Revolut eyes $100bn valuation with fresh share sale; Understanding Agentic Payments; Stripe vs Adyen

Video of the Week

Deep Dive of the Week

Why Fintechs and Crypto Companies Want US Bank Charters

I treat “getting a charter” as buying a different physics model for your business. It is not branding. It is permissioning, funding, and durable control over dependencies.

Fintechs pursue charters for three hard reasons: (1) cheaper and stickier funding via insured deposits rather than wholesale lines and securitizations, (2) federal preemption and single-regulator operating posture instead of state-by-state licensing and sponsor-bank fragility, and (3) direct or more durable access to payment rails and network roles that are otherwise rented through partners.

Crypto companies pursue charters, especially national trust bank variants, to sit inside the regulated custody and settlement perimeter: fiduciary custody, qualified custodian posture, reserve management for stablecoins, and in some cases stablecoin issuance under the post-2025 federal stablecoin framework.

The trade is non-negotiable. You exchange speed for sovereignty. You reduce partner risk and unit funding costs, but you accept capital lock-up, BSA/AML burden, examiner-driven operating cadence, affiliate constraints, and higher scrutiny on anything that looks like regulatory arbitrage.

This week’s reports

1️⃣Governments are entering a new phase of AI adoption

2️⃣Fintech VC Is Repricing Around AI, Infrastructure, and Liquidity

3️⃣Why 97% of Banks Are Falling Behind in AI

4️⃣The internet was built without a native payment layer

5️⃣Mexico is structurally primed for a Fintech 3.0 shift

6️⃣Tokenised money is not a new payment method. It is a redesign of settlement architecture

7️⃣Stablecoin Utility Report 2026

This week’s insights

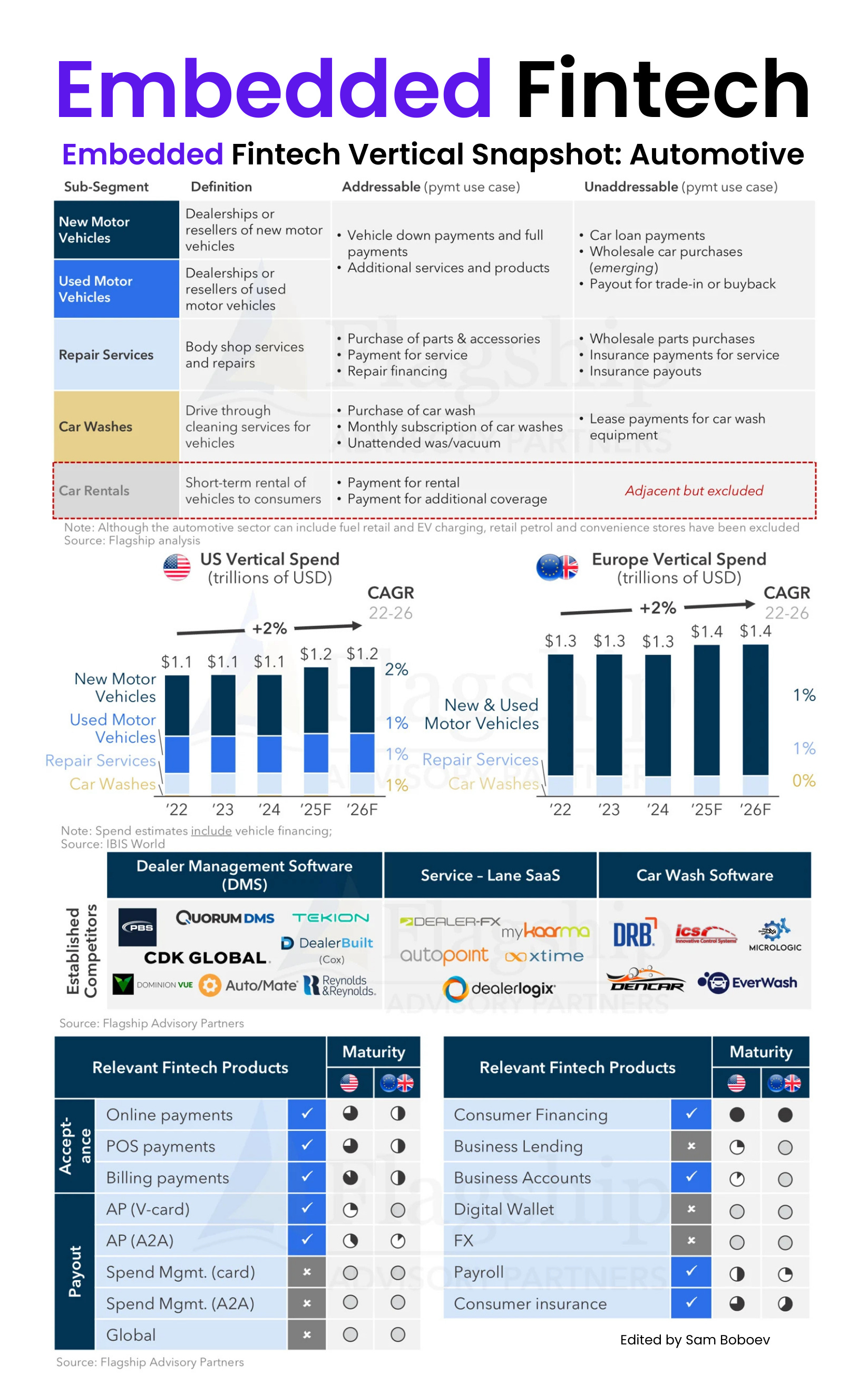

1️⃣Embedded Fintech Vertical Snapshot: Automotive

2️⃣The United States is not adopting tokenization for novelty. It is weaponizing distribution

3️⃣Settlement on the blockchain: Stablecoin payments finality in focus

4️⃣Stripe vs Adyen

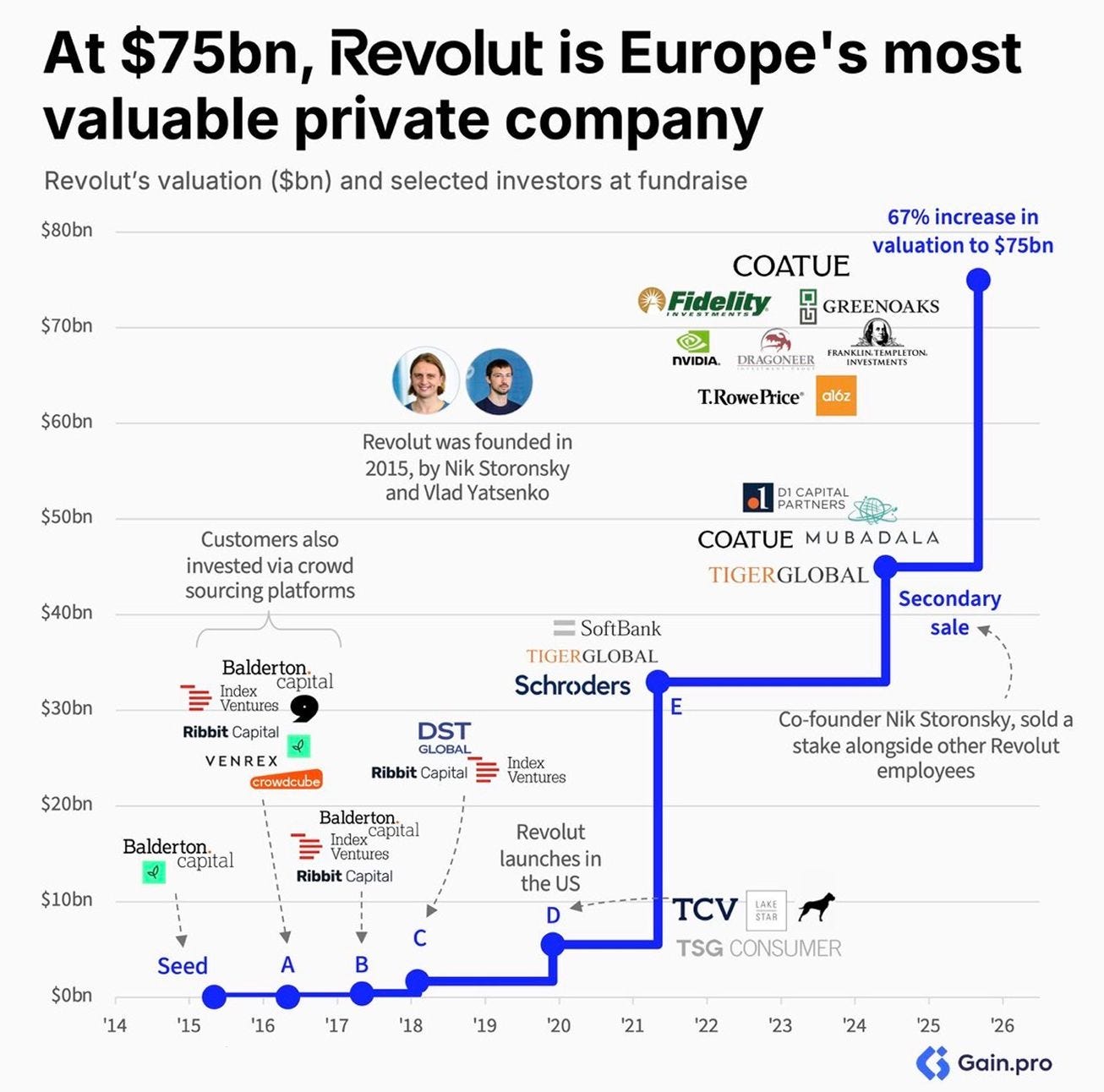

5️⃣Revolut eyes $100bn valuation with fresh share sale

6️⃣Understanding Agentic Payments

7️⃣A clearer view of stablecoin payment activity

Embedded Fintech Vertical Snapshot: Automotive

The automotive industry is highly complex with high software penetration (95% of companies use software to manage at least part of their business). However, embedded fintech adoption varies. While payment acceptance is relatively mature, we see substantial opportunity, especially in payouts and lending.

General Commentary & Highlights

- High software usage: The automotive industry is very dependent on software. 95% of companies use software to manage at least one part of their business in US and EU.

- Consolidated list of providers: Most dealerships rely on dealer management systems (DMS) for end-to-end business management. Various point solutions also exist to service specific functions or business areas.

- Tender Mix: Vehicle financing is largely un-addressable by PSPs, but remaining serviceable payment opportunity, is large, and card-centric (credit + debit covers 75% or more in the US and EU). This pool of volume largely originates from the service lane.

- In-car payments: enable drivers to transact directly from their, are seeing increased adoption; however, usage remains largely confined to car washes and has not yet extended to repair services.

Embedded Fintech Highlights

Keep reading with a 7-day free trial

Subscribe to Fintech Wrap Up to keep reading this post and get 7 days of free access to the full post archives.