Reports: Let's dive into 9 fintech predictions in 2026; From Click to Command: The Shift to Agentic Payments; The Agentic AI Advantage: Finance agents that move the numbers

This week’s reports all point to the same shift: finance is moving toward a more programmable, real-time, and autonomous operating model. Tokenized deposits are presented as a banking infrastructure upgrade rather than a crypto replacement, while stablecoins and CBDCs are emerging as parallel rails in a more controlled monetary stack. At the same time, payments are being shown as fragmented across multiple systems, which makes observability and reconciliation a core challenge. The other major theme is AI agents: they are evolving from tools that recommend actions into actors that can search, negotiate, procure, and pay within defined limits. Taken together, the reports suggest that commerce and finance are converging into a new system where settlement, compliance, and execution happen closer together, and where banks, fintechs, and AI systems all play roles in the same evolving infrastructure.

Video of the Week

Deep Dive of the Week

An Analytical Breakdown of Revolut’s 2025 Performance

The fiscal year 2025 represents a landmark epoch for Revolut, marking a decade of operational existence and a definitive transition from a high-growth fintech disruptor to a globally systemic financial institution. The dual analysis of the firm’s 2025 Annual Report and the independent assessment by Andreessen Horowitz (a16z) reveals a financial profile characterized by “outlier” performance metrics that deviate significantly from both traditional banking incumbents and modern neobank peers. With a reported revenue of £4.5 billion, a 46% year-on-year increase, and a profit before tax of £1.7 billion, representing a 57% surge, Revolut has demonstrated a capacity for compounding efficiency that validates its technology-first operating model. This transition is underpinned by a “Growth Algorithm” that prioritizes product velocity, regulatory statecraft, and extreme operational leverage, resulting in a return on equity that challenges the fundamental assumptions of the consumer finance sector.

This week’s reports

1️⃣Tokenized Deposits Essential to the Future of Digital Finance

2️⃣Stablecoins and the Future of Payments: Evidence from Financial Markets

3️⃣From Click to Command: The Shift to Agentic Payments

4️⃣Building Gulf stablecoins and CBDCs infrastructures Strategy, Scale and Supervision (2026-2030)

5️⃣Let’s dive into 9 fintech predictions in 2026

6️⃣The Agentic AI Advantage: Finance agents that move the numbers

7️⃣Everything to Know About the New Stack for Autonomous Commerce

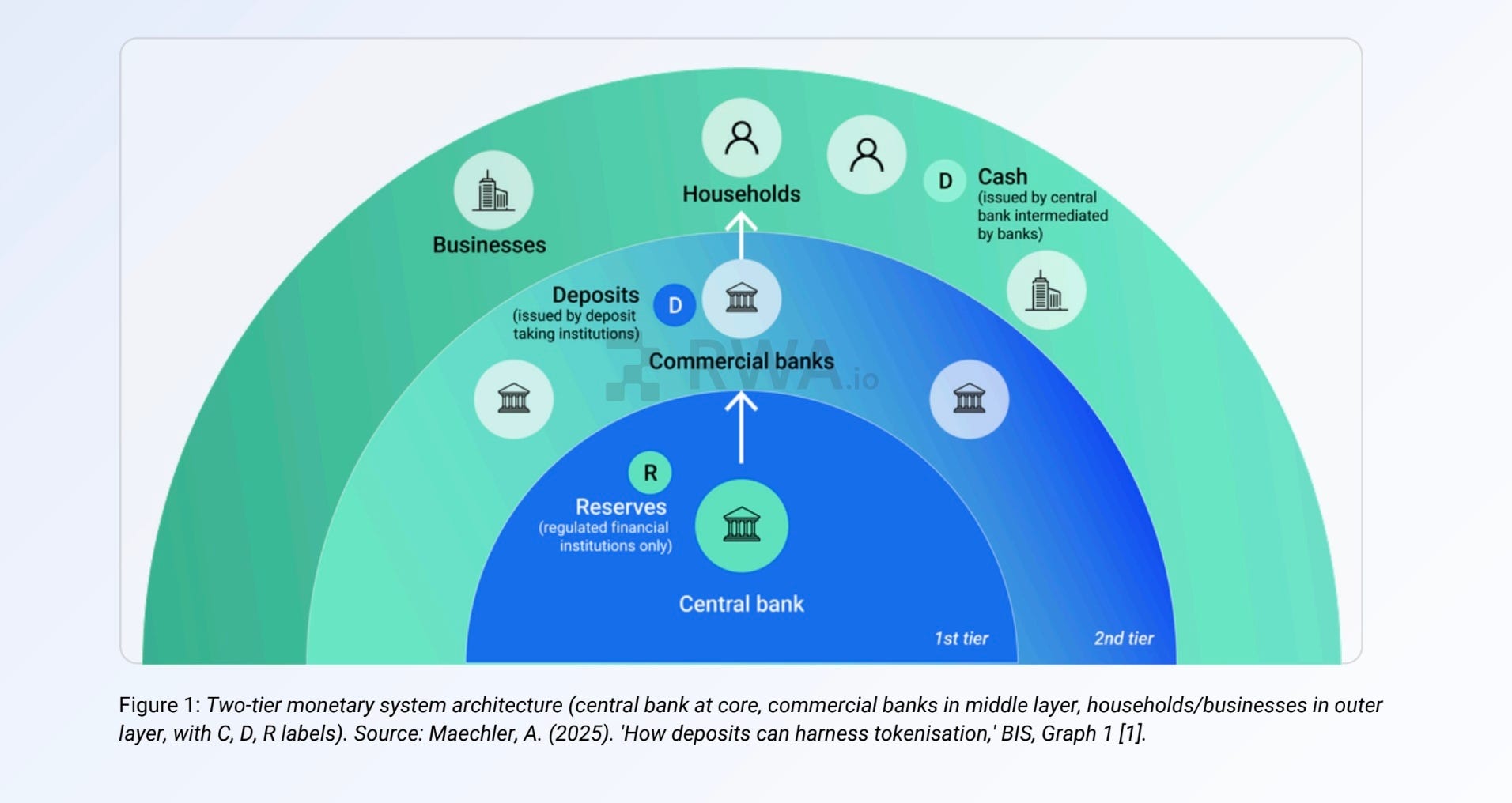

Tokenized Deposits Essential to the Future of Digital Finance

Most people still think tokenized deposits are a crypto story. But I would say they are a banking infrastructure upgrade.

Tokenized deposits are simply commercial bank money represented on a blockchain. The key difference is not what they are, but how they move. They enable 24/7, near real-time settlement with programmable logic, while remaining fully within the regulated banking system.

____

This is why banks are leading, not being disrupted.

Unlike stablecoins, tokenized deposits are direct liabilities of banks, backed by existing deposits, covered by deposit insurance, and governed by the same regulatory frameworks. They preserve the two-tier monetary system instead of bypassing it.

____

The shift is already operational, not theoretical.

J.P. Morgan, Citi, and BNY are running live systems for institutional clients. Corporates are using them for treasury automation, FX, and liquidity management. Transactions that used to take hours or days are executed instantly and programmatically across time zones.

____

The real change is structural.

-> Settlement is collapsing into the same layer as execution.

Keep reading with a 7-day free trial

Subscribe to Fintech Wrap Up to keep reading this post and get 7 days of free access to the full post archives.