Reports: The $400T Future of Tokenised Assets; Mapping the Top 100 Stablecoins and Their Future; State of AI in FinTech

This week’s reports highlight three major themes shaping financial services: the rise of tokenized assets, the growing role of AI, and the increasing burden of compliance. Research suggests tokenized assets could expand from a niche market into a multi-trillion-dollar ecosystem by 2030, supported by improving liquidity, infrastructure, and regulatory clarity. Meanwhile, stablecoins are challenging traditional payment economics by offering cheaper, programmable settlement rails that could pressure interchange-based revenue models. AI continues to deliver significant efficiency gains across fintech, particularly in compliance, underwriting, and fraud prevention, though rising AI infrastructure costs are offsetting some productivity benefits. Across the industry, compliance remains both a major operational challenge and a growing opportunity for automation, while blockchain adoption is increasingly shifting from experimentation toward practical applications in money, contracts, and financial markets.

Video of the Week

Deep Dive of the Week

Tokenized Money Validates the Need for Unified Bank OS Infrastructure

The transition from traditional fiat messaging to tokenized asset execution represents the most significant architectural shift in the history of financial services. This evolution marks the end of the era of the ledger as a passive database and the beginning of the ledger as an active, programmable operating system.

The key insight driving this shift is simple but profound: tokenized money is not a replacement for fiat it is a natural extension of it. Just as banks extended from paper ledgers to digital core systems, the modern bank must now extend from fiat-only infrastructure to infrastructure that natively supports stablecoins, tokenized deposits, and future forms of digital currency. The institutions that thrive will not be those that treat each new form of money as a separate initiative. They will be those that build a unified operating system capable of treating every new innovation as a natural extension of what already exists.

The current global financial infrastructure is built on a series of fragmented, message-based systems that rely on bilateral reconciliation a model that is fundamentally incompatible with the instant, 24/7, and programmable nature of tokenized money. To survive the next decade, financial institutions must abandon the strategy of bolting on point solutions and instead adopt a unified operating system (OS) infrastructure that can orchestrate fiat, stablecoins, and tokenized deposits through a single, composable platform.

This week’s reports

1️⃣Who Pays for Payments?

2️⃣The $400T Future of Tokenised Assets

3️⃣Everything, Everywhere is Compliance

4️⃣State of AI in FinTech

5️⃣Can Blockchain Decentralise Money, Contracts, and Finance?

6️⃣Mapping the Top 100 Stablecoins and Their Future

7️⃣The State of Tokenization

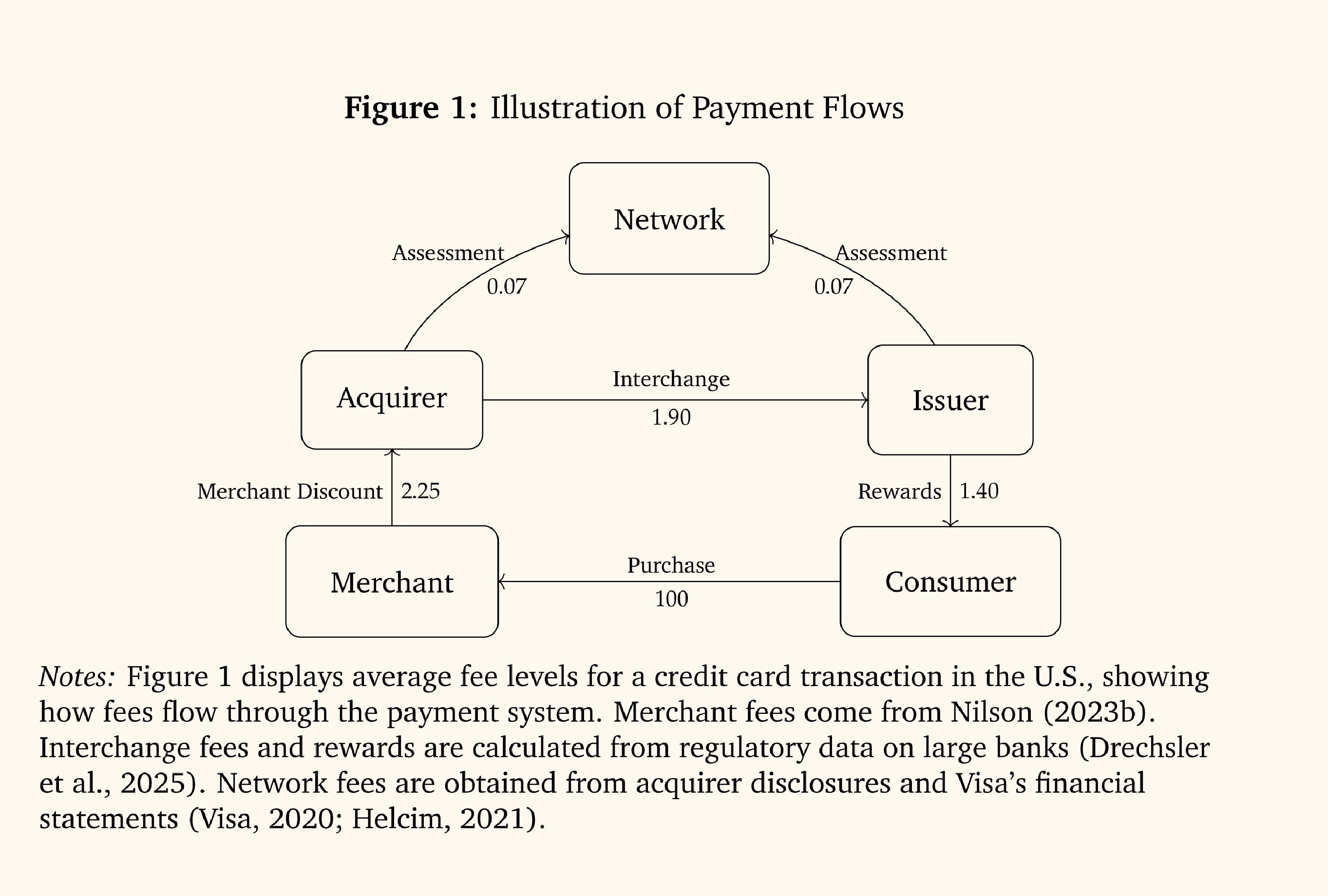

Who Pays for Payments?

The payment system was never just a transaction layer. It became one of the largest hidden redistribution systems in finance.

A new Harvard Business School paper built on merchant-level data from roughly 1 million U.S. merchants and 800,000 Clover POS businesses shows how interchange fees quietly move purchasing power across consumers depending on how they pay.

The headline number is massive.

Researchers estimate around $30 billion annually flows from cash and debit users toward credit card users through interchange economics and rewards structures. Higher-income households capture a disproportionate share because premium credit card usage rises with income.

What makes this interesting is that the mechanism is more complex than the standard “merchants pay fees, consumers get rewards” narrative.

The paper argues redistribution depends on where people shop and what payment methods dominate inside those merchants. Grocery stores, gas stations, travel merchants, premium retail, large chains, and small businesses all face different interchange economics. Some large merchants negotiate materially lower fees while smaller merchants absorb higher costs.

That changes how the burden spreads across the economy.

Keep reading with a 7-day free trial

Subscribe to Fintech Wrap Up to keep reading this post and get 7 days of free access to the full post archives.