by eliminating the need to store PANs.

👉 Imagine this:

A customer frequently orders takeout from your restaurant's website using their saved card. Later, they dine in and pay with the same card. 💳

With PAR, your system can automatically recognize this as the same customer, allowing you to personalize future offers or even surprise them with a complimentary dessert based on their combined spending. It allows you to:

🔹 Recognize the same customer across channels

🔹 Auto-enroll them in your loyalty program

🔹 Flag suspicious activity, if needed

Think of it like the tracking ID you get when you order a package. 📦 Even if it changes carriers or routes, that single ID lets you follow the journey from start to finish.

PAR works the same way for payments. Whether a customer uses their phone, laptop, or physical card, PAR ties every transaction back to the same underlying account.

✅ It works across PSPs and token formats—giving you true omnichannel intelligence, without sacrificing security.

For businesses serious about increasing revenue, reducing risk, and creating seamless customer experiences, PAR isn’t just another payment acronym. It’s a strategic advantage that allows you to move beyond fragmented data and gain a true 360-degree understanding of your customers.

Monzo’s Business, Explained

Monzo has emerged as one of fintech’s standout success stories – a digital bank that now boasts over 12 million customers and a profitable business model. In an industry where many challengers are still chasing sustainable unit economics, Monzo has redefined what banking can be – and where it’s going. Launched in 2015 as a scrappy startup, Monzo set out to “build a current account that lives on your smartphone and gives you control of your money”. A decade later, it has grown into Britain’s largest digital bank and even reached full-year profitability – all while cultivating a devoted user base and an NPS around +70 (versus an industry average of 30). Monzo matters because it exemplifies how a relentless focus on customers can translate into both rapid growth and real revenues. This deep dive examines Monzo’s evolution, from its early days and expanding product portfolio to the technology under the hood, its business strategy, international forays, and the financial journey toward profit.

Monzo’s trajectory offers a blueprint for fintech innovation: prove that “mission, growth, [and] profit” can go hand in hand. By “bringing together the best of technology and banking, and remaining customer obsessed,” Monzo has shown it’s possible to delight users while building a sustainable bank. Let’s explore how Monzo got here and where it’s heading next.

Keep reading with a 7-day free trial

Subscribe to Fintech Wrap Up to keep reading this post and get 7 days of free access to the full post archives.