Deep Dive: Monzo’s Business, Explained

In an industry where many challengers are still chasing sustainable unit economics, Monzo has redefined what banking can be – and where it’s going

Monzo has emerged as one of fintech’s standout success stories – a digital bank that now boasts over 12 million customers and a profitable business model. In an industry where many challengers are still chasing sustainable unit economics, Monzo has redefined what banking can be – and where it’s going. Launched in 2015 as a scrappy startup, Monzo set out to “build a current account that lives on your smartphone and gives you control of your money”. A decade later, it has grown into Britain’s largest digital bank and even reached full-year profitability – all while cultivating a devoted user base and an NPS around +70 (versus an industry average of 30). Monzo matters because it exemplifies how a relentless focus on customers can translate into both rapid growth and real revenues. This deep dive examines Monzo’s evolution, from its early days and expanding product portfolio to the technology under the hood, its business strategy, international forays, and the financial journey toward profit.

Monzo’s trajectory offers a blueprint for fintech innovation: prove that “mission, growth, [and] profit” can go hand in hand. By “bringing together the best of technology and banking, and remaining customer obsessed,” Monzo has shown it’s possible to delight users while building a sustainable bank. Let’s explore how Monzo got here and where it’s heading next.

From Bold Idea to Banking License

Monzo’s story began in 2015, when a team led by Tom Blomfield founded the company (originally called Mondo) with the aim of creating a branchless, app-based bank. The vision was clear from the start: a bank “that lives on your smartphone”, delivering instant notifications, intuitive budgeting, and a user-friendly experience starkly different from high-street incumbents. Early on, Monzo launched Alpha and Beta prepaid debit cards to test the waters, rapidly gaining a waitlist of enthusiastic early adopters. This grassroots momentum was amplified by record-setting crowdfunding campaigns – in 2016, Monzo raised £1 million in 96 seconds from customers eager to own a part of the bank. By late 2018, Monzo had topped one million users, with 95% of its initial cardholders seamlessly migrating to its new current accounts once those launched. Growth came almost entirely through word of mouth, reflecting a passionate community that Monzo actively nurtured via forums and transparency reports.

Regulatory milestones came quickly. Monzo obtained a UK banking license with restrictions in 2016 and, after rigorous testing, had those restrictions lifted in April 2017 – officially becoming “a fully authorised, unrestricted bank”. This allowed Monzo to transition all customers from prepaid cards to full Monzo current accounts, each with a sort code and FSCS deposit protection. “Today is a major step towards making [our] mission a reality,” CEO Tom Blomfield wrote at the time, crediting Monzo’s community of users for fueling its early success. Throughout 2017–2018, Monzo rolled out core banking features like Monzo.me (for easy P2P payments) and Targets (budgeting goals), while maintaining an ethos of openness – Monzo famously shared product roadmaps and engaged users in feedback through its “Making Monzo” forum.

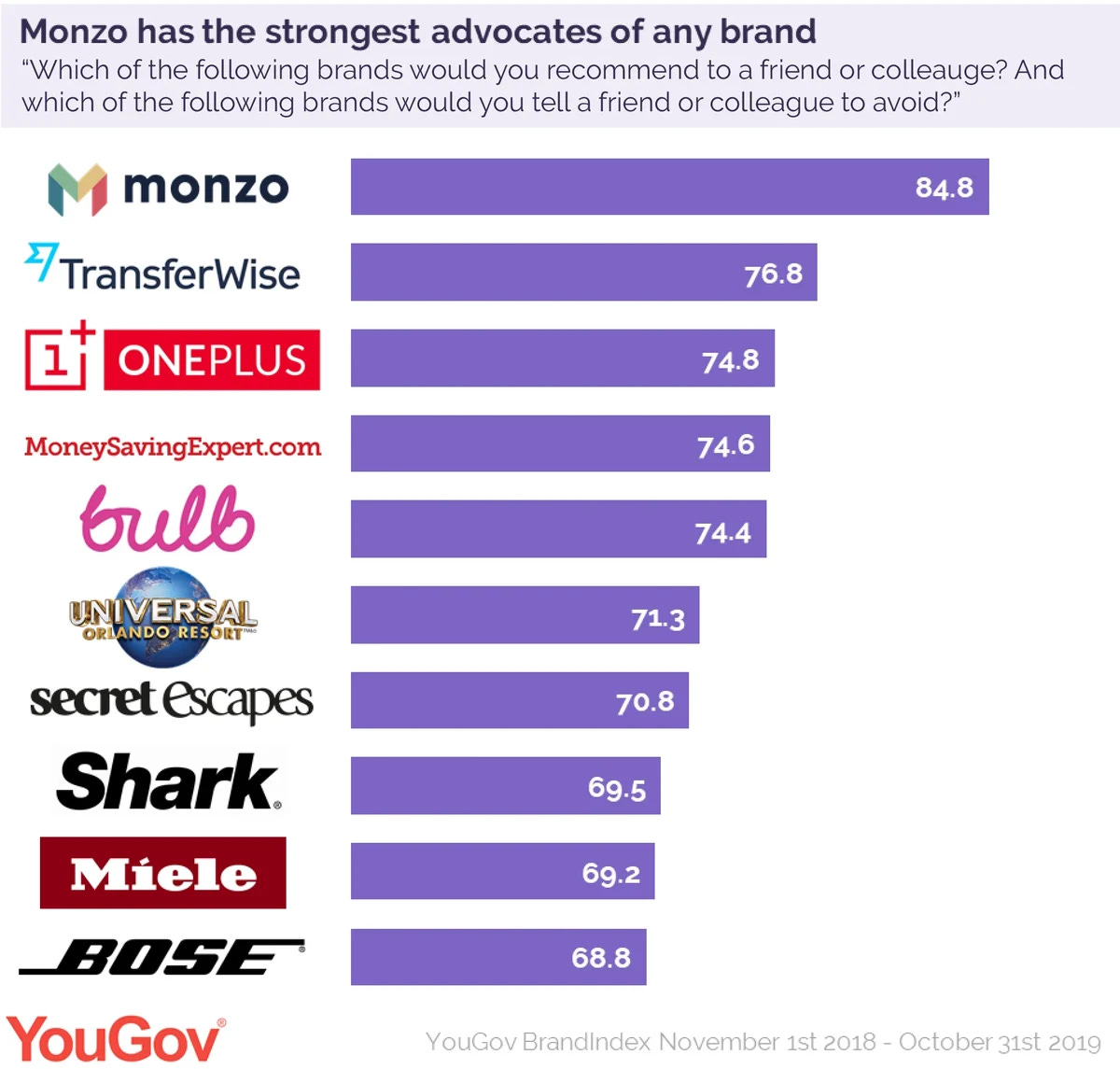

By 2019, Monzo was solidifying its position as a mainstream player. It became the UK’s most recommended brand according to YouGov and saw more people switching their primary accounts to Monzo than to any other bank. The bank introduced pioneering app features that competitors would later emulate – Salary Sorter to auto-budget paychecks, Bills Pots to segregate funds for expenses, and Get Paid Early to receive BACS payments a day in advance. All these innovations, alongside the vibrant coral debit card and real-time notifications, helped Monzo build a reputation for making money feel easy. Despite the challenges of 2020’s pandemic (when lockdowns briefly dampened card spending), Monzo kept investing in its product. “As the world shut down, we stayed focused on our customers... delivered new products and invested heavily in key areas of our business,” said TS Anil (who took over as CEO in 2020). That resilience paid off: customer growth remained robust – climbing 23% year-on-year in FY2021 – and engagement deepened even faster.

Fast forward to 2023 and Monzo had swelled to around 7½ million personal customers (plus hundreds of thousands of business users) and was ranked as the 7th largest UK bank by customer numbers. It also consistently topped independent surveys for service quality, reflecting the loyalty of its base. Remarkably, 66–90% of Monzo’s customer growth came organically via referrals in these years – a testament to its product-market fit and brand love. A typical Monzo user had 30+ friends on Monzo too, underscoring a viral network effect. Monzo’s journey from a bold idea in 2015 to a fully licensed, multi-million-user bank within a decade is impressive on its own. But equally notable is how Monzo evolved its product lineup beyond a simple checking account to become a broad financial platform.

Evolving the Product Portfolio

Monzo’s initial offering was a simple app-linked account, but over time it has broadened into a one-stop shop for personal finance. Today, “Monzo’s now a place where you can budget, spend, save, borrow, invest, track your mortgage, insure your contents, and combine your pensions.” This product diversification did not happen overnight – it was a deliberate expansion, year by year, often driven by customer demand and experimentation.

Everything still “starts with our personal current account,” as Monzo likes to say. The personal account (with its bright “hot coral” debit card) remains Monzo’s flagship, offering features like instant spend notifications, fee-free spending abroad, and easy money management. Monzo also provides joint accounts for shared finances, and in 2023 it introduced accounts for 16-17 year-olds, eventually followed by Under 16s accounts in 2025 to help the next generation manage money digitally. On the business side, Monzo launched its business accounts in 2020 after a period of testing. By FY2024, Monzo Business had over 400,000 customers (up from 200k the year prior), ranging from sole traders on free accounts to larger SMEs paying for premium plans. Monzo’s business banking has been well-received – for the past two years it’s been rated Britain’s most recommended business account for overall service quality in independent surveys.

To monetize its robust retail base, Monzo rolled out premium account tiers in 2020. Monzo Plus (re-launched in July 2020 after an earlier iteration faltered) and Monzo Premium (launched later in 2020) offer advanced features for monthly fees. Plus (originally £5/month) added perks like custom budgeting categories, interest on balances, and virtual cards, while Premium (at £15/month) tacked on benefits like phone insurance, higher interest, and a metal debit card. These proved popular with Monzo’s power users: within the first year, over 134,000 customers signed up for Plus or Premium. By FY2022, Monzo reported 360,000+ combined subscribers across Plus, Premium, and paid business accounts. Subscription uptake contributed meaningfully to revenue – by 2021, 25% of Monzo’s revenue was coming from new products (like Plus/Premium and business accounts). Notably, Monzo has continued iterating on its plans. In 2023, it even made some formerly paid features free for all (for instance, releasing its “most powerful budgeting tools” to the entire user base) to drive engagement, while simultaneously enhancing the paid tiers with new benefits. The result: by FY2025 Monzo had 1 million+ customers on subscription plans, and subscription fee income grew 50% year-on-year.

Keep reading with a 7-day free trial

Subscribe to Fintech Wrap Up to keep reading this post and get 7 days of free access to the full post archives.