Deep Dive: Tokenized Money Validates the Need for Unified Bank OS Infrastructure

The transition from traditional fiat messaging to tokenized asset execution represents the most significant architectural shift in the history of financial services. This evolution marks the end of the era of the ledger as a passive database and the beginning of the ledger as an active, programmable operating system.

The key insight driving this shift is simple but profound: tokenized money is not a replacement for fiat it is a natural extension of it. Just as banks extended from paper ledgers to digital core systems, the modern bank must now extend from fiat-only infrastructure to infrastructure that natively supports stablecoins, tokenized deposits, and future forms of digital currency. The institutions that thrive will not be those that treat each new form of money as a separate initiative. They will be those that build a unified operating system capable of treating every new innovation as a natural extension of what already exists.

The current global financial infrastructure is built on a series of fragmented, message-based systems that rely on bilateral reconciliation a model that is fundamentally incompatible with the instant, 24/7, and programmable nature of tokenized money. To survive the next decade, financial institutions must abandon the strategy of bolting on point solutions and instead adopt a unified operating system (OS) infrastructure that can orchestrate fiat, stablecoins, and tokenized deposits through a single, composable platform.

The structural failure of legacy banking cores

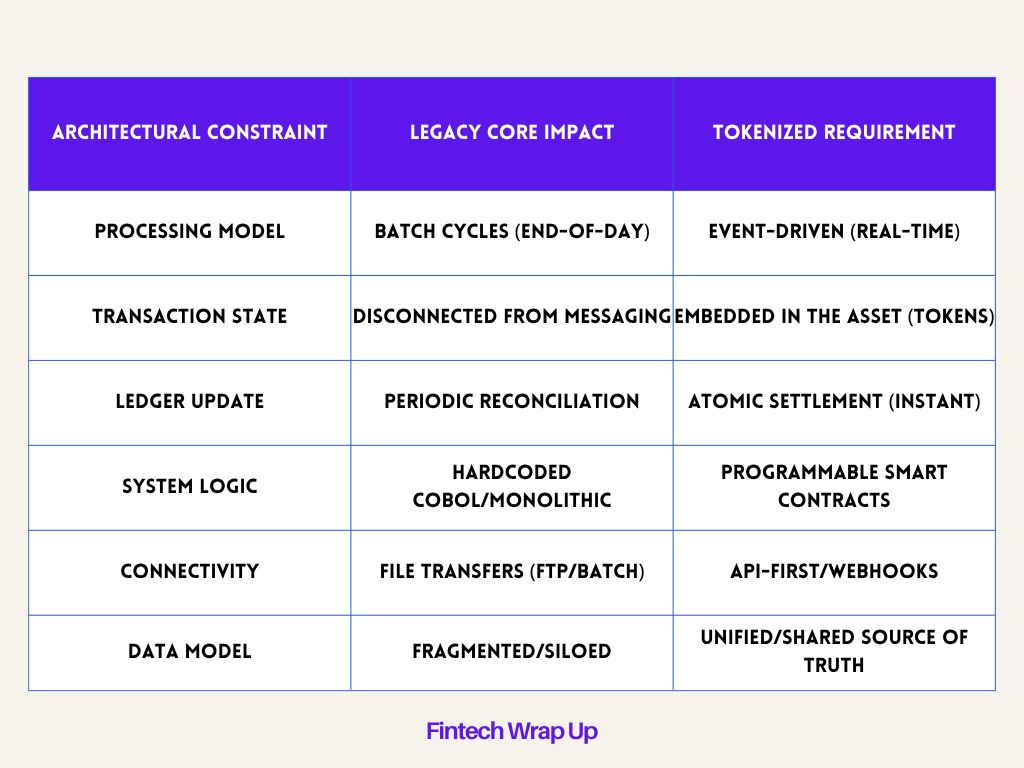

The legacy core banking system is the primary obstacle to the adoption of tokenized money. These systems, many of which were architected in the 1970s and 1980s, were designed for an era of physical branches, paper checks, and overnight batch processing. They operate on the principle of ‘delayed state,’ where the record of a transaction is updated long after the payment instruction is initiated. This architecture is inherently flawed in a tokenized environment where the asset and the ledger are one and the same.

The problem of batch processing

Batch-oriented systems create a ‘liquidity lag’ that increases counterparty risk and operational friction. In a traditional system, a transaction must pass through a sequence of messages, reconciliations, and legal confirmations across multiple institutions before finality is achieved. This process is not only slow but also opaque, as participants often have incomplete information about the end-to-end transaction state.

The technical debt associated with these systems is staggering. Research indicates that approximately 90% to 95% of bank IT spending is consumed by the maintenance of legacy infrastructure rather than innovation. This resource drain prevents institutions from developing the high-speed data pipelines required for digital money. Furthermore, the lack of native API support in legacy cores necessitates the creation of complex middleware wrappers that add latency and create new points of failure.

The integration debt

Integrating blockchains with legacy systems is not a simple matter of cabling two databases together. Blockchains are deterministic and operate in a closed loop to ensure consensus. They cannot natively make API calls to a bank’s server to confirm a payment without reintroducing the single point of failure that the blockchain was designed to eliminate. This is known as the ‘Oracle Problem’.

When banks attempt to solve this by adding isolated tokenization modules, they create ‘integration debt.’ These point solutions often rely on asynchronous data ingestion and manual bridging mechanisms that are structurally insufficient in synchronous, real-time markets. The result is a proliferation of siloed tools and brittle pipelines that collapse under the weight of real-world complexity.

How banks are approaching tokenized money

As tokenized money moves from experimentation to production, banks are taking markedly different approaches. Understanding this landscape is essential because the infrastructure challenge each approach creates is converging on the same bottleneck.

The first group is doing nothing. These institutions are in a wait-and-see mode, sticking to the status quo while monitoring how the regulatory and competitive environment evolves. For now, this is a defensible position. It will not remain one for long.

The second group is moving to stablecoins alone. These banks recognize that stablecoins particularly USDC represent the path of least resistance. They are already established, widely accepted, and enable 24/7 programmable dollar transfers. For cross-border payments in particular, stablecoins eliminate costly intermediaries and foreign exchange friction.

The third group consists of the largest institutions JPMorgan, Citi, and a handful of others that have the scale and balance sheet to issue their own proprietary tokenized deposits. JPMorgan’s evolution from JPM Coin (a private-chain token for internal transfers) to JPMD (a tokenized deposit issued on public Layer 2 networks) illustrates the strategic direction: moving from liquidity islands toward institutional DeFi on public rails.

The fourth and largest group is forming consortia. Across the United States, banks are clustering by size to issue tokenized deposits collectively. The Clearing House (TCH) has brought together the largest names JPMorgan, Citi, Wells Fargo, and others to form a shared issuance network. Smaller banks have coalesced around the Hazel Network. Mid-sized institutions are forming the Cari Network. A similar dynamic is playing out in the United Kingdom, where major banks and the central bank are coordinating on interoperability standards.

The fragmentation problem

Here is the challenge every consortium creates: tokenized deposits issued within one network only function within that network. If a corporate treasurer’s bank is on Cari Network and their counterparty’s bank is on TCH, the tokenized deposit still does not work across that boundary. Each consortium solves the problem for its members while creating a new version of the same problem at the network edge.

The result is an increasingly fragmented ecosystem multiple networks, multiple issuers, multiple asset types, each operating according to different standards and settlement models. This fragmentation mirrors a pattern banking has seen before: when new payment networks emerged, many institutions rushed to connect, only to find that participation did not automatically translate into operational readiness. Access to a network is not the same as the ability to operate effectively within it.

What banks actually need is not a choice between consortia it is infrastructure capable of operating across all of them simultaneously. This requires two things: multi-issuer support (the ability to receive, hold, and settle tokenized deposits issued by different networks) and multi-asset support (the ability to manage fiat, stablecoins, and tokenized deposits within a single operational model). Without this, every new consortium a bank joins adds complexity rather than capability. Banks should keep these factors in mind as they prepare for the inevitable challenge of coexisting in a consortium-driven ecosystem.

The unified ledger

The Bank for International Settlements (BIS) has proposed the ‘Unified Ledger’ as the foundational infrastructure for the future monetary system. This concept represents a shift from fragmented networks to a shared programmable platform where tokenized central bank money, commercial bank deposits, and real-world assets reside on the same network.

The mechanics of executable objects

The unified ledger replaces passive records with ‘executable objects’ or tokens. These tokens integrate the record of the underlying asset with the specific rules and logic governing its transfer. This dual nature allows for ‘composability,’ where multiple transactions can be bundled together and executed automatically based on predefined conditions.

Atomic settlement is the core mechanic of this system. In a unified ledger, the exchange of assets and payments happens simultaneously. If any part of the transaction fails, the entire operation is canceled, ensuring that neither party is left without their funds or their asset. This eliminates the need for manual intervention and the message-passing processes that characterize modern banking.

The three aspects of tokenized assets

The BIS vision centers on a ‘trilogy’ of tokenized assets that together provide the stability, elasticity, and integrity required for a functional monetary system:

Wholesale Central Bank Digital Currency (wCBDC): Acts as the ultimate settlement asset, providing a direct claim on the central bank to ensure interbank settlements occur with zero credit risk.

Tokenized Commercial Bank Deposits: Represent the primary means of payment for the digital economy, retaining the traditional two-tier banking system while adding programmability and real-time settlement.

Tokenized Real-World Assets (RWA): Include digitized versions of bonds, real estate, and commodities that can interact directly with tokenized money on the shared ledger.

The integration of these three components on a single platform allows for the creation of new economic arrangements that were previously impossible due to information and incentive frictions. For example, a smart contract could automatically disburse a dividend payment to thousands of token holders the instant a company’s earnings are verified, or a trade finance transaction could be settled automatically when a digital bill of lading is recorded on-chain.

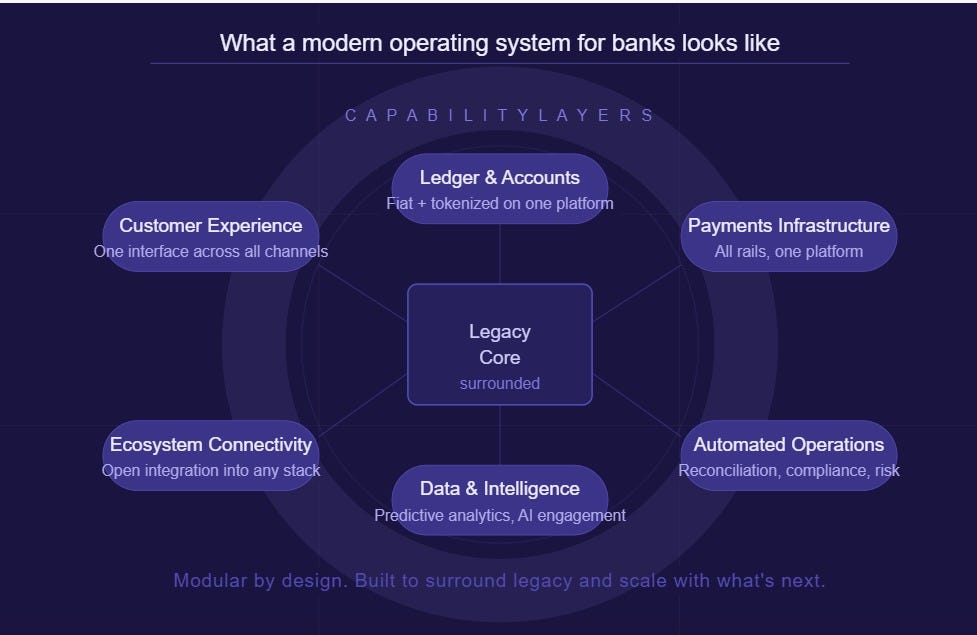

The bank operating system (BankOS) paradigm

To bridge the gap between legacy cores and the unified ledger, financial institutions must adopt a modern ‘Bank Operating System’ (BankOS). A BankOS is a composable, cloud-native infrastructure that surrounds the legacy core with modern capabilities, allowing banks to modernize journey-by-journey without a ‘rip and replace’ of their system of record.

The defining feature of a modern BankOS is simple: every new innovation is absorbed as an extension of the infrastructure already in place. When real-time payments emerged, BankOS evolved to support them as another layer within existing payment rails. Now, as on-chain rails enter the equation, they slot into the very same payment architecture that already processes fiat today. For banks, this changes everything. New innovation no longer means building a new operating model from scratch — the operating system is designed to evolve ahead of change.

Composable infrastructure

Modern platforms like Finzly’s BankOS organize banking functions into specialized modules that deliver specific services independently. This modular approach is essential for preventing the creation of new silos as the bank adopts new payment rails and asset types:

Payment: A unified payment hub that orchestrates all payment rails including ACH, Fedwire, RTP, FedNow, and SWIFT from a single platform, with centralized controls and real-time monitoring.

Account: A real-time virtual account and ledger platform designed to support embedded finance, specialty deposits through virtual accounts including tokenized deposits. It functions as a ‘sidecar core’ or 24/7 shadow ledger, maintaining sub-second balance updates that the legacy core cannot handle.

Token: Specifically designed for the tokenized economy, this suite unifies traditional and tokenized rails managing fiat, stablecoins, and tokenized deposits on a single platform with the flexibility to connect to multiple blockchains, issuers, and consortia simultaneously. It means new asset classes seamlessly integrate into existing account infrastructure, while on-chain connectivity becomes just another extension of the payment systems banks already rely on today.

The logic of the sidecar core

The ‘sidecar core’ strategy allows a bank to launch new products such as instant payments or tokenized deposits in weeks rather than years. By running a modern ledger (Account) alongside the legacy core, the bank can handle high-volume, real-time operational workloads while the legacy core remains the ultimate system of record for accounting and regulatory purposes.

This architecture provides a path for ‘progressive modernization.’ Over time, more functionality is strangled off the legacy core and provided by modern modules, until the legacy system can eventually be retired without disrupting business continuity.

Tokenized assets: Deposits, Stablecoins, and the On/Off ramp

The landscape of tokenized money is evolving into a spectrum of assets with varying degrees of trust, regulation, and utility. A unified OS must be capable of managing all these assets within a single operational environment and critically, providing intelligent movement between them.

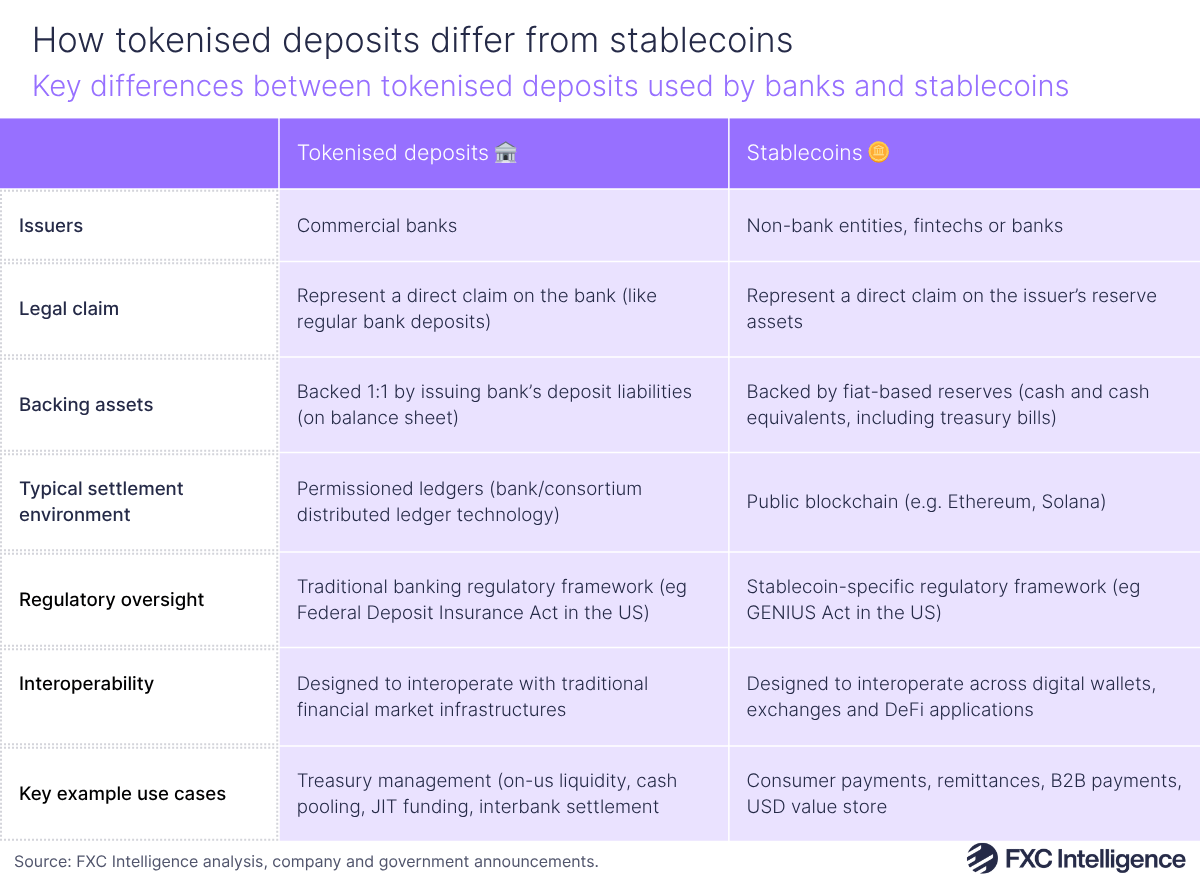

Tokenized Deposits vs. Stablecoins

Tokenized deposits are the digital extension of a bank’s existing liabilities. They preserve the two-tier monetary system and benefit from existing regulatory frameworks, such as deposit insurance and central bank liquidity. Crucially, tokenized deposits earn interest making them attractive to corporate treasurers who need yield alongside speed.

Stablecoins, conversely, are typically issued by private entities and backed by reserves of cash or short-term securities. They have proven the demand for 24/7 programmable dollars, particularly for cross-border payments. A corporate treasurer moving funds to a counterparty in China, for example, can use USDC to avoid cross-border fees and correspondent banking friction entirely. However, under the U.S. GENIUS Act, stablecoin deposits cannot earn interest a meaningful limitation for treasury operations where yield matters.

The practical reality is that neither asset wins outright. Treasurers will hold stablecoins for cross-border payment velocity and hold tokenized deposits for yield and speed within the domestic banking system. Banks need infrastructure that can operate across both.

The intelligent On/Off ramp

This is where the infrastructure challenge becomes concrete. Banks need the ability to move fluidly between fiat, stablecoins, and tokenized deposits automatically and intelligently. When a client needs to convert fiat to stablecoins for a cross-border transfer, the platform must coordinate the fiat debit in the legacy ledger and the on-chain minting of the token in a single, synchronized workflow. When conditions favor tokenized deposits (for yield), the system should be able to sweep funds between asset types automatically.

Finzly’s Token Galaxy platform addresses this by coordinating the bridging between traditional and tokenized money automatically. But the key architectural requirement goes beyond any single bridge: the platform must support on-ramp and off-ramp between multiple asset types simultaneously, route intelligently based on cost, speed, and yield, and handle multiple issuers across multiple consortia all from a single operational model.

The programmability of JPMD

JPMorgan’s evolution from JPM Coin to JPMD illustrates the strategic shift toward public-rail interoperability. JPM Coin was a digital deposit token used for moving funds faster than traditional rails allowed, but it was limited to the bank’s internal, private blockchain (Onyx/Kinexys). This created a ‘liquidity island’ where assets could not interact with the broader $4 trillion daily repo market.

The launch of JPMD a tokenized version of a bank deposit issued on public Layer 2 networks like Base marks a shift toward ‘Institutional DeFi.’ JPMD allows the dollar on-chain to behave exactly like a dollar in the bank, providing the protection expected by institutions while enabling the speed and programmability of public blockchains.

Programmable treasury

Much of today’s discussion focuses on payments. Treasury may ultimately be the larger opportunity.

Once money becomes programmable, liquidity becomes programmable. Treasury becomes programmable. Consider what becomes possible when a bank operates across fiat, stablecoins, and tokenized deposits through a unified infrastructure:

Automatic movement between operating accounts and yield-bearing tokenized deposits based on real-time balance thresholds

Real-time liquidity optimization across multiple entities and currencies

Instant cross-border liquidity movement using stablecoins, without correspondent banking delays or fees

Dynamic funding decisions that respond to market events rather than scheduled windows

Continuous cash positioning rather than end-of-day reconciliation

For corporate clients, this is far more compelling than simply moving money faster. It changes how cash is managed. And banks that can offer programmable treasury backed by multi-asset, multi-rail infrastructure are uniquely positioned to capture this opportunity.

The Architectural Blueprint: Two Foundational Capabilities

To treat tokenized deposits or stablecoins as isolated payment rails is an architectural failure. Digital assets must be treated as a natural, seamless extension of existing fiat assets. A modern Bank Operating System (BankOS) must deliver two foundational, non-negotiable capabilities to achieve this integration :

1. A Unified Ledger

As the variety of asset types expands, maintaining separate databases for fiat and digital liabilities becomes operationally impossible. The future bank requires a unified ledger, a single, real-time source of truth capable of managing fiat deposits, tokenized deposits, stablecoins, treasury positions, and liquidity balances.

This is not merely an accounting exercise. A unified ledger simplifies reconciliation, strengthens compliance controls, improves audit readiness, and ensures the bank can adopt new forms of money without rebuilding its core infrastructure every time a new asset emerges.

2. A Unified Money Movement Engine

While the unified ledger serves as the system of record, the money movement engine acts as the system of execution. Its purpose is to move value across any network through a common framework. Whether money travels through legacy rails (ACH, Wire), instant rails (RTP, FedNow), or digital rails (stablecoins, tokenized deposit networks, and blockchain settlement layers), the bank must manage routing, compliance, liquidity, and reporting from a single operational console.

When these two capabilities are unified, the real opportunity of programmable money shifts from basic payments to advanced treasury orchestration. Corporate clients gain access to automated cash positioning, real-time cross-border liquidity optimization, and dynamic funding decisions that respond automatically to events rather than rigid banking schedules.

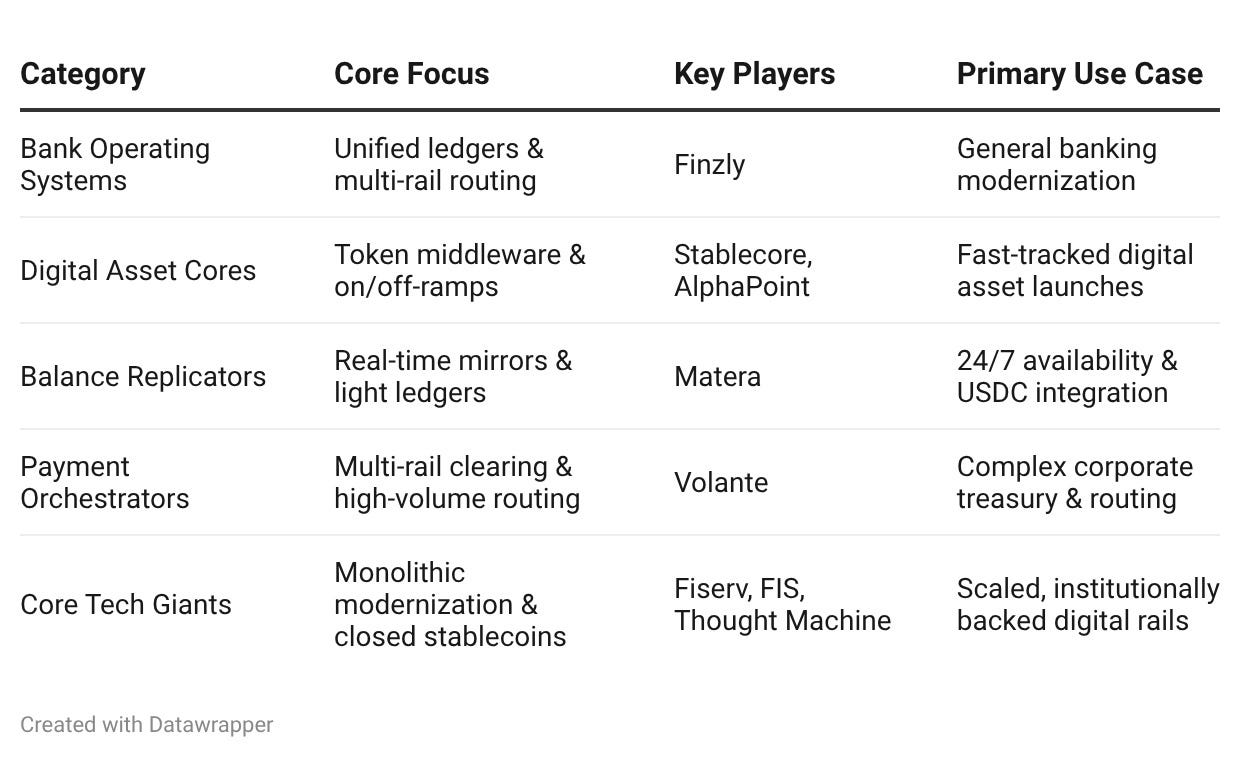

Platform vs. Point Solutions

The current technology market remains highly fragmented. Most vendors focus on a single piece of the architecture, forcing banks to act as systems integrators.

Payments platforms solve routing, ledger platforms solve balance replication, and digital asset providers solve token minting. This piecemeal approach increases integration debt and operational risk.

The following matrix evaluates the primary technology providers against the requirements of a unified money operating system:

The data indicates that banks must move away from point solutions toward a comprehensive platform strategy. Point systems cannot handle the orchestration requirements of a multi-rail, multi-asset financial environment.

The adoption of a unified OS for tokenized money is not merely a technical upgrade; it is a strategic mandate driven by clear economic incentives.

Capital efficiency and liquidity optimization

The move from T+1 or T+2 settlement to T+0 or instant settlement has a massive impact on capital efficiency. Traditional settlement windows tie up billions of dollars in liquidity to manage settlement risk. By utilizing tokenization, institutions can free up capital nearly instantaneously. JPMorgan’s Kinexys platform has demonstrated a 30% reduction in intraday liquidity needs for its participants.

Operational cost reduction

A unified platform reduces operational complexity by removing messaging silos and the need for manual reconciliation between separate databases. In 2023, Goldman Sachs reported that 20% of their repo operations staff were solely dedicated to handling trade breaks and mismatches. On a blockchain ledger, where all parties view the same source of truth, these discrepancies are eliminated entirely.

Finzly reports that its unified payment hub can achieve a 60% cost reduction in payment processing operations with a Straight Through Processing (STP) rate of more than 99%. Furthermore, tokenization can automate regulatory reporting, which JPMorgan estimated could reduce compliance reporting costs for repo transactions by up to 70%.

Revenue growth through embedded finance

Legacy cores were never designed for the emerging embedded banking segment, where fintechs and non-bank platforms embed banking services directly into their customer journeys. A modern BankOS, such as Account, allows banks to generate unlimited virtual accounts programmatically, enabling them to compete for corporate and small-business customers who expect integrated financial services.

By using tokenization to fractionalize assets like private credit or real estate, banks can also unlock new revenue opportunities in traditionally illiquid markets. Fractionalization lowers the minimum investment size, allowing a broader pool of investors to access institutional-grade assets, thereby increasing market liquidity and transaction volume.

Escaping ‘Pilot Loop’

Despite the clear benefits of tokenized money, many banks are stuck in ‘pilot loop’ running dozens of isolated experiments that never scale into production. An MIT study from August 2025 found that 95% of enterprise AI and digital asset pilots fail to deliver measurable financial impact.

The failure of efficiency-only portfolios

Most institutions approach innovation through a narrow efficiency lens, focusing on cost reduction rather than growth or resilience. This results in an unbalanced portfolio of use cases that cannot justify the high upfront cost of new infrastructure. The banks seeing the greatest returns are those that have built balanced portfolios spanning growth (embedded finance), efficiency (automated reconciliation), and resilience (real-time risk monitoring).

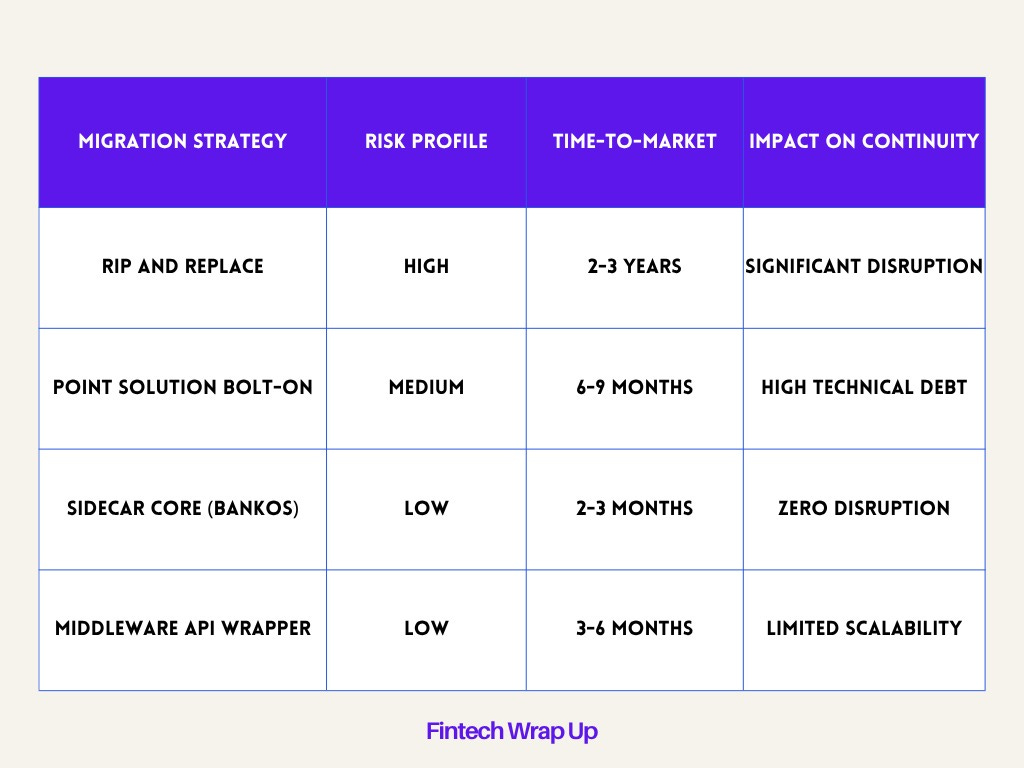

The ‘Tractable Wedge’ strategy

Rather than a full core replacement, successful banks are using ‘tractable wedges’ small, contained deployments that run alongside existing systems:

Shadow Mode Decisioning: The new OS runs in parallel with the legacy core, receiving the same live production data and logging its decisions without executing them. This allows the bank to build the empirical record required for regulatory approval with zero production risk.

Progressive Migration: Once the new system consistently outperforms the legacy core, the bank can gradually ramp traffic via canary deployments.

The transition to tokenized money requires a shift in governance models. Traditional systems rely on institutional buffers and legal processes to manage failure. Tokenized systems rely on the correctness, resilience, and governance of code. This necessitates the creation of ‘AI and DLT Control Towers’ that provide explainability, human-in-the-loop controls, and immutable audit trails.

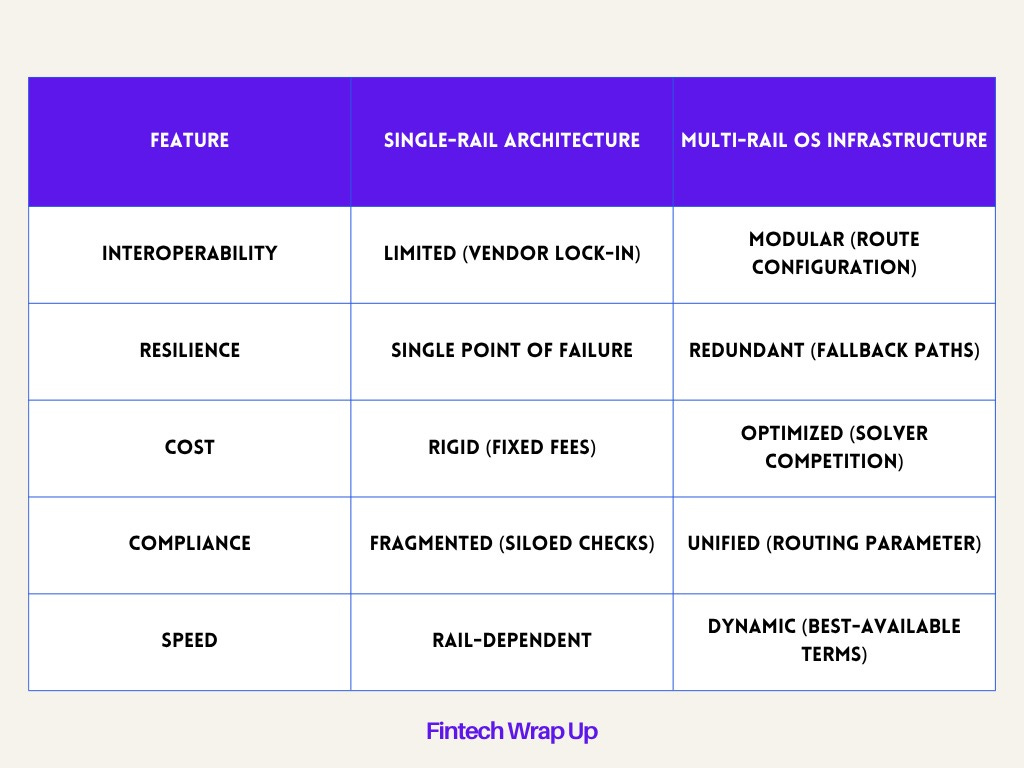

Multi-rail money movement

The future of payments is not the replacement of traditional rails with blockchain, but the coordination of multiple rails within a unified system. Modern fintech founders should view payment rails as evolutionary layers:

Traditional Rails (ACH/SWIFT): Function like domestic road networks or global shipping routes reliable but slow and complex.

Modern Rails (RTP/FedNow): Focus on real-time availability and open connectivity.

Emerging Rails (Blockchain/Stablecoin/Tokenized Deposit Networks): Resemble autonomous air corridors decentralized, borderless, and continuously available.

A multi-rail strategy provides redundancy, cost optimization, and speed flexibility. Instead of building custom integrations for each rail, banks can publish a ‘standardized intent’ and let the OS infrastructure route it optimally across fiat rails, stablecoin networks, and tokenized deposit consortia simultaneously.

Risk mitigation in the tokenized economy

The rapid growth of digital assets introduces substantial risks that a unified OS must be equipped to handle.

Banks’ heavy reliance on technology makes them vulnerable to coding bugs in smart contracts and the potential compromise of digital wallets or private keys. A unified OS must implement robust security measures, including Multi-Party Computation (MPC) for key management, Hardware Security Modules (HSM), and 256-bit encryption.

MPC is particularly critical for institutional custody, as it ensures that the private key is never assembled in a single location. Instead, key shares are distributed across multiple parties, and signatures are computed collaboratively, eliminating any single point of compromise.

The inclusion of crypto into traditional finance introduces potential volatility and contagion. As on-chain transactional activity increases in size and complexity, stablecoins may pose risks to monetary policy and credit intermediation if they are not adequately regulated. By using tokenized deposits which are subject to existing bank capital and liquidity requirements institutions can mitigate these stability risks. The GENIUS Act’s restriction on stablecoin interest-bearing accounts reflects this regulatory concern, reinforcing why tokenized deposits represent the more durable long-term form of bank money in the digital economy.

The mandate for a unified Banking OS

Tokenized money is not a separate innovation silo. It is the next logical extension of digital recordkeeping and value transfer as natural a progression as the move from paper ledgers to core banking systems, or from batch payments to real-time rails.

The banking industry is converging on a world where traditional deposits, real-time payments, tokenized deposits, stablecoins, and future central bank digital currencies all coexist. The challenge is not deciding which form of money wins. The challenge is building infrastructure capable of operating across all of them simultaneously.

Banks that approach each new form of money as a separate project, a separate technology, a separate operating model will find themselves overwhelmed by complexity as the ecosystem fragments further. Banks that build a unified operating system will find that every new consortium, every new asset type, and every new regulation becomes a natural extension of infrastructure they already have.

A modern Bank Operating System, characterized by composable infrastructure, real-time ledgering, multi-issuer and multi-asset support, and intelligent on/off ramp capabilities, provides the only viable path to modernize without disruption. The era of the point solution is over. The era of the unified banking OS has begun.

Sources

III. Blueprint for the future monetary system: improving the old ..., accessed May 10, 2026, https://www.bis.org/publ/arpdf/ar2023e3.htm

Understanding the BIS Unified Ledger | Chainlink, accessed May 10, 2026, https://chain.link/article/bis-unified-ledger

What are Legacy Core Banking Systems? The Complex Nightmare - Baseella, accessed May 10, 2026, https://baseella.com/kb/what-are-legacy-core-banking-systems/

Multi-Rail Payments Infrastructure: Unifying Fiat and Stablecoins - Modern Treasury, accessed May 10, 2026, https://www.moderntreasury.com/journal/fiat-stablecoins-multi-rail-infrastructure

Finzly Unveils Token Galaxy: Unifying Money Movement for Traditional and Tokenized Banking - PR Newswire, accessed May 10, 2026, https://www.prnewswire.com/news-releases/finzly-unveils-token-galaxy-unifying-money-movement-for-traditional-and-tokenized-banking-302710960.html

Finzly Unveils Token Galaxy: Unifying Money Movement for Traditional and Tokenized Banking, accessed May 10, 2026, https://finzly.com/resources/press-releases/finzly-unveils-token-galaxy-unifying-money-movement-for-traditional-and-tokenized-banking/

Tokenized Deposits & Stablecoins Platform for Banks - Finzly, accessed May 10, 2026, https://finzly.com/solutions/tokenized-deposits/

Why Your Legacy Banking System is Holding You Back (And How to Fix It), accessed May 10, 2026, https://www.abbacustechnologies.com/why-your-legacy-banking-system-is-holding-you-back-and-how-to-fix-it/

The Future of Core Banking Systems: Architecture & Modernization - KMS Technology, accessed May 10, 2026, https://kms-technology.com/blog/core-banking-system/

SoK of RWA Tokenization: A Systematization of Concepts, Architectures, and Legal Interoperability - arXiv, accessed May 10, 2026, https://arxiv.org/html/2604.06608v1

JP Morgan made a huge deal with tokenized repos...so how did it go? - Substack, accessed May 10, 2026,

Tokenized Finance; IMF Notes No. 26/01; April 2026, accessed May 10, 2026, https://www.imf.org/-/media/files/publications/imf-notes/2026/english/insea2026001.pdf

Tokenized cash: A regulatory view of unlocking a digital financial market | State Street, accessed May 10, 2026, https://www.statestreet.com/pl/en/insights/digital-digest-december-2024-regulatory-update-tokenization

Legacy Systems vs. Modern Systems in Banking - KITRUM, accessed May 10, 2026, https://kitrum.com/blog/legacy-vs-modern-systems/

Virtual Account Management Platform | Real-Time Ledger System ..., accessed May 10, 2026, https://finzly.com/account-galaxy/

Three strategic mistakes that keep banks stuck in AI pilot mode - The Wealth Mosaic, accessed May 10, 2026, https://www.thewealthmosaic.com/vendors/backbase/blogs/three-strategic-mistakes-that-keep-banks-stuck-in-/

# AI Core Banking Integration: Strategies That Scale - Backbase, accessed May 10, 2026, https://www.backbase.com/blog/core-banking-integration

Blockchain Legacy System Integration Guide - Chainlink, accessed May 10, 2026, https://chain.link/article/blockchain-legacy-system-integration

Point Solutions or an Integrated Platform? - LexisNexis Risk Solutions, accessed May 10, 2026, https://risk.lexisnexis.com/insights-resources/article/point-solutions-or-an-integrated-platform

Digital Assets and Digital Market Infrastructure – A Structural Shift in Treasury and Capital Markets - Banking.Vision, accessed May 10, 2026, https://banking.vision/en/digital-assets-and-digital-market-infrastructure/

Legacy Payment Systems : 4 Important Bridging Strategies - Host Merchant Services, accessed May 10, 2026, https://hostmerchantservices.com/articles/legacy-payment-systems/

From Pilots to Production: How Banks Are Building With AI - Oscilar, accessed May 10, 2026, https://oscilar.com/blog/aibank

Next-generation monetary and financial system takes shape, based on a tokenised unified ledger: BIS - Bank for International Settlements, accessed May 10, 2026, https://www.bis.org/press/p250624.htm

Tokenization and Unified Ledger: Building the Future Monetary System | Gate Learn, accessed May 10, 2026, https://www.gate.com/learn/articles/from-digitization-to-tokenization-the-unified-ledger-is-building-a-grand-blueprint-for-future-currency/1311

Tokenization architecture: Components, patterns, and integration decisions - Nextrope, accessed May 10, 2026, https://nextrope.com/tokenization-architecture-components-patterns-and-integration-decisions

Digital Banking System | Business & Consumer Banking - Finzly, accessed May 10, 2026, https://finzly.com/digital-galaxy/

Award-winning banking solutions for BaaS, Payments, Treasury & FX, accessed May 10, 2026, https://finzly.com/

Finzly Launches Account Galaxy: Embedded Banking Solution with Virtual Account and Virtual Ledger Capabilities, accessed May 10, 2026, https://finzly.com/resources/press-releases/finzly-launches-account-galaxy-embedded-banking-solution-with-virtual-account-and-virtual-ledger-capabilities/

How to Identify the Payment Hub That’s Right for Your Financial ..., accessed May 10, 2026, https://finzly.com/resources/blogs/how-to-identify-the-payment-hub-thats-right-for-you/

Payment Rails Explained: The Infrastructure Powering Money Movement - SDK.finance, accessed May 10, 2026, https://sdk.finance/blog/payment-rails-explained-the-infrastructure-powering-money-movement/

Tokenized Payments Platform for Banks | Deposits & Stablecoins - Finzly, accessed May 10, 2026, https://finzly.com/token-galaxy/

Banks ditching point solutions: 5 reasons to unify platforms - Backbase, accessed May 10, 2026, https://www.backbase.com/blog/unified-banking-platform-benefits

AI-native banking OS vs AI-powered platform - Backbase, accessed May 10, 2026, https://www.backbase.com/blog/ai-native-vs-ai-powered-banking-platform

Core Banking Platforms Compared: Features, Pricing, and Integration Ease | Gemba, accessed May 10, 2026, https://ge.mba/research/core-banking-platforms-compared-features-pricing-and-integration-ease

Tokenized Deposits: Models, Use Cases & Infrastructure - Kaleido, accessed May 10, 2026, https://www.kaleido.io/blockchain-blog/tokenized-deposits-models-use-cases-infrastructure

A foundation for stable digital money - J.P. Morgan, accessed May 10, 2026, https://www.jpmorgan.com/kinexys/documents/deposit-tokens.pdf

Chiara Scotti: Digital money and the architecture of trust - Bank for International Settlements, accessed May 10, 2026, https://www.bis.org/review/r260505d.pdf

III. The next-generation monetary and financial system - Bank for International Settlements, accessed May 10, 2026, https://www.bis.org/publ/arpdf/ar2025e3.htm

Breaking Down JPMD, JPM Coin, and Stablecoins - WhiteSight, accessed May 10, 2026, https://whitesight.net/infographics/breaking-down-jpmd-jpm-coin-and-stablecoins/

It’s Time to Explore Institutional DeFi - Oliver Wyman Forum, accessed May 10, 2026, https://www.oliverwymanforum.com/future-of-money/2022/Nov/institutional-defi.html

Compliance Automation in Blockchain Markets - Chainlink, accessed May 10, 2026, https://chain.link/article/blockchain-compliance-automation

Compliance is the new payments rail - Lisk - The Growth Platform for EM Founders, accessed May 10, 2026, https://lisk.com/blog/posts/compliance-is-the-new-payments-rail/

Compliance-Aware Agentic Payments on Stablecoin Rails - arXiv, accessed May 10, 2026, https://arxiv.org/html/2605.00071v1

Onchain KYC: Identity and Compliance for Smart Contracts - Chainlink, accessed May 10, 2026, https://chain.link/article/onchain-kyc

Blockchain KYC: How It Works and Use Cases - Chainlink, accessed May 10, 2026, https://chain.link/article/blockchain-kyc

Advanced Digital Identity Orchestration Engine for Privacy-Preserving KYC Verification | Request PDF - ResearchGate, accessed May 10, 2026, https://www.researchgate.net/publication/400289457_Advanced_Digital_Identity_Orchestration_Engine_for_Privacy-Preserving_KYC_Verification

Why JPMorgan Started Kinexys: The Case for Blockchain in Institutional Settlements, accessed May 10, 2026, https://www.bastion.com/blog/why-jpmorgan-started-kinexys-the-case-for-blockchain-in-institutional-settlements

Tokenization in financial services: Delivering value and transformation - PwC, accessed May 10, 2026, https://www.pwc.com/us/en/tech-effect/emerging-tech/tokenization-in-financial-services.html

Debt Tokenization: A Guide to Onchain Credit | Chainlink, accessed May 10, 2026, https://chain.link/article/debt-tokenization

Key differences between tokenized real-world assets vs traditional securities - MetaMask, accessed May 10, 2026, https://metamask.io/news/tokenized-real-world-assets-vs-traditional-securities

Decoding Tokenization Costs: Converting Real World Assets To RWA Tokens - InvestaX, accessed May 10, 2026, https://investax.io/blog/asset-tokenization-costs

Builder’s Guide to Multi-Rail Money Movement - Modern Treasury, accessed May 10, 2026, https://www.moderntreasury.com/journal/a-builder-s-guide-to-multi-rail-money-movement

Payment Rails in Smart Contract as a Service (SCaaS) Solutions from BPMN Models - MDPI, accessed May 10, 2026, https://www.mdpi.com/1999-5903/18/2/110

Stablecoin Payment Rails in 2026: Why Enterprises Are Choosing Multi-Rail Over Vendor Lock-In | Support, accessed May 10, 2026, https://eco.com/support/en/articles/14465844-stablecoin-payment-rails-in-2026-why-enterprises-are-choosing-multi-rail-over-vendor-lock-in

American Banker Report: Setting the Stage for Tokenized Money - Finzly, accessed May 10, 2026, https://finzly.com/resources/industry-insights/american-banker-report-setting-the-stage-for-tokenized-money/

What Is a Unified Treasury Platform? Why a Fiat-Only TMS Is Now a Strategic Liability, accessed May 10, 2026, https://treasury.ripple.com/de/posts/what-is-a-unified-treasury-platform

Digital assets: risks, regulations, mitigation - PMC - NIH, accessed May 10, 2026, https://pmc.ncbi.nlm.nih.gov/articles/PMC12883517/

How Banks Can Mitigate Risks Across the Digital Asset Value Chain - ISG, accessed May 10, 2026, https://isg-one.com/articles/how-banks-can-mitigate-risks-across-the-digital-asset-value-chain

Digital assets and banks: A shifting regulatory and risk landscape - WTW, accessed May 10, 2026, https://www.wtwco.com/en-ca/insights/2025/11/digital-assets-and-banks-a-shifting-regulatory-and-risk-landscape

Disclaimer:

Fintech Wrap Up aggregates publicly available information for informational purposes only. Portions of the content may be reproduced verbatim from the original source, and full credit is provided with a “Source: [Name]” attribution. All copyrights and trademarks remain the property of their respective owners. Fintech Wrap Up does not guarantee the accuracy, completeness, or reliability of the aggregated content; these are the responsibility of the original source providers. Links to the original sources may not always be included. AI is used to produce some pieces of this article. For questions or concerns, please contact us at sam.boboev@fintechwrapup.com.