Deep Dive: Why Fintechs and Crypto Companies Want US Bank Charters

I treat “getting a charter” as buying a different physics model for your business. It is not branding. It is permissioning, funding, and durable control over dependencies.

Fintechs pursue charters for three hard reasons: (1) cheaper and stickier funding via insured deposits rather than wholesale lines and securitizations, (2) federal preemption and single-regulator operating posture instead of state-by-state licensing and sponsor-bank fragility, and (3) direct or more durable access to payment rails and network roles that are otherwise rented through partners.

Crypto companies pursue charters, especially national trust bank variants, to sit inside the regulated custody and settlement perimeter: fiduciary custody, qualified custodian posture, reserve management for stablecoins, and in some cases stablecoin issuance under the post-2025 federal stablecoin framework.

The trade is non-negotiable. You exchange speed for sovereignty. You reduce partner risk and unit funding costs, but you accept capital lock-up, BSA/AML burden, examiner-driven operating cadence, affiliate constraints, and higher scrutiny on anything that looks like regulatory arbitrage.

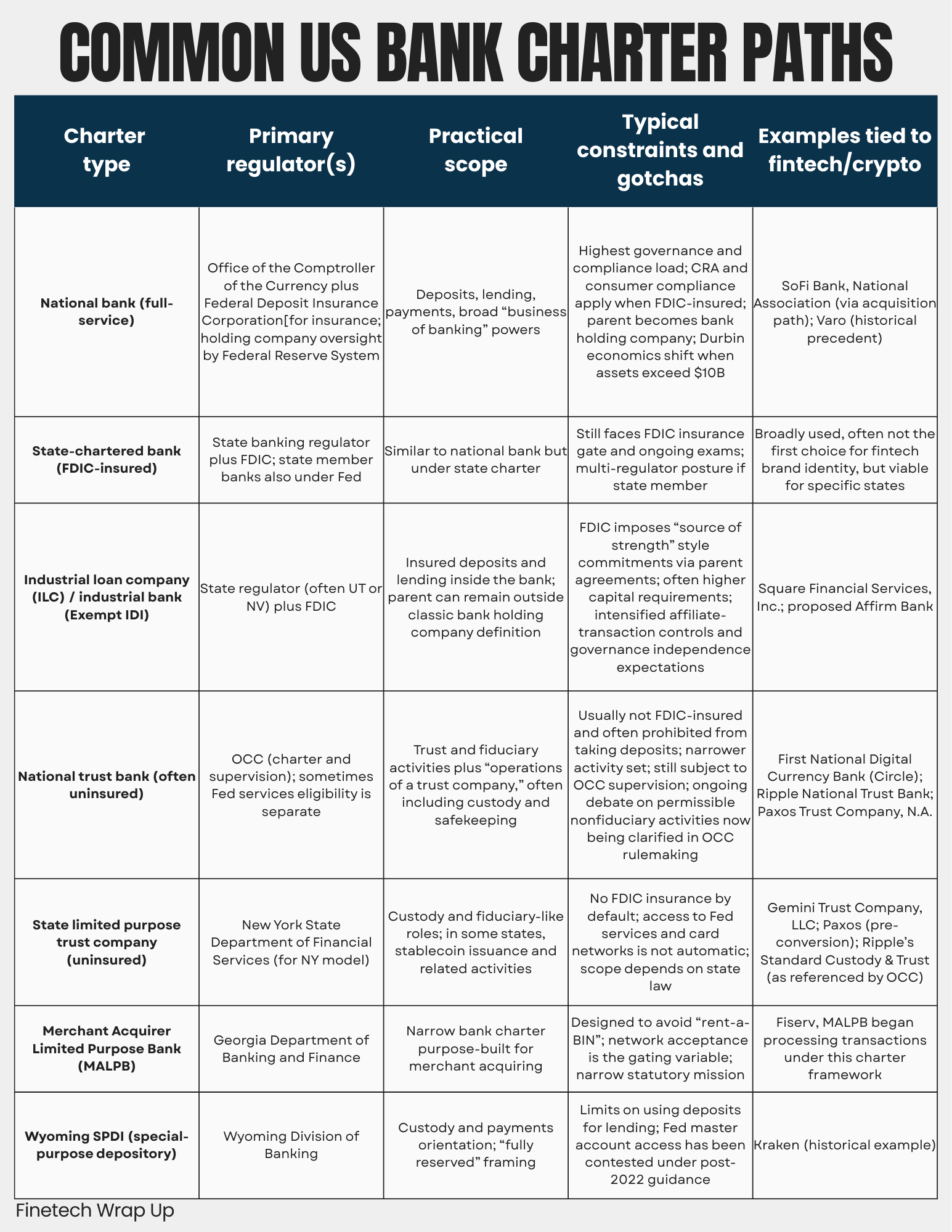

Charter types and what they actually enable

When I map charter interest across fintech and crypto, I see firms selecting from a menu of “legal capabilities,” not picking a monolithic status badge. The recent wave is heavy on limited-purpose designs (trust banks, merchant-acquirer charters, ILCs) because they target a single bottleneck: funding, network access, or custody.

Comparative table of common US charter paths

Policy and regulatory drivers behind the 2023 to 2026 charter push

I do not attribute the charter wave to “confidence.” I attribute it to shifted constraints. The sponsor-bank model got more expensive and less stable under tighter third-party oversight, while regulators reopened explicit pathways for de novo charters and trust-bank activity expansion.

Three policy shifts matter most:

First, banking agencies finalized third-party risk management guidance in mid-2023. This raised baseline expectations for banks that “rent their plumbing,” especially around due diligence, ongoing monitoring, and contract controls. That change flows straight through to fintech programs as higher friction, slower approvals, and more abrupt exits when a sponsor bank’s exam cycle goes sideways.

Second, the post-2022 framework for Federal Reserve master account access institutionalized tiered scrutiny. Non-federally-insured institutions, especially those outside Tier 2 conditions, fall into Tier 3 and “generally receive the strictest level of review.” This makes “I got a special charter so I get Fed access” a flawed assumption. Charter selection now has to include a realistic path to Fed services, not just the paper license.

Keep reading with a 7-day free trial

Subscribe to Fintech Wrap Up to keep reading this post and get 7 days of free access to the full post archives.