Visa Q1 FY26 Results; The Architecture of the Onchain Bank; Overview of Roles in the Cards Ecosystem

Video of the Week

Deep Dive of the Week

JPMorgan’s Payments Strategy and Systems-Level Integration Analysis

I’ve been following JPMorgan’s methodical buildout of a payments empire. The firm has quietly integrated every layer of the payments stack from corporate treasury to merchant acquiring into a unified infrastructure. In this report, I break down how JPMorgan segments its payments business, the technology platforms underpinning it, and the long-term moat the bank is fortifying.

This week’s reports

2️⃣Airwallex is not a payments company

3️⃣Stablecoins Are Imperfect but Inevitable

5️⃣Payments’ state of play 2026

6️⃣Deep Dive - 2025 FinTech Almanac by FT Partners

7️⃣Practical pricing framework for fintech companies

This week’s insights

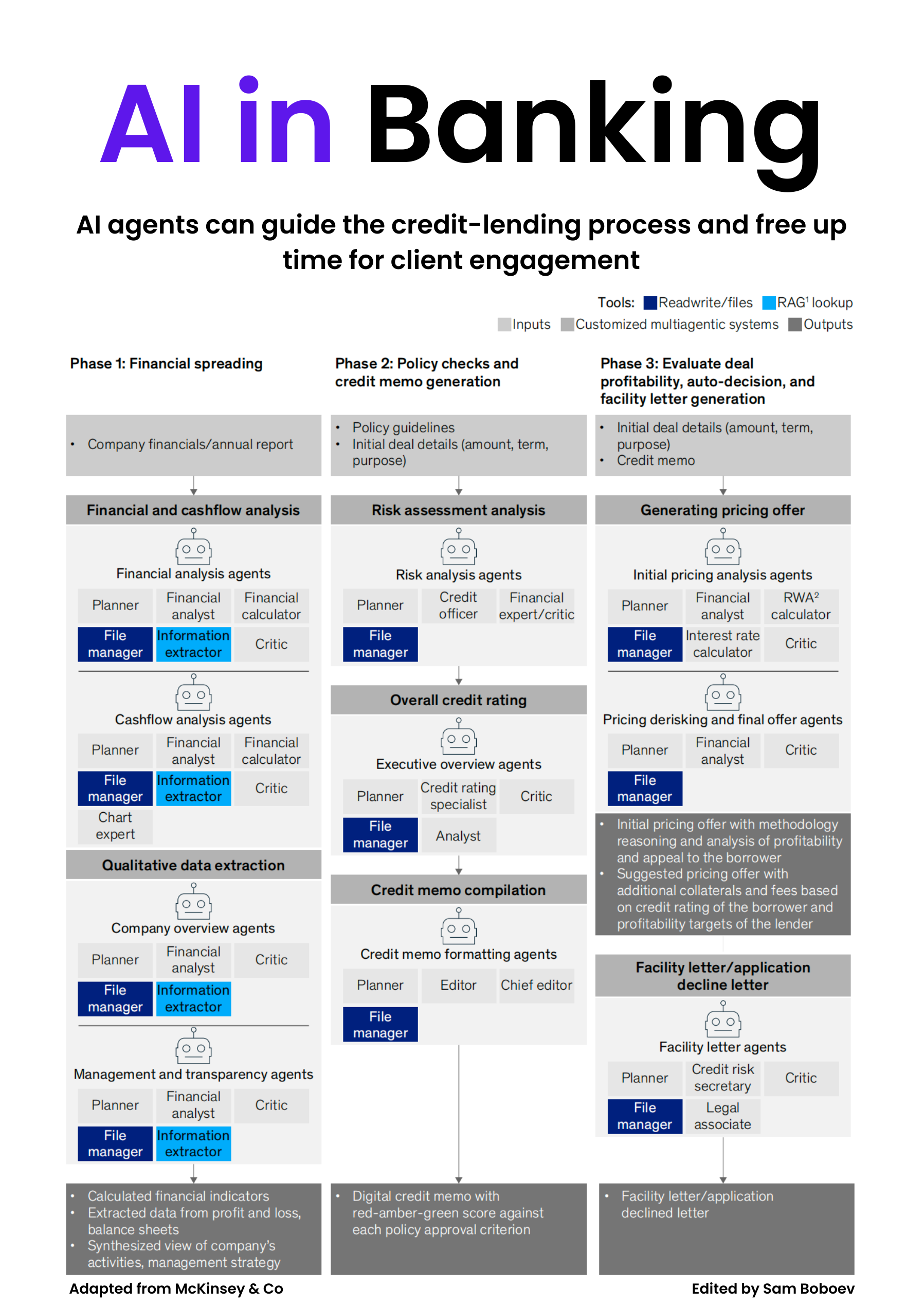

1️⃣How agentic AI actually changes inside lending and credit operations

2️⃣Agentic Commerce Creating New Payment Models

3️⃣Overview of Roles in the Cards Ecosystem

4️⃣Deposit Tokens - P2P Deposit Token Transaction

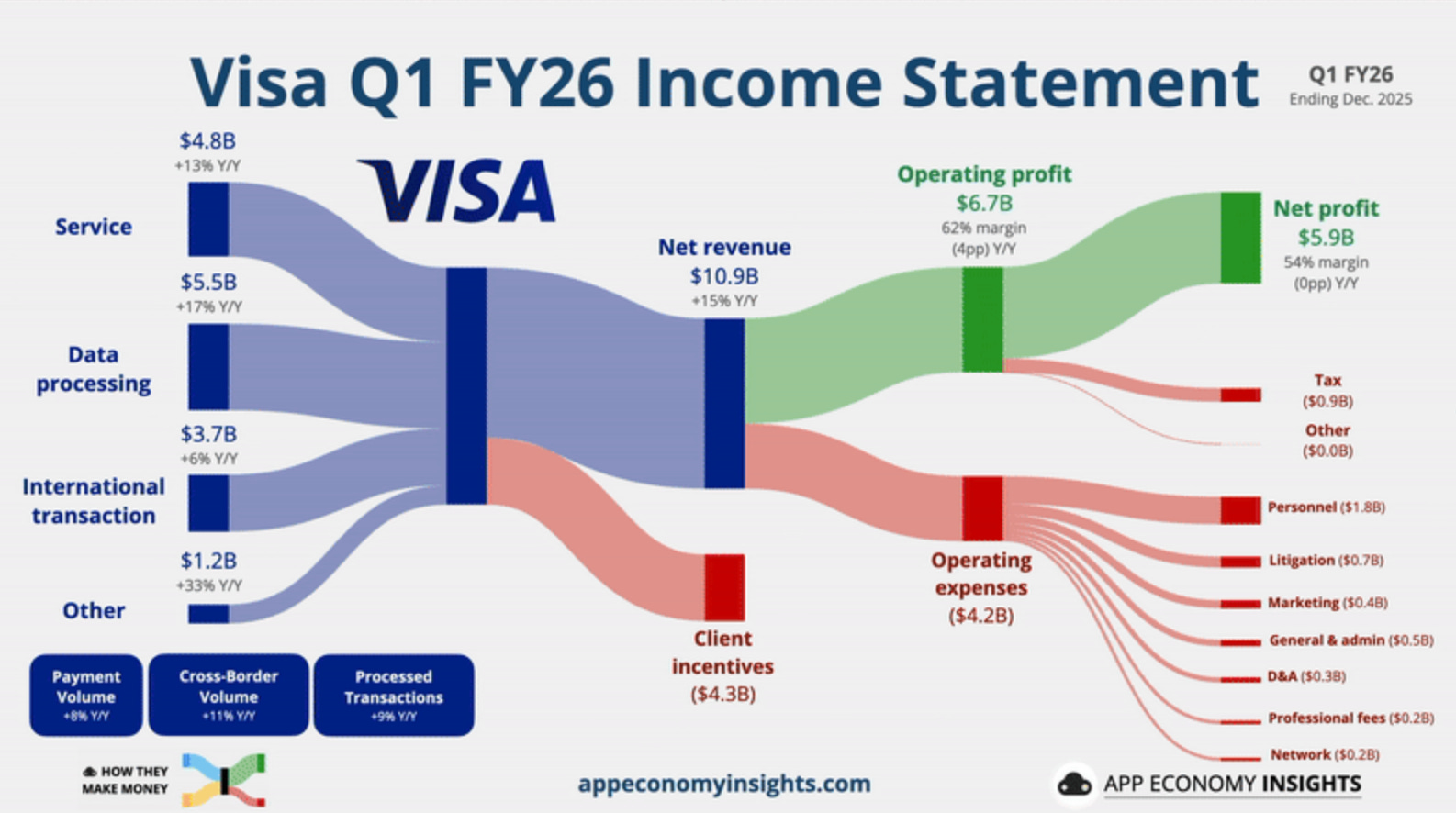

5️⃣Visa Q1 FY26 Results

6️⃣Payment Tokenization Explained

7️⃣The Architecture of the Onchain Bank

How agentic AI actually changes inside lending and credit operations

I mapped what agentic AI actually changes inside lending and credit operations. Not conceptually. Operationally.

Traditional credit is memo-driven. Analysts extract financials, interpret policy, calculate ratios, draft credit notes, review each other’s work, then repeat. Outputs vary by person. Turnaround time stretches to days. Risk logic lives in people’s heads.

Agentic underwriting replaces this with an AI-led credit assembly line built around three explicit phases.

____

Phase 1: Financial spreading

This is not data extraction. It is structured interpretation. AI agents ingest annual reports, management accounts, and bank statements, then:

- Normalize P&L, balance sheet, and cashflow data across formats

- Reconstruct financial indicators consistently across borrowers

- Synthesize qualitative context on business model, revenue concentration, and management behavior

The output is a standardized financial view. Analyst variance is removed before risk is discussed.

____

Phase 2: Policy checks and credit memo generation

This is where underwriting logic moves from human memory into systems.

Agents evaluate the deal against credit policy line by line:

- Amount, tenor, purpose, sector exposure

- Covenant and structural constraints

- Risk drivers translated into red-amber-green scores per approval criterion

The credit memo becomes a digital artifact with traceable reasoning. Humans review exceptions, not entire files. Consistency is enforced by architecture, not training.

____

Phase 3: Deal evaluation, pricing, and facility output

Keep reading with a 7-day free trial

Subscribe to Fintech Wrap Up to keep reading this post and get 7 days of free access to the full post archives.