Reports: Five startup opportunities in stablecoins; The next age of fintech; Asset Tokenization in Financial Markets

The reports highlight how stablecoins and tokenization are reshaping financial infrastructure beyond crypto speculation. Stablecoin adoption is creating new startup opportunities in fiat off-ramping, enterprise compliance, privacy-focused payments, B2B FX liquidity, and global digital banking. At the same time, fintech continues expanding rapidly, with industry revenues reaching $650B in 2025 and projected to approach $2T by 2030, driven by stablecoin growth, consolidation, and increasing profitability. Meanwhile, asset tokenization is emerging as a structural upgrade for financial markets, improving settlement speed, collateral mobility, transparency, and operational efficiency, particularly in bonds and asset management. Together, the reports suggest the next phase of fintech will be defined by regulated digital assets, programmable financial infrastructure, and more efficient global payment and capital market systems.

Video of the Week

Deep Dive of the Week

The 2026 Directory of Stablecoin Card Program Enablers

The financial ecosystem of 2026 has definitively transitioned from a phase of speculative exploration to one of rigorous institutionalization. Stablecoins, once viewed through the lens of decentralized finance experiments, now serve as the primary settlement rails for internet-native commerce, representing a structural shift in how value is moved and spent globally. This transformation is anchored by the full deployment of the European Union’s Markets in Crypto-Assets (MiCA) regulation and the United States’ Guiding and Establishing National Innovation for U.S. Stablecoins (GENIUS) Act, both of which have reached critical enforcement milestones as of early 2026.

In the European theatre, the April 2026 status report from the Spanish Government and EU tax agencies confirms that MiCA has moved from a legislative framework into an “eminently supervisory cycle”. The “grandfathering” transitional periods, which allowed legacy providers to operate under limited oversight, are concluding, with a hard deadline of July 1, 2026, for all Crypto-Asset Service Providers (CASPs) to secure full MiCA authorization or cease operations. This regulatory rigor has resulted in a consolidated market of 38 accredited Electronic Money Token (EMT) issuers, ensuring that any card program operating within the Eurozone utilizes tokens backed one-to-one by high-quality liquid assets and redeemable at par value.1 The implication for fintech founders is profound: the “regulatory arbitrage” era is over. Launching a card in Europe now requires an infrastructure partner that is either an Electronic Money Institution (EMI) or maintains a primary relationship with one to ensure that euro-denominated settlement layers like EURe are compliant with the categorical ban on interest-bearing stablecoins.

Simultaneously, the United States has seen the rapid maturation of the GENIUS Act framework. As of April 2026, the Federal Deposit Insurance Corporation (FDIC) and the Office of the Comptroller of the Currency (OCC) have issued comprehensive rules defining the pathways to becoming a Permitted Payment Stablecoin Issuer (PPSI).9 These pathways—spanning subsidiaries of insured depository institutions, federally qualified issuers (FQPSIs), and state-qualified issuers (SQPSIs)—have effectively brought stablecoin issuance into the federal banking perimeter. For product managers, this means that U.S.-based stablecoin cards are no longer “fringe” products; they are regulated financial instruments supported by “pass-through” deposit insurance models and strict reserve asset concentration limits, which prohibit any single financial institution from holding more than 40% of an issuer’s reserve assets. The 2026 market is thus characterized by “bank-grade” systems that support multi-jurisdictional operations, where stablecoins like USDC and PYUSD are treated with the same prudential respect as traditional commercial bank deposits.

This institutionalization has driven stablecoin transfer volumes to unprecedented heights. By 2024, volume had already reached $27.6 trillion, exceeding the combined transaction volumes of Visa and Mastercard, and by 2026, this momentum has only accelerated as cross-border B2B payments and consumer card programs have matured. The “wild ride” of crypto has been replaced by the “steady hum” of stablecoin infrastructure, where the focus has shifted from ideological debates to the practical details of slippage management, cost-basis tracking, and real-time settlement across 190+ countries.

This week’s reports

1️⃣Reforming MiCA for Euro Stablecoins

2️⃣Five startup opportunities in stablecoins

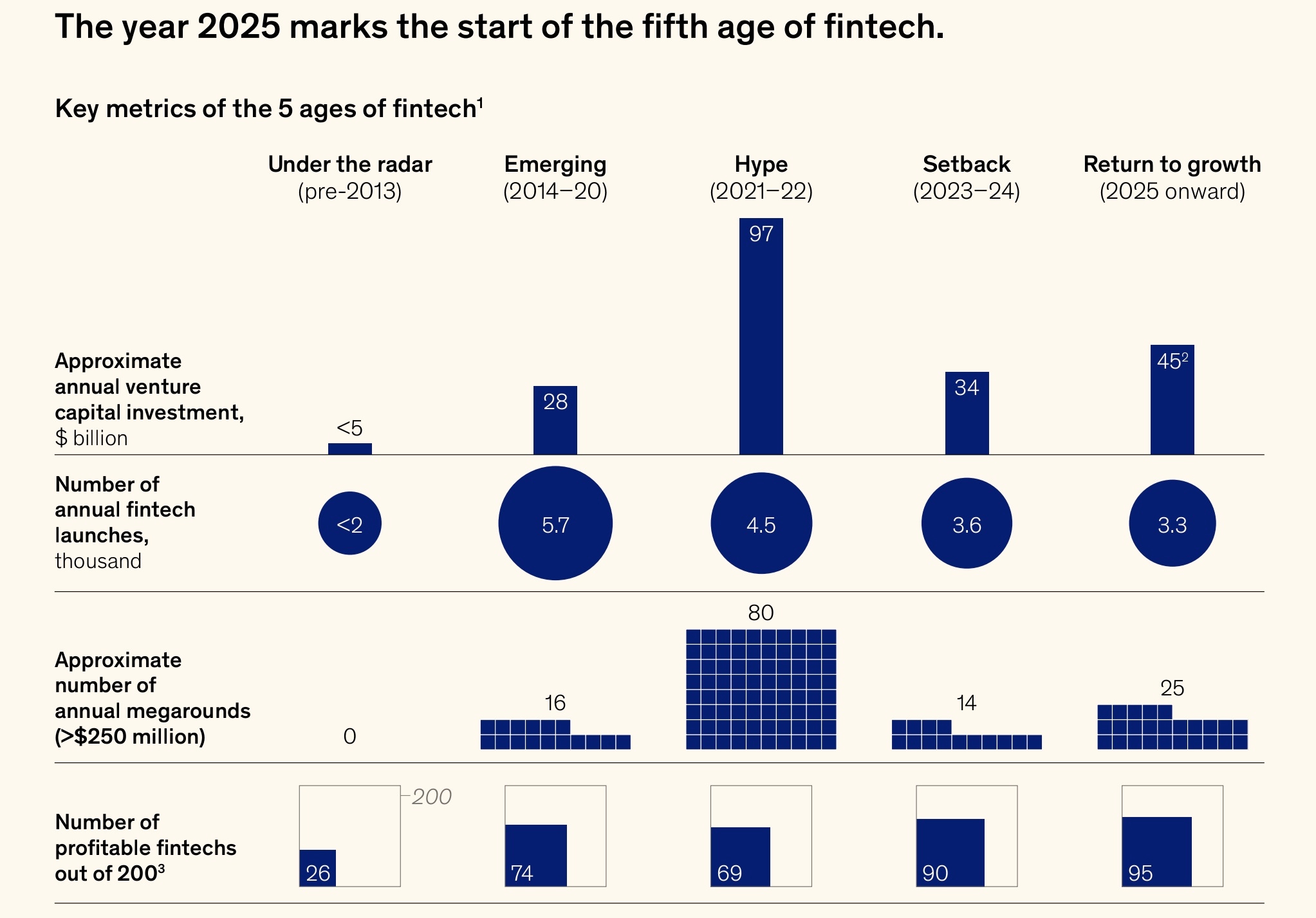

3️⃣The next age of fintech

4️⃣Asset Tokenization in Financial Markets

5️⃣The Coming FinTech Liquidity Supercycle

6️⃣Dollar Supremacy

7️⃣Business Banking Digital Maturity

Reforming MiCA for Euro Stablecoins

Stablecoins are forcing a bigger question in Europe: can regulation protect markets without pricing itself out of relevance?

Europe built one of the world’s most comprehensive crypto frameworks. But comprehensive does not automatically mean competitive. The report argues euro stablecoins still account for less than 1% of global stablecoin volume, despite the euro’s role in global finance.

That gap matters.

Because stablecoins are no longer just crypto instruments. They are becoming payment rails, treasury tools, settlement assets, and increasingly the cash layer for tokenized markets.

The report highlights four structural frictions holding euro stablecoins back:

• ban on interest-bearing models

• rigid reserve allocation rules

• limited access to central bank infrastructure

• unclear cross-border frameworks

In simple terms: Europe has rules, but not yet the conditions for scale.

What I find most interesting is the competitive lens.

Keep reading with a 7-day free trial

Subscribe to Fintech Wrap Up to keep reading this post and get 7 days of free access to the full post archives.