UK Fintech Unicorns: What the Multiples Are Telling Us; Mastercard Q4 FY 2025 Results; Agentic Commerce Market Tracker

Video of the Week

Deep Dive of the Week

How Zelle Scaled to $1.2 Trillion by Embedding Into Banking

The Zelle network owned by Early Warning Services handled over $1.2 trillion in 2025 (20% growth) on roughly 4.2 billion transactions, far outpacing the 3–4% pace of U.S. consumer spending. Roughly 30% of that volume is payments to or from small businesses, underscoring Zelle’s role in everyday commerce. Banks are now expanding Zelle globally: in late 2025 Early Warning announced a stablecoin-based cross-border initiative “to bring speed and reliability” to international payments, to be offered on equal terms to all Zelle banks. Integration of Zelle typically means partnering with a sponsor bank or vendor (e.g. Alacriti’s Orbipay) and using ISO20022-based APIs. Key trade-offs include security and fraud: regulators note hundreds of millions lost to scams (CFPB cited ~$870M since 2017), while Early Warning touts that 99.95% of transactions have no reported fraud. Consumer protection laws (EFTA/Reg E) do not easily reverse Zelle’s instant transfers, so banks emphasize fraud mitigation and user education. For fintechs, the decision to integrate with or compete against Zelle hinges on infrastructure and strategy: partnering with a bank or fintech provider offers real-time P2P liquidity and access to Zelle’s 2,300+ FI network, but imposes network fees and compliance duties. Alternatives like FedNow (free real-time ACH), card-rail push payments, or crypto rails each carry different cost, speed, and risk profiles. In this article, I unpack integration options, technical flows, security/regulatory issues, and strategic product and go-to-market considerations. In short, Zelle integration can deepen customer relationships and expedite B2C/B2B payouts, but requires balancing irreversible payment risk against speed and reach.

This week’s reports

1️⃣ How European Banks Are Embracing Stablecoins

2️⃣ The $62 Trillion Stablecoin Myth

3️⃣ Agentic payments are not just a UX upgrade

4️⃣ State of Fintech 2026 report by F-Prime

5️⃣ Stablecoins Inherit Treasury Fragility

7️⃣ Five Stablecoin Adoption Trends by Stripe

This week’s insights

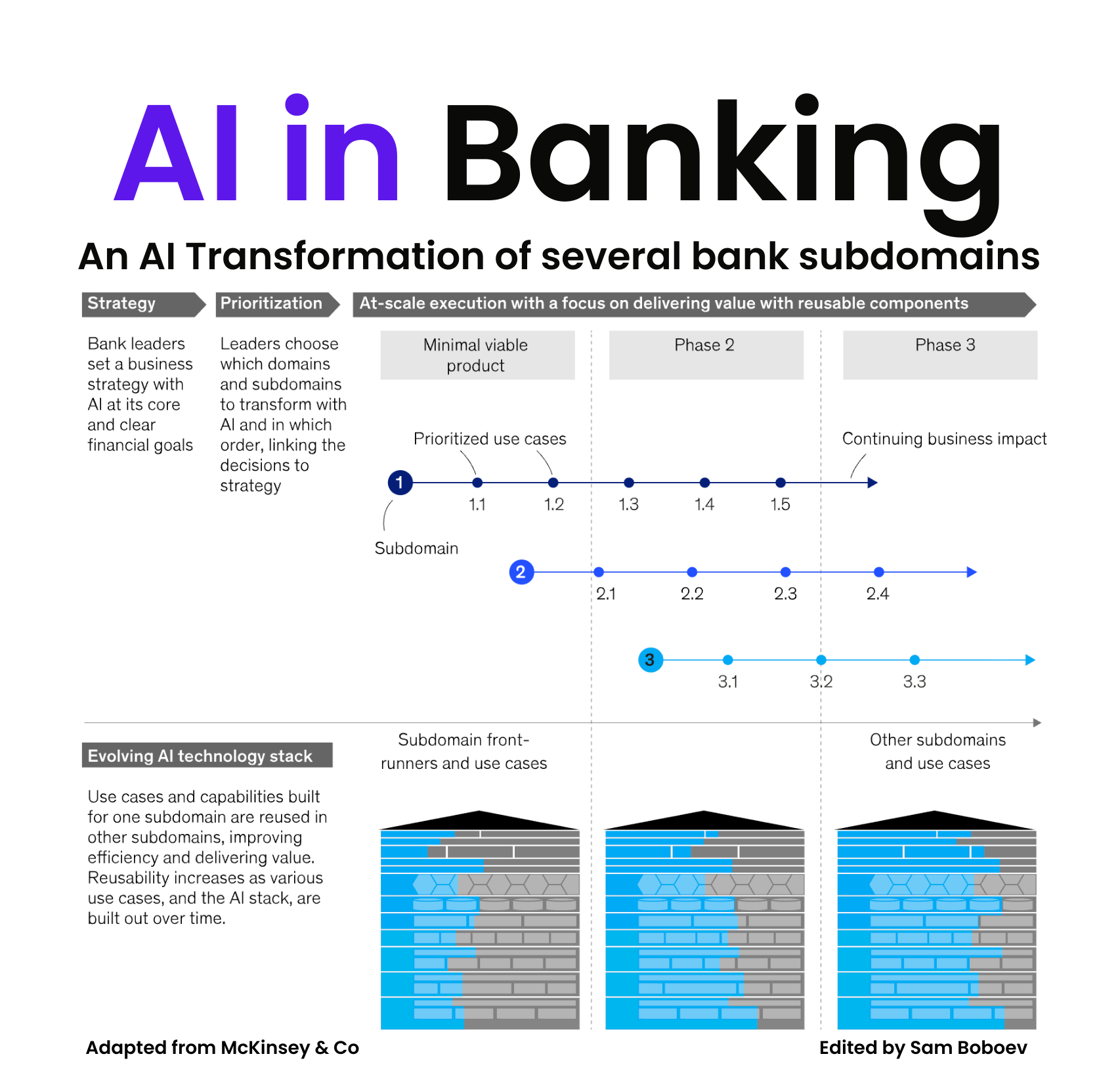

1️⃣Scaling AI in Banks Is a Governance Problem, Not a Data Problem

2️⃣Agentic Commerce Market Tracker

3️⃣How Blockchain Data Represents Stablecoin Activity

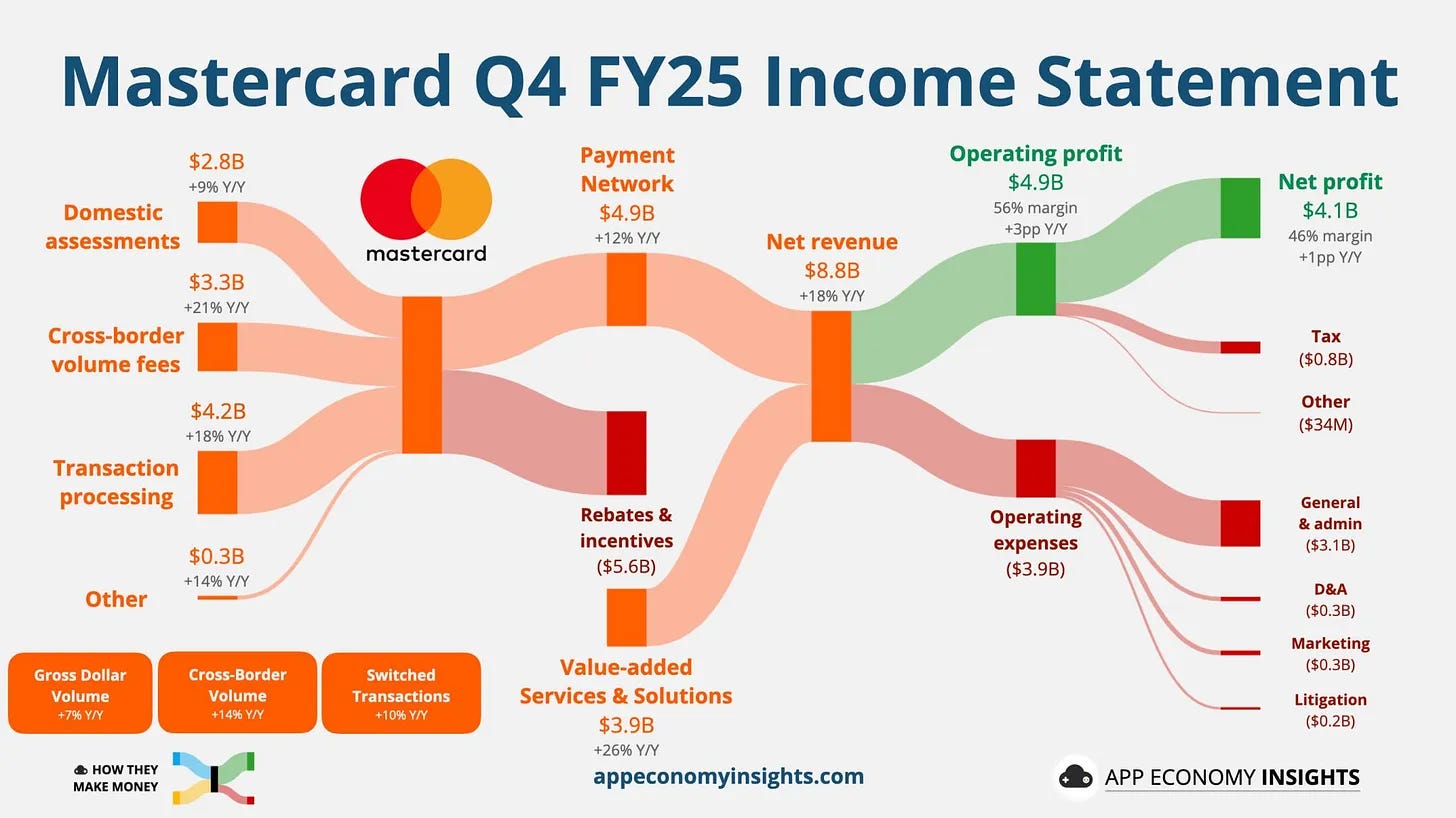

4️⃣Mastercard Q4 FY 2025 Results

5️⃣UK Fintech Unicorns: What the Multiples Are Telling Us

6️⃣Agentic Commerce 101

7️⃣How Much Stablecoin Volume Is Actually Payments?

Scaling AI in Banks Is a Governance Problem, Not a Data Problem

A successful AI transformation balances two things at once: near-term financial impact and long-term capability building. Miss either, and the effort stalls.

____

Here’s what actually works.

AI transformation does not start with a platform. It starts with a business strategy where AI is explicit, not implied. Domains and subdomains are selected based on value density, not technical curiosity. Execution then happens at scale, with reuse designed in from day one.

One large bank illustrates this well. Instead of shipping isolated models, it built reusable assets and an end-to-end analytics pipeline powering 50+ machine-learning models. Those components now support more than 150 use cases across the bank. Early impact: ~10% projected revenue uplift from hyper-personalization, lead optimization, and cross-sell. Same core assets. Different domains. Compounding returns.

____

This is the pattern most teams miss.

Transform one subdomain deeply. Move from MVP to industrialized use cases. Extract reusable components. Then plug them into adjacent subdomains. Build the AI stack in phases. Never all at once.

____

The real bottlenecks are not technical.

Keep reading with a 7-day free trial

Subscribe to Fintech Wrap Up to keep reading this post and get 7 days of free access to the full post archives.