Deep Dive: Structural Analysis of Visa’s Value-Added Services

The contemporary payments landscape is defined by the progressive decoupling of software intelligence from proprietary physical transaction rails. Historically, global card networks operated as unified utility systems, extracting rent primarily from transaction clearing and settlement routed exclusively over their own systems. Under this legacy framework, monetization was strictly tied to the proprietary network volume. However, the rise of account-to-account (A2A) infrastructure, domestic real-time payments (RTP) schemes, and decentralized ledgers has fragmented transaction routing. In response, Visa has established its Value-Added Services (VAS) division, a strategic shift designed to monetize transactions regardless of the underlying payment network.

During fiscal year 2025, Visa processed 257.5 billion transactions on its proprietary networks, up from 233.8 billion in fiscal year 2024 and 212.6 billion in fiscal year 2023. Total payments and cash volume reached $16.7 trillion in fiscal year 2025, supported by 4.9 billion payment credentials. GAAP net revenue grew 11% year-over-year to $40.0 billion, driven primarily by transaction volumes, nominal cross-border processing, and nominal payments volume.

Against this transaction processing baseline, the VAS portfolio has emerged as a high-margin revenue engine, delivering a 20% compound annual growth rate (CAGR) in constant dollars since fiscal year 2021. In fiscal year 2025, VAS generated nearly $11 billion ($10.9 billion) in revenue, representing a 24% increase over the prior fiscal year.

The structural contribution of VAS to Visa’s net revenue rose from 22% in fiscal year 2021 to 24% in fiscal year 2024. Over the same period, the geographic distribution of VAS revenue shifted internationally, with the share generated outside the United States increasing from 57% to 60%. This geographic dispersion indicates that international markets, characterized by fragmented domestic clearing rails and diverse regulatory systems, have the highest demand for standardized software modules that optimize payment performance.

Total addressable market dynamics

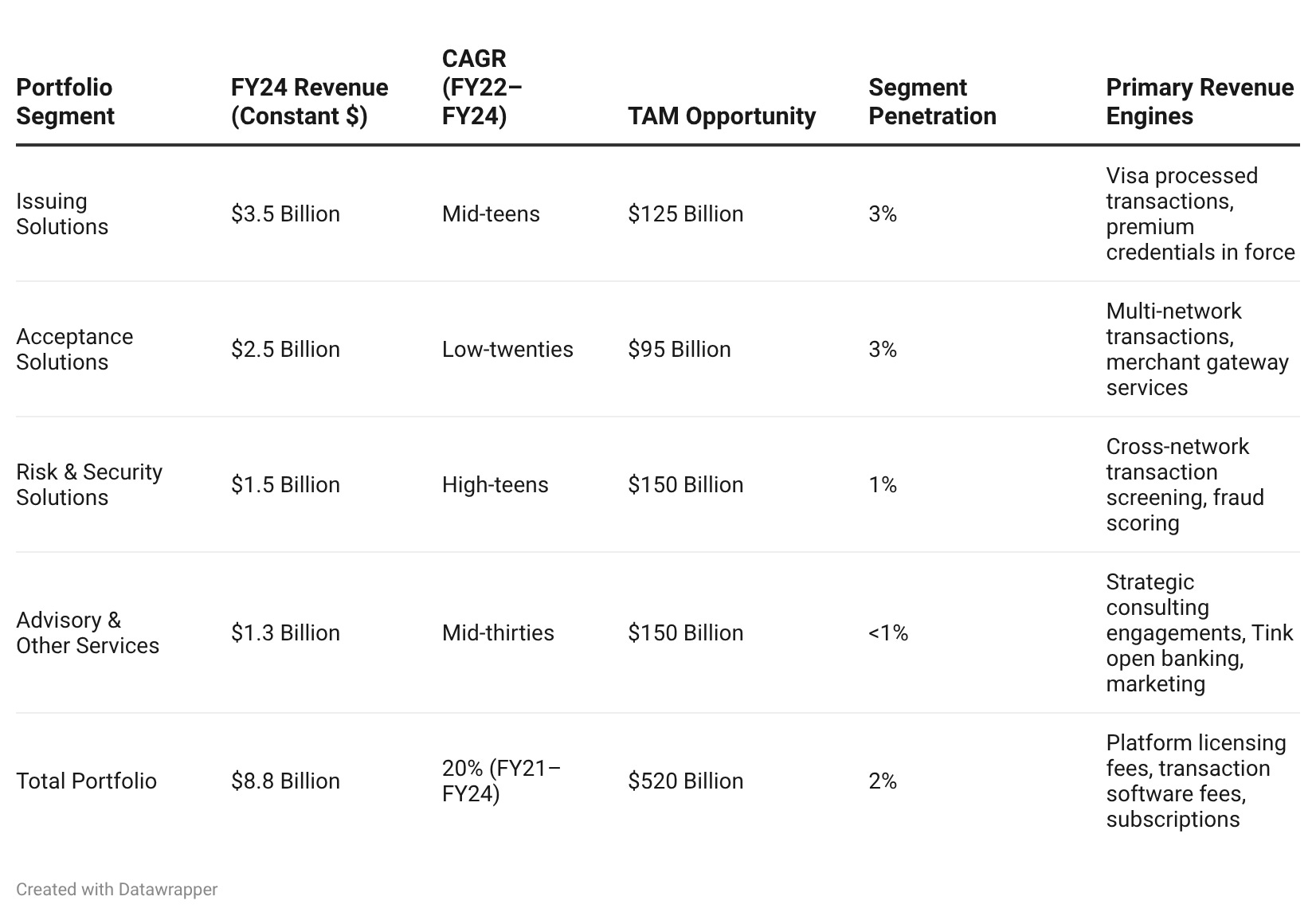

The strategic objective of the VAS portfolio is to address a projected $520 billion total addressable market (TAM). With fiscal year 2024 VAS revenues at $8.8 billion, the organization has captured approximately 2% of this opportunity.1 The distribution of revenue and growth rates across individual VAS portfolios highlights a long runway for software-driven expansion.

The varying CAGRs across these portfolios reveal that while Issuing and Acceptance remain the volume-heavy anchors of the division, the fastest expansion is occurring in Advisory & Other Services. The mid-thirties CAGR in Advisory indicates a structural trend where financial institutions and large merchants are relying on predictive data engines to protect operating margins under interchange compression.

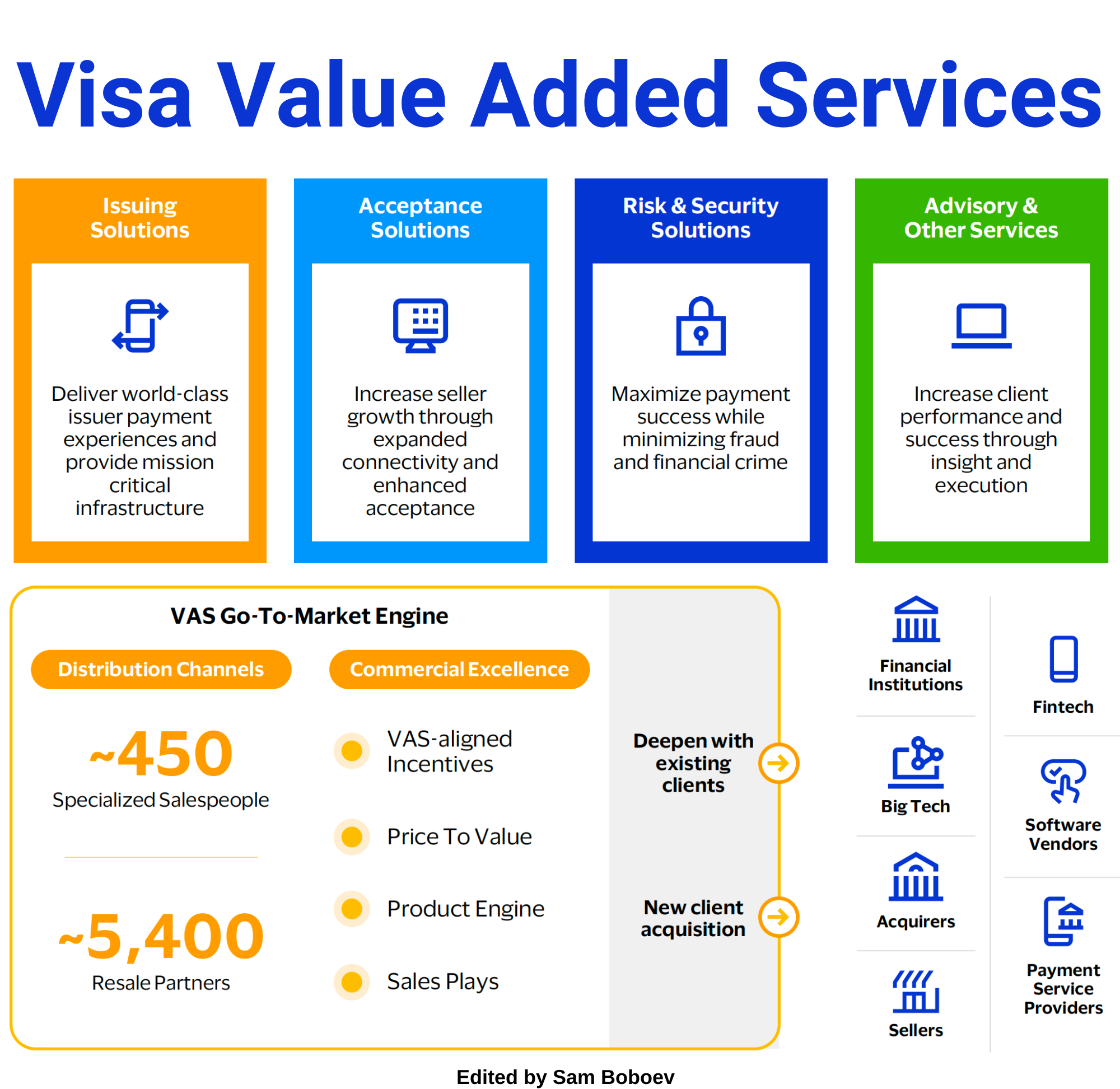

The Visa as a Service Stack

For developers, fintech founders, and software engineers, accessing the global payments network requires programmatic, modular, and highly available interfaces. The organization delivers its services through the Visa as a Service (VaaS) stack, an API-driven architecture structured into four distinct layers.

The foundational layer consists of the physical networks and global telecommunications systems, including four redundant global data centers in the United States, the United Kingdom, and Singapore. This physical layer maintains six-nines of operational reliability and sub-second response times across 200 countries and territories, supporting settlement in 160 currencies.

The services layer abstracts core transactional operations into discrete, reusable software components. Capabilities such as tokenization, multi-factor authentication, and transaction verification are decoupled from card routing, allowing clients to consume them as standalone services.

Keep reading with a 7-day free trial

Subscribe to Fintech Wrap Up to keep reading this post and get 7 days of free access to the full post archives.