Report: AI in banking; Next-Gen Acquiring Processing; Stablecoins could reshape Africa’s digital payments landscape

The reports collectively show that financial services are entering a new phase driven by AI, cloud infrastructure, stablecoins, and modular payment systems. Banks and fintechs are moving from experimentation toward operational transformation, but legacy systems, fragmented data, regulatory pressure, and organizational complexity remain major barriers to scaling innovation. Across banking, payments, and fintech, the competitive advantage is shifting from owning infrastructure to building flexible, API-driven, AI-enabled platforms that can adapt quickly to changing customer and market demands. At the same time, stablecoins are evolving into real payment infrastructure with growing use in commerce, cross-border transfers, and programmable finance, particularly in emerging markets like Africa. The broader message across all reports is clear: the next generation of financial leaders will be the firms and ecosystems that simplify operations, modernize infrastructure, integrate AI responsibly, and create scalable environments for long-term innovation and growth.

Video of the Week

Deep Dive of the Week

The Transaction Foundation Models

We are observing a structural re-architecture of the financial internet. The legacy stack, composed of siloed rule engines, task-specific machine learning models, and human-centric interfaces, is being replaced. We are moving toward a unified paradigm where self-supervised foundation models act as the core operating system for banking and payments. This is a move from information exchange to value exchange. The data suggests that we are witnessing the death of the manual rule engine and the birth of the behavioral embedding as the primary unit of fintech utility.

This deep dive analyzes the technical transition from Gradient Boosted Decision Trees (GBDTs) to Transformer-based foundation models. I will examine the implementation of these systems at Revolut, PayPal, Stripe, and Plaid. I will also detail the infrastructure requirements, the economics of token inference, and the protocol layer defining how AI agents will transact in a zero-trust environment.

This week’s reports

1️⃣AI in banking

2️⃣How radical simplification can transform corporate and investment banking

3️⃣From process automation to industry reimagination

4️⃣Stablecoins could reshape Africa’s digital payments landscape

5️⃣Next-Gen Acquiring Processing

6️⃣9 charts on what stablecoins are becoming

7️⃣Accelerating the Unicorn Landscape in UK Fintech

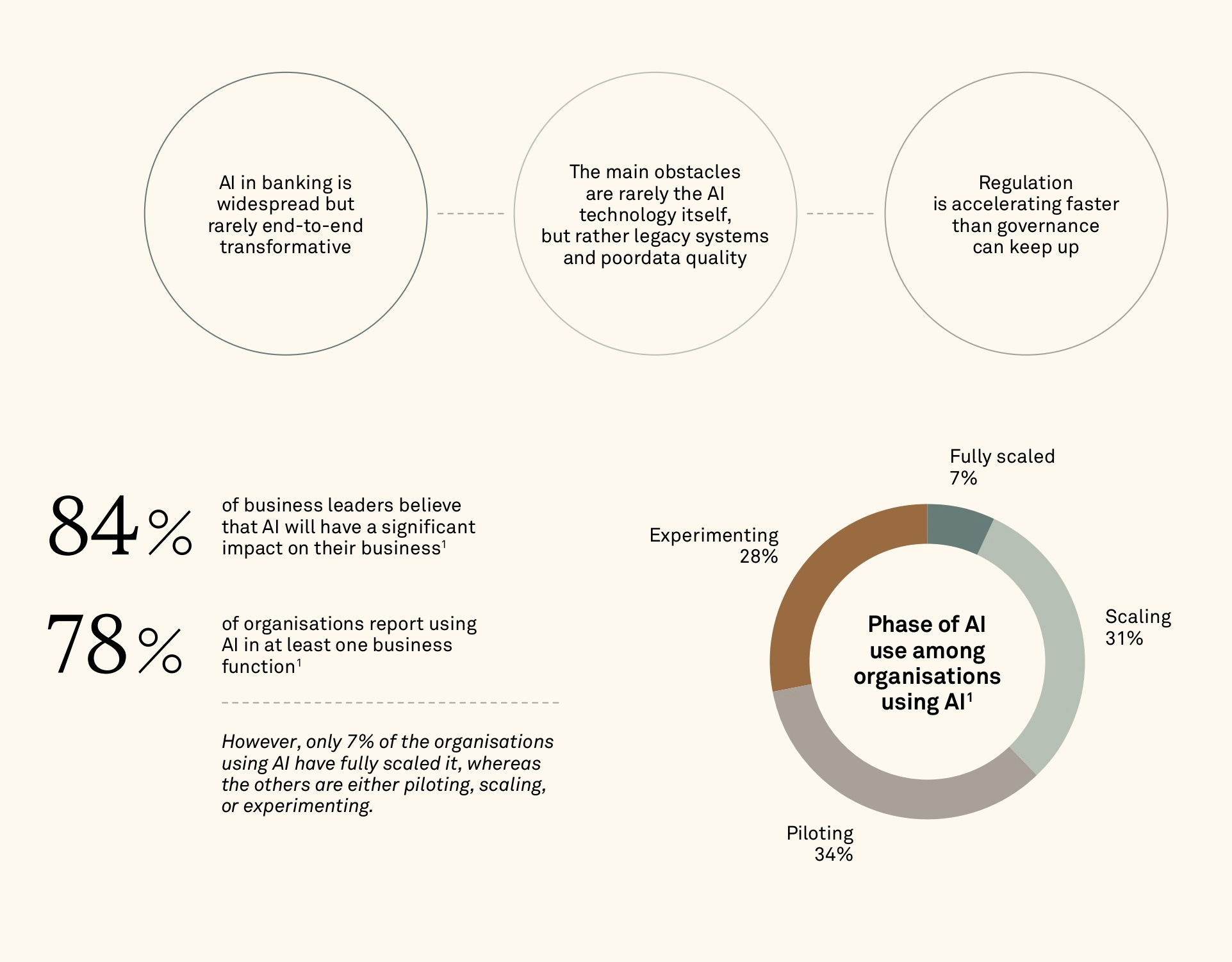

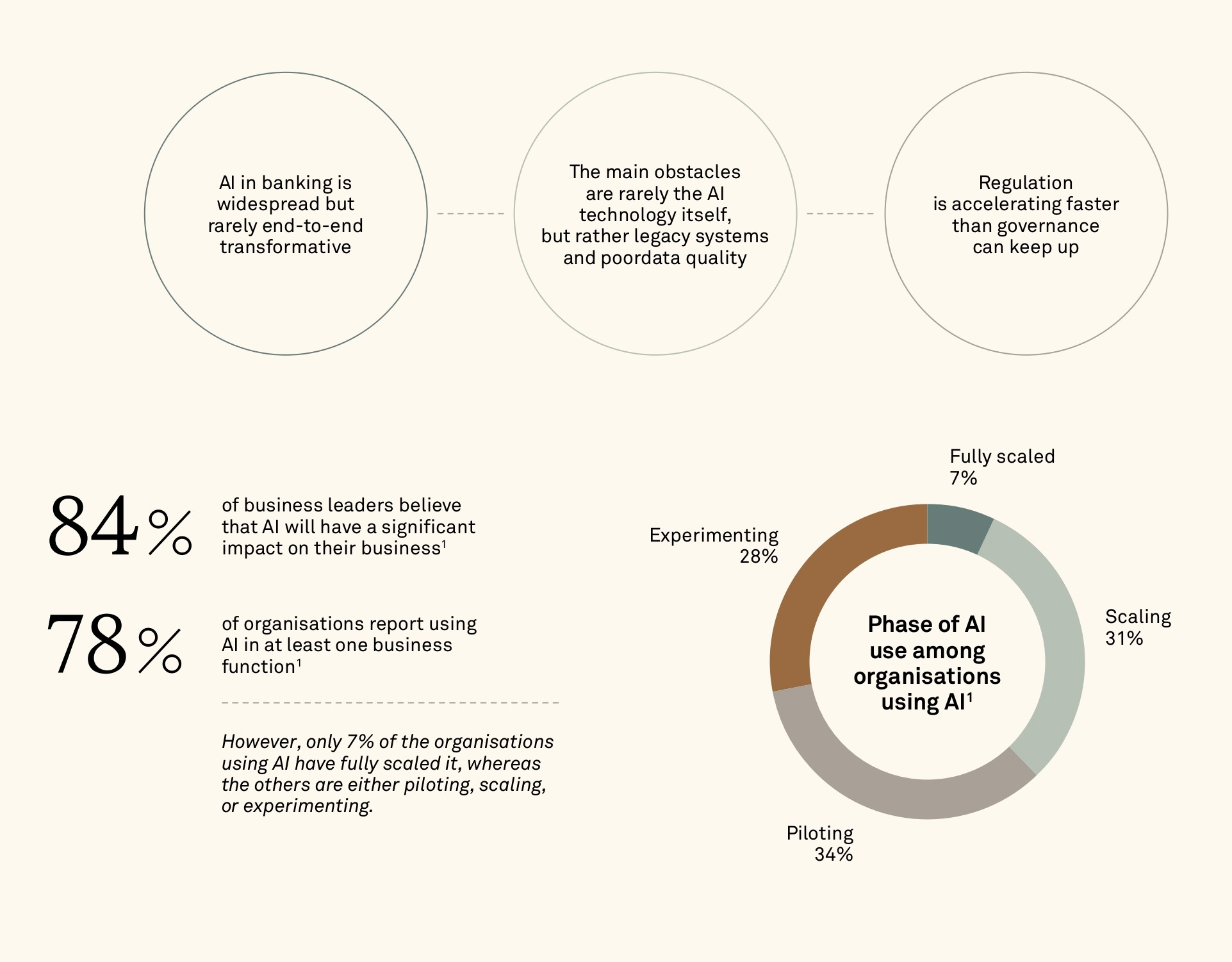

AI in banking

Most banks are no longer asking whether AI matters.

They are asking how to scale it without breaking governance, data quality, or core operations.

One stat from this report stood out to me.

78% of organisations already use AI in at least one business function. 84% of business leaders expect AI to affect their business. Yet only 7% have fully scaled it. Another 31% are scaling, 34% are piloting, and 28% are still experimenting.

That gap says a lot.

AI in banking is real, but it is still uneven. Most banks are not running end to end AI driven journeys yet. They are using AI in narrow parts of the business where the value is easier to prove.

The clearest use cases are already visible.

Keep reading with a 7-day free trial

Subscribe to Fintech Wrap Up to keep reading this post and get 7 days of free access to the full post archives.