Deep Dive: How Zelle Scaled to $1.2 Trillion by Embedding Into Banking

The Zelle network owned by Early Warning Services handled over $1.2 trillion in 2025 (20% growth) on roughly 4.2 billion transactions, far outpacing the 3–4% pace of U.S. consumer spending. Roughly 30% of that volume is payments to or from small businesses, underscoring Zelle’s role in everyday commerce. Banks are now expanding Zelle globally: in late 2025 Early Warning announced a stablecoin-based cross-border initiative “to bring speed and reliability” to international payments, to be offered on equal terms to all Zelle banks. Integration of Zelle typically means partnering with a sponsor bank or vendor (e.g. Alacriti’s Orbipay) and using ISO20022-based APIs. Key trade-offs include security and fraud: regulators note hundreds of millions lost to scams (CFPB cited ~$870M since 2017), while Early Warning touts that 99.95% of transactions have no reported fraud. Consumer protection laws (EFTA/Reg E) do not easily reverse Zelle’s instant transfers, so banks emphasize fraud mitigation and user education. For fintechs, the decision to integrate with or compete against Zelle hinges on infrastructure and strategy: partnering with a bank or fintech provider offers real-time P2P liquidity and access to Zelle’s 2,300+ FI network, but imposes network fees and compliance duties. Alternatives like FedNow (free real-time ACH), card-rail push payments, or crypto rails each carry different cost, speed, and risk profiles. In this article, I unpack integration options, technical flows, security/regulatory issues, and strategic product and go-to-market considerations. In short, Zelle integration can deepen customer relationships and expedite B2C/B2B payouts, but requires balancing irreversible payment risk against speed and reach.

Network and Volume Growth

Zelle has become a foundational digital payments rail in the U.S. By end-2025, all major banks and roughly 2,500 credit unions are onboard. Those institutions account for 80% of all U.S. deposit accounts, even though they represent only a quarter of banks by count. Volume exploded during 2020–2025: Zelle’s annual dollar volume tripled from ~$300 billion in 2020 to over $1 trillion in 2024, and reached $1.2 trillion in 2025. Daily peaks have been staggering: a single day in August 2025 saw $9 billion in transactions. Small businesses have rapidly adopted Zelle: in 2025 nearly 8 million businesses were enrolled, and they moved $357 billion (26% growth). This capture of merchant flows – from landscapers to care providers – highlights Zelle’s penetration beyond consumer P2P into the economy’s core.

This scale matters for any fintech strategy. Notably, more than 99% of credit union users say Zelle in their app positively impacts how they view their bank (see sidebar). Conversely, surveys show many consumers consider switching banks if they lack Zelle access. Zelle, by “keeping payments inside the secured banking experience,” helps banks retain deposits that might otherwise flow to third-party apps. In practice, offering Zelle has been shown to drive higher engagement and small-business retention: one bank saw a 78% surge in small-business payments after launching Zelle for Business. In summary, for U.S. domestic payments the network effect of Zelle is very strong.

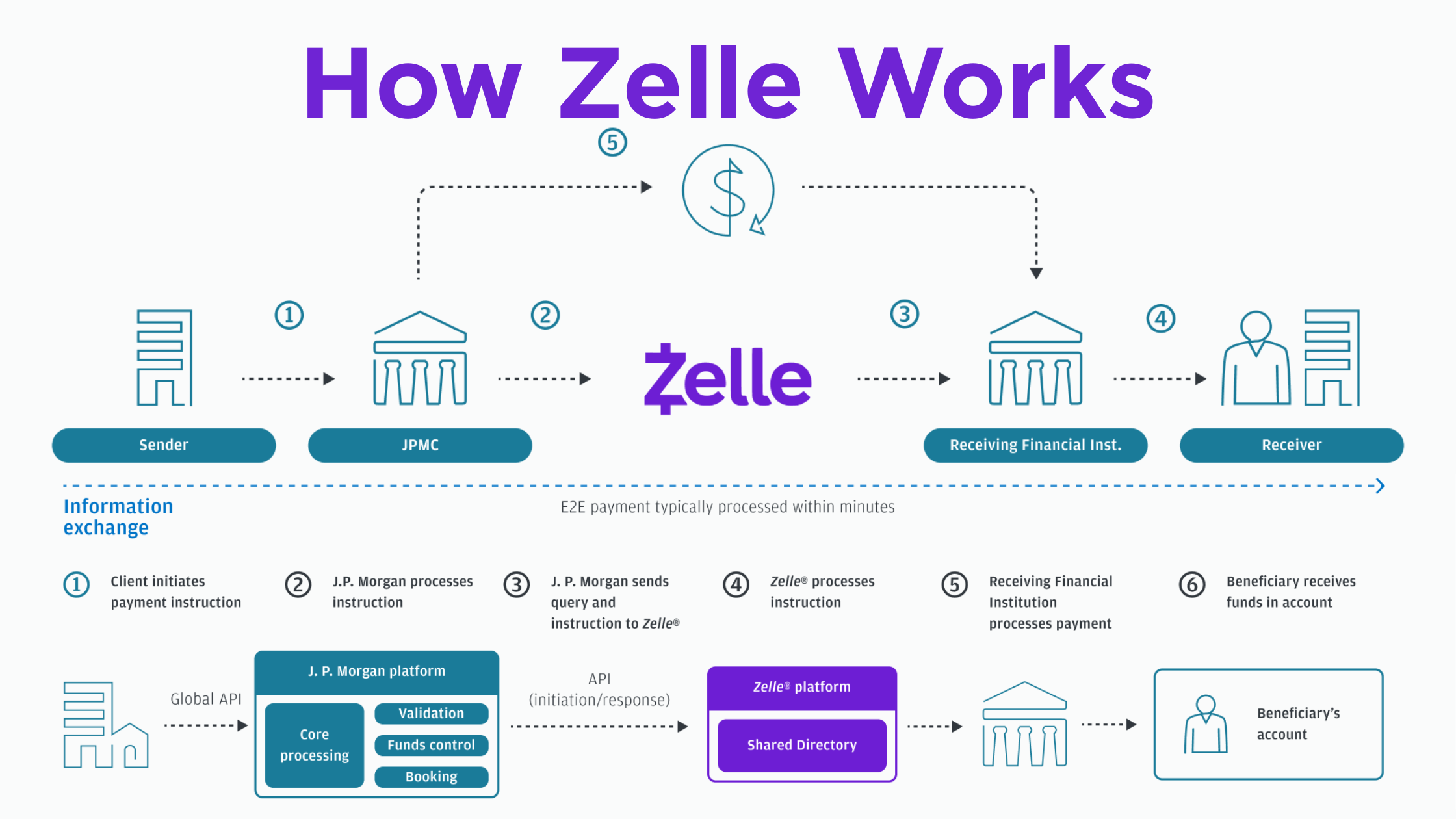

Integration Architecture and Options

From a systems perspective, integrating Zelle means connecting through its owner/consortium network via licensed sponsor banks. J.P. Morgan’s Global Payments API provides one model: it exposes a 24/7 real-time “Zelle Disbursement” capability where corporate clients can POST a payment using a beneficiary’s email or phone token. The API flow is straightforward: the payer’s bank sends a payment file to the Zelle network, which routes it to the receiver’s bank, crediting the recipient’s account within minutes. Each corporate transfer can be up to $100,000 and is irrevocable. The integration is ISO20022-based and supports name-matching controls to reduce misdirected payments.

Keep reading with a 7-day free trial

Subscribe to Fintech Wrap Up to keep reading this post and get 7 days of free access to the full post archives.