Deep Dive: An Analytical Breakdown of Revolut’s 2025 Performance

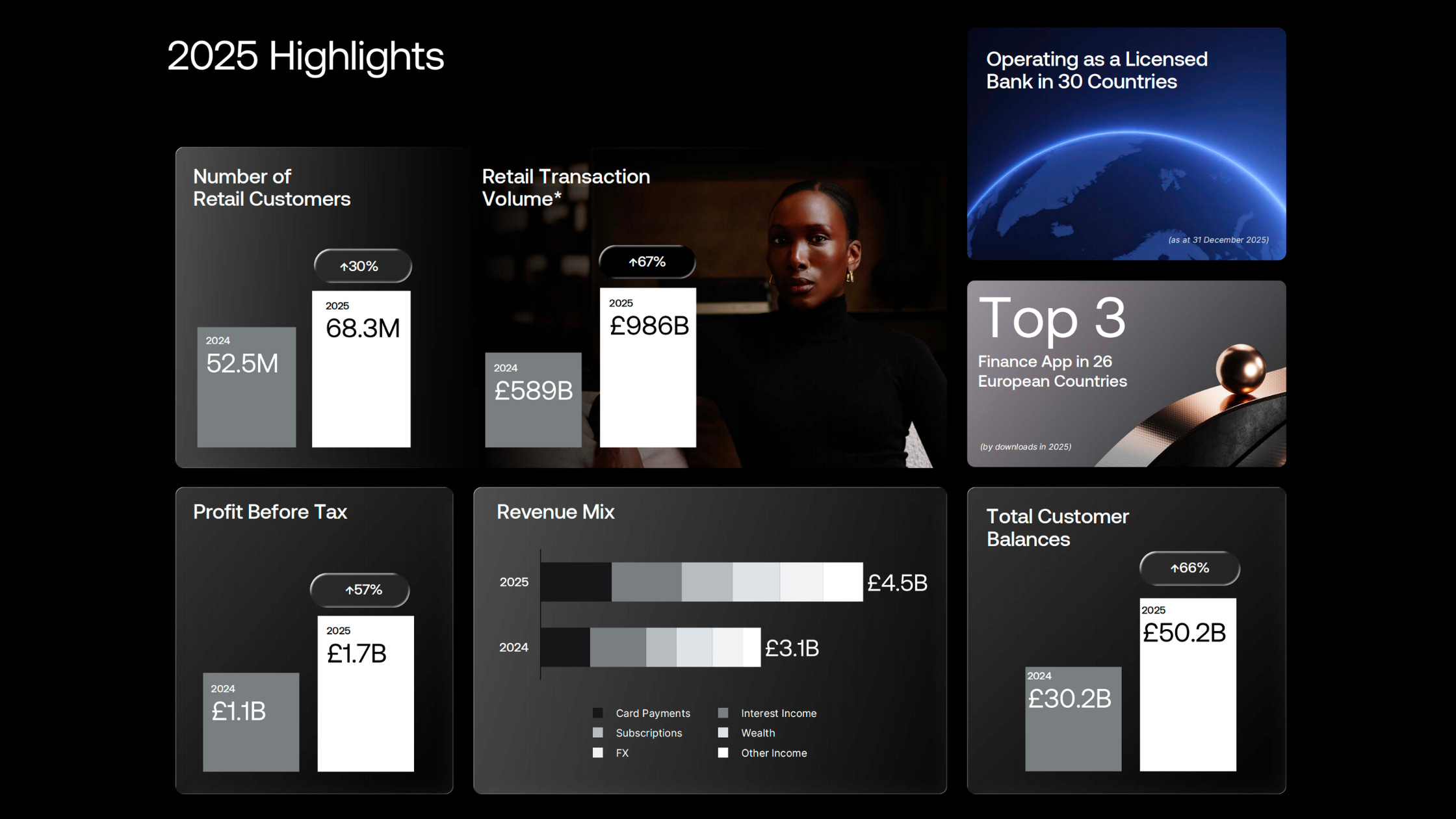

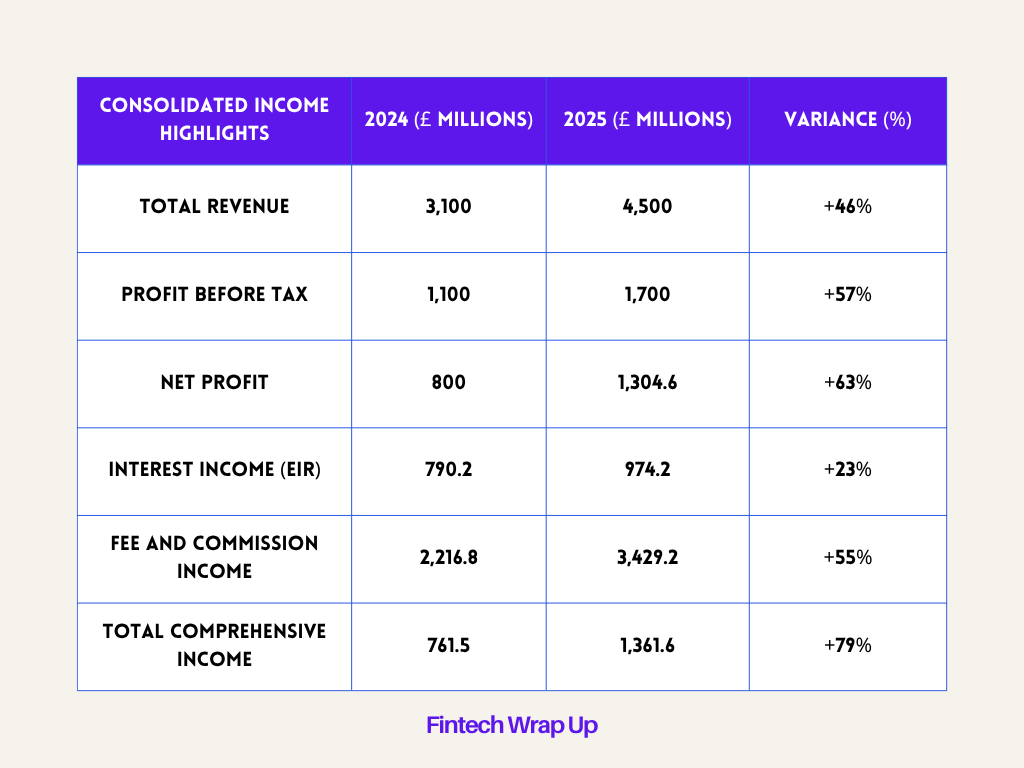

The fiscal year 2025 represents a landmark epoch for Revolut, marking a decade of operational existence and a definitive transition from a high-growth fintech disruptor to a globally systemic financial institution. The dual analysis of the firm’s 2025 Annual Report and the independent assessment by Andreessen Horowitz (a16z) reveals a financial profile characterized by “outlier” performance metrics that deviate significantly from both traditional banking incumbents and modern neobank peers. With a reported revenue of £4.5 billion, a 46% year-on-year increase, and a profit before tax of £1.7 billion, representing a 57% surge, Revolut has demonstrated a capacity for compounding efficiency that validates its technology-first operating model. This transition is underpinned by a “Growth Algorithm” that prioritizes product velocity, regulatory statecraft, and extreme operational leverage, resulting in a return on equity that challenges the fundamental assumptions of the consumer finance sector.

The financial architecture of scaled efficiency

Revolut’s 2025 financial results provide the empirical bedrock for its current $75 billion valuation, establishing it as the most valuable private technology company in Europe. The organization has achieved a rare equilibrium between aggressive top-line expansion and bottom-line profitability, entering its fifth consecutive year of net profit in 2025. According to a16z analysis, a critical component of this success is the “Rule of 75,” a metric formulated by combining revenue growth and net profit margin. For the 2025 period, Revolut achieved a revenue growth rate of 46% (57% when translated to USD) and a net profit margin of 29%, placing it in a unique tier of efficiency that few financial institutions, modern or established, have historically reached.

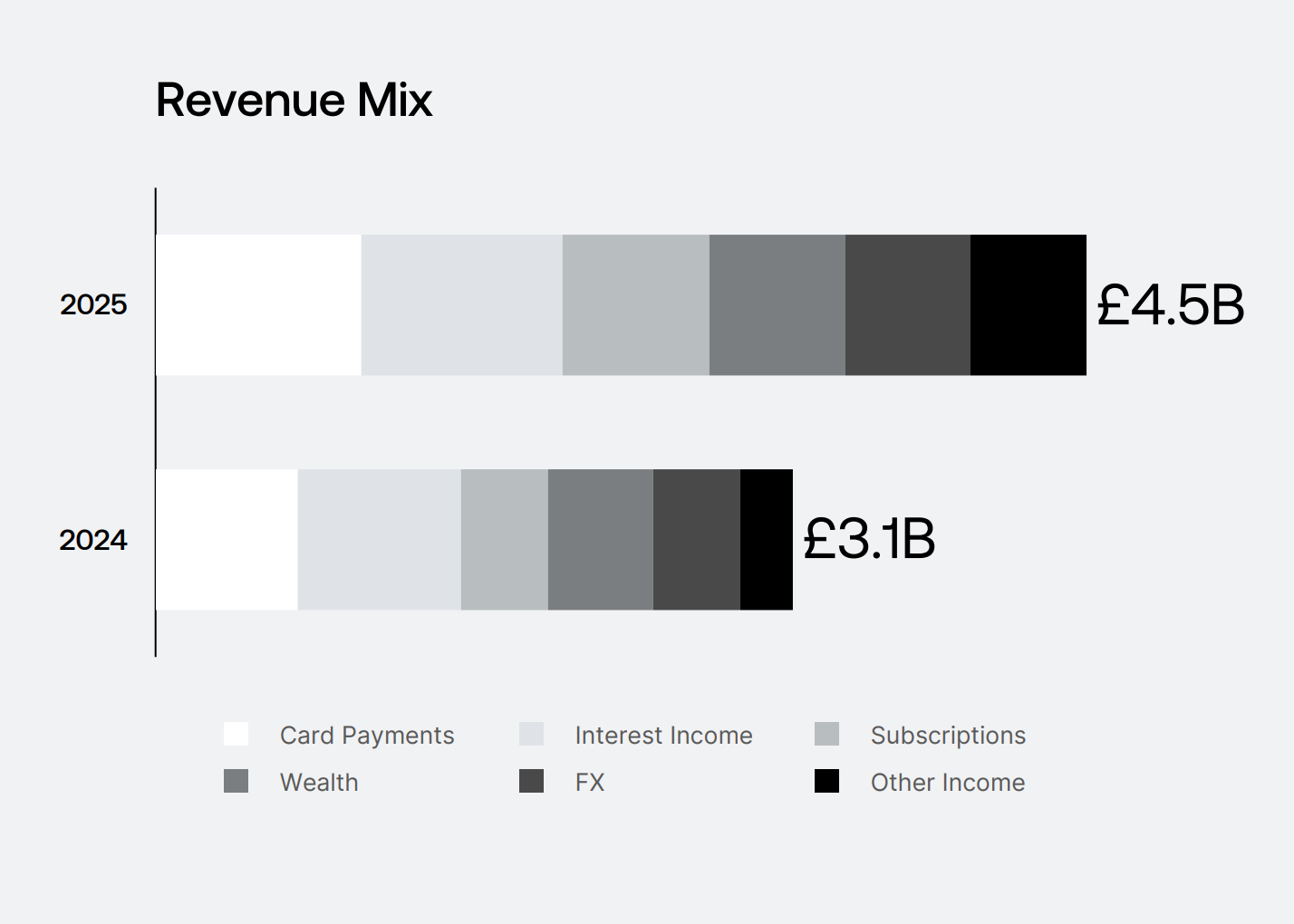

The composition of Revolut’s revenue streams highlights a diversification strategy that mitigates the interest rate sensitivity typically found in traditional banking models. While many established banks derive upwards of 70% of their income from interest, Revolut has inverted this structure, with fee-based revenues accounting for 76% of total turnover in 2025, an increase of 4.2 percentage points over the prior year. This diversification is realized across six primary segments, with no single category responsible for more than 22% of total revenue, ensuring that the firm is not reliant on a “one-trick pony” revenue model.

Revenue mix and segment performance

The 2025 revenue breakdown reveals that card payments remain the largest single revenue stream at 22.2%, closely followed by interest income at 21.6%. The growth in subscription revenue, which reached 15.7% of the total, is particularly significant as it represents a recurring, high-margin income source that reflects deepening customer engagement. Wealth services, including equities and cryptocurrency trading, contributed 14.7%, while foreign exchange services accounted for 13.4%. Internally, the company now tracks 11 distinct product lines that exceeded £100 million in revenue during the 2025 fiscal year, illustrating the breadth of its monetization engine.

The 2025 report also notes a significant shift in geographic revenue distribution. While the United Kingdom remains a core market, Revolut has achieved Euro-wide penetration, with no single country accounting for more than 25% of fee revenue. This regional resilience is bolstered by explosive growth in markets such as France, Italy, and Spain, where Revolut is increasingly perceived not as a secondary travel tool but as a primary bank account of choice. In Europe, approximately one in five working-age adults now uses Revolut, and in several key markets, nearly one in three newly opened bank accounts is a Revolut account.

The compounding algorithm: a16z perspectives on growth

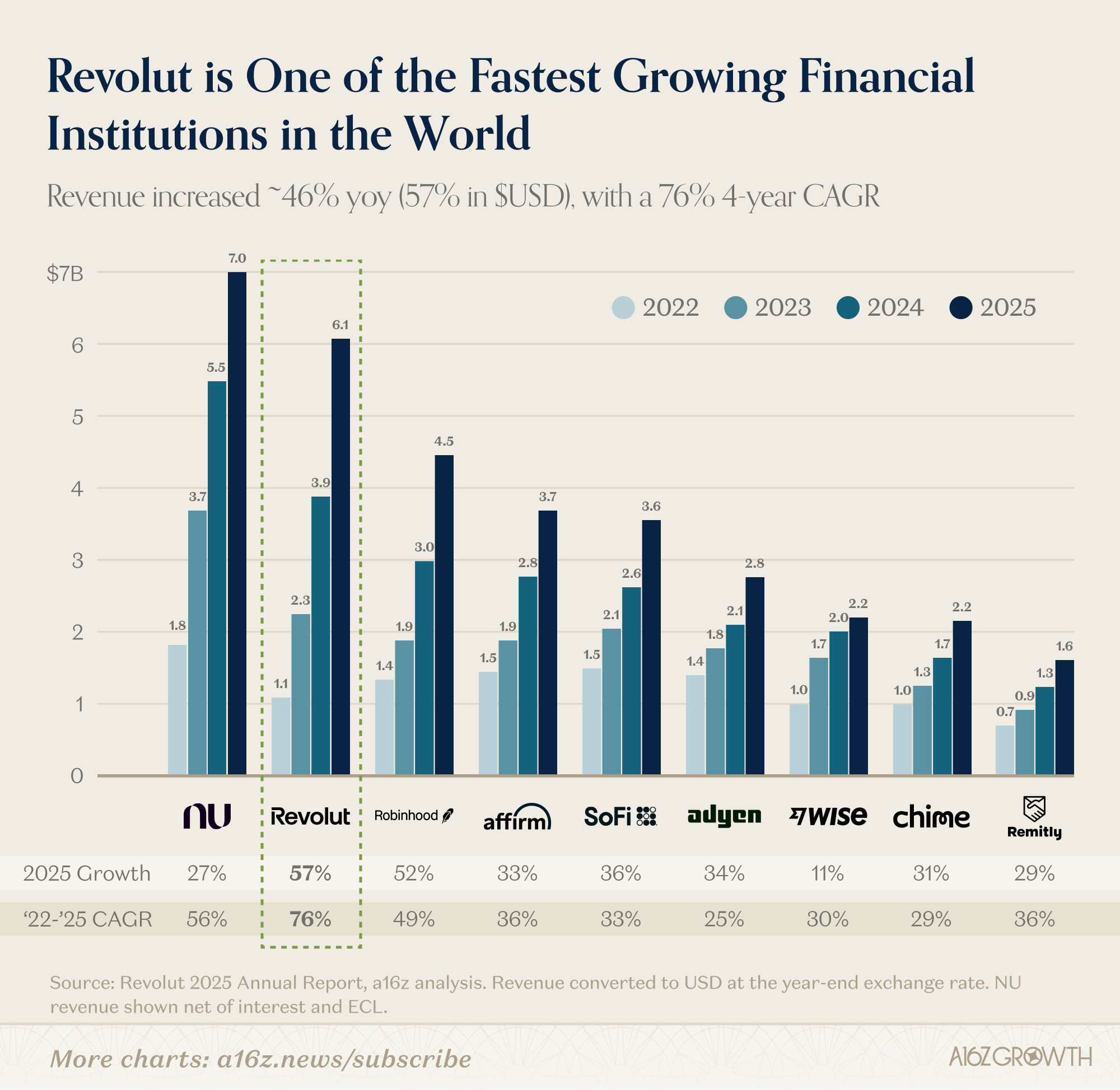

Analysis from a16z posits that Revolut is one of the fastest-growing financial institutions in history, maintaining a remarkable 76% four-year Compound Annual Growth Rate (CAGR) in USD terms since crossing the $1 billion revenue threshold in 2022. This performance is particularly notable given that Revolut operates primarily in mature European markets with entrenched incumbents, unlike peers such as NuBank that have scaled in developing regions. The a16z study emphasizes that in 2022, Revolut had less revenue than many of its well-known fintech peers, including Robinhood, SoFi, and Chime; however, by 2025, it had surpassed them, generating up to three times the revenue of some competitors.

Keep reading with a 7-day free trial

Subscribe to Fintech Wrap Up to keep reading this post and get 7 days of free access to the full post archives.