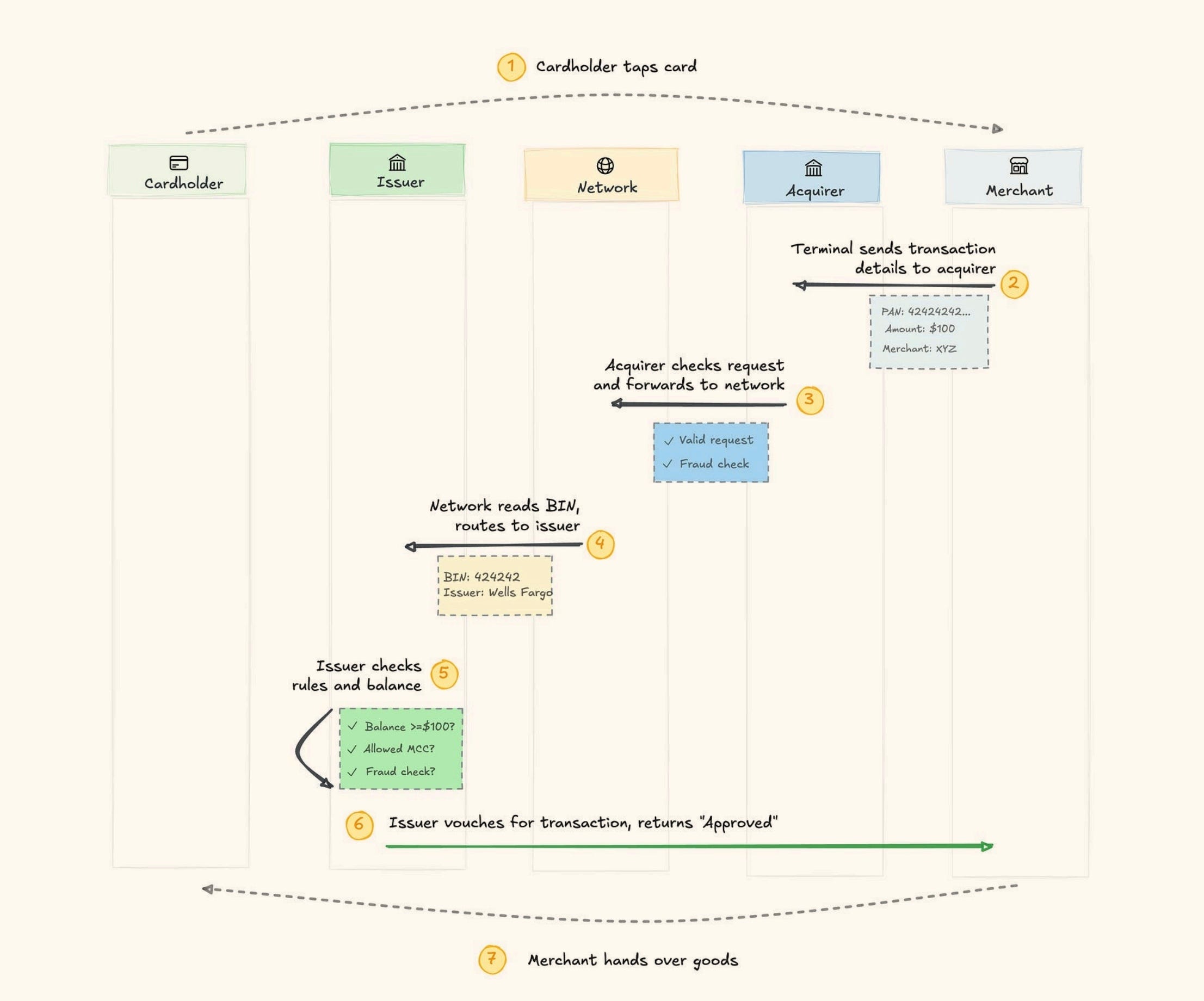

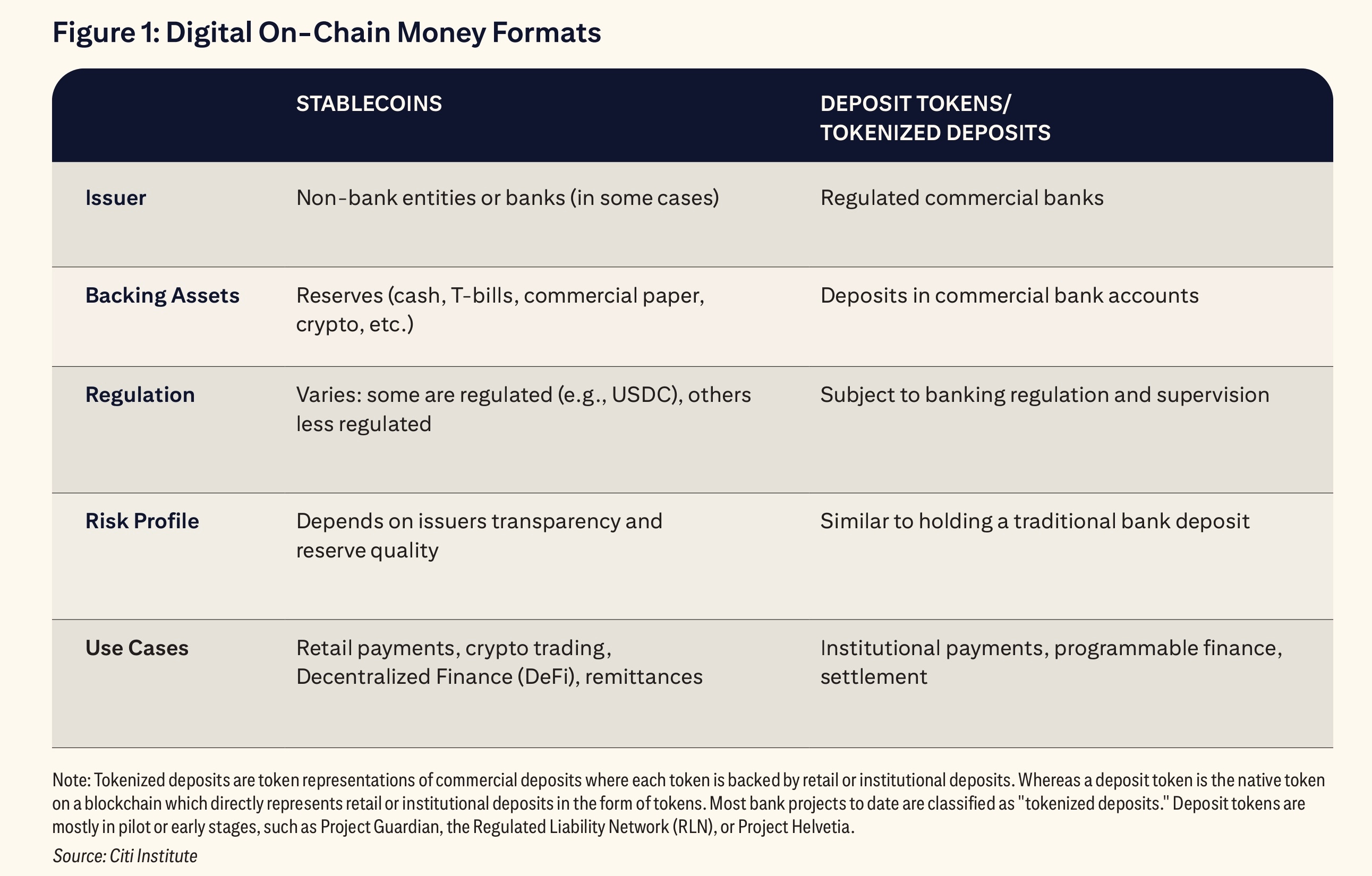

Reports: Card issuing in 1,000 words; Banking in the tokenized economy; Three Types of Digital Money

The reports collectively highlight a major transformation underway in financial services, driven by tokenization, digital money, and real-time infrastructure. Card Issuing in 1,000 Words explains how modern card payments function as a “chain of promises,” where issuers, networks, and acquirers coordinate authorization and settlement, with different card types—debit, prepaid, credit, and charge—shaping risk and economics. Three Types of Digital Money frames the future monetary landscape through CBDCs, deposit tokens, and stablecoins, emphasizing how differences in issuer backing, transfer mechanisms, and banking-system integration will influence regulation, monetary policy, and financial stability. Meanwhile, Banking in the Tokenized Economy argues that tokenization is no longer experimental but a strategic shift reshaping banking business models, with institutions investing in custody, hybrid cloud infrastructure, and AI-enabled settlement systems to remain competitive. Together, these reports suggest the future of finance will be increasingly programmable, real-time, and software-driven, forcing banks and payment providers to rethink infrastructure, customer relationships, and sources of value creation.

Video of the Week

Deep Dive of the Week

Structural Analysis of Visa’s Value-Added Services

The contemporary payments landscape is defined by the progressive decoupling of software intelligence from proprietary physical transaction rails. Historically, global card networks operated as unified utility systems, extracting rent primarily from transaction clearing and settlement routed exclusively over their own systems. Under this legacy framework, monetization was strictly tied to the proprietary network volume. However, the rise of account-to-account (A2A) infrastructure, domestic real-time payments (RTP) schemes, and decentralized ledgers has fragmented transaction routing. In response, Visa has established its Value-Added Services (VAS) division, a strategic shift designed to monetize transactions regardless of the underlying payment network.

During fiscal year 2025, Visa processed 257.5 billion transactions on its proprietary networks, up from 233.8 billion in fiscal year 2024 and 212.6 billion in fiscal year 2023. Total payments and cash volume reached $16.7 trillion in fiscal year 2025, supported by 4.9 billion payment credentials. GAAP net revenue grew 11% year-over-year to $40.0 billion, driven primarily by transaction volumes, nominal cross-border processing, and nominal payments volume.

Against this transaction processing baseline, the VAS portfolio has emerged as a high-margin revenue engine, delivering a 20% compound annual growth rate (CAGR) in constant dollars since fiscal year 2021. In fiscal year 2025, VAS generated nearly $11 billion ($10.9 billion) in revenue, representing a 24% increase over the prior fiscal year.

The structural contribution of VAS to Visa’s net revenue rose from 22% in fiscal year 2021 to 24% in fiscal year 2024. Over the same period, the geographic distribution of VAS revenue shifted internationally, with the share generated outside the United States increasing from 57% to 60%. This geographic dispersion indicates that international markets, characterized by fragmented domestic clearing rails and diverse regulatory systems, have the highest demand for standardized software modules that optimize payment performance.

This week’s reports

1️⃣How Blockchain and Tokenization Can Propel Finance Into the Real-Time Future

2️⃣Three Types of Digital Money

3️⃣Banking in the tokenized economy

4️⃣Key Insights from the 2026 Global eCommerce Payments & Fraud Report

5️⃣What payment optimization really means

6️⃣Card issuing in 1,000 words

7️⃣The Future of Digital Assets

How Blockchain and Tokenization Can Propel Finance Into the Real-Time Future

Modern life operates at the speed of thought. In a 24/7 and always-on digital economy, individuals command global services with a single tap, ordering goods at midnight, streaming a movie, paying a friend, and communicating across time zones without friction.

Technology has redefined our lives, business and society. Many of the architectures, practices and processes that underpin commerce, trade, securities and other critical financial interactions, however, are still playing catch up and are constrained by legacy infrastructure.

This is the always-on divide: a structural gap between an increasingly realtime global economy and a financial system that still operates in parts through batches or intervals. Significant progress has been made, and financial infrastructure is certainly more interconnected than it was in decades past. From the emergence of correspondent banking to the ubiquity of SWIFT messaging and centralized clearing, each iteration has incrementally improved how money and value circulates. However, these advancements have largely retained a model where data and information are transmitted separately from the final settlement of value. While this separation is a practical and efficient design for certain payment types, it represents a fundamental limitation in the context of a fully real-time global economy.

Current end-to-end services rely on a fragmented model of coordinating independent entities. While this establishes a baseline of trust, it means the financial system is prone to be constrained by structural inefficiencies:

Keep reading with a 7-day free trial

Subscribe to Fintech Wrap Up to keep reading this post and get 7 days of free access to the full post archives.