How Fintechs Should Approach Stablecoins in 2026; Comparison of successful digital payments systems; Paypal's Strategy Map

Video of the Week

Deep Dive of the Week

Citi’s Strategy to Dominate Institutional Payments

Citi’s core payments thesis is blunt: own and integrate the entire payments value chain globally to stay on top. The bank touts a #1 global market position in institutional payments with an estimated 7.7% market share. That leadership is underpinned by scale and reach. Citi supports local payment flows in ~90 countries through its proprietary network. In practice, this means Citi directly connects to domestic payment systems around the world (290+ clearing system links, by its count) instead of relying solely on partner banks. The thesis is that by “owning the network” end-to-end, Citi can offer clients a more consistent, transparent service globally and capture a disproportionate share of volumes.

This strategy is driven by the structural shift to digital commerce and real-time finance. As transactions move online and instantaneously, Citi is positioning itself as the go-to infrastructure for institutional money movement. Payments already contribute the bulk of Citi’s Treasury and Trade Solutions (TTS) business, roughly three-quarters of TTS non-interest revenue, growing ~13% annually in recent years. The bank processed $358 B in cross-border FX payments in 2023, up from $280 B in 2021 (13% CAGR). It also handled 157 million USD clearing transactions in 2023 and saw explosive growth in instant payments (from ~2 million to ~10 million daily transactions, ~120% CAGR over 2021–2023). In short, Citi’s payments franchise is huge and on an upswing, a high-growth profit engine in an otherwise mature banking landscape.

Citi’s thesis is to double down on this momentum by meeting clients’ evolving needs across every leg of a payment’s journey. That journey spans accepting payments, holding liquidity, paying out, and financing transactions. Citi’s strategy explicitly breaks this into “Accept, Hold, Pay, Finance,” ensuring the bank has offerings at each step. The underlying bet: if Citi can embed itself at each link in the chain from checkout to treasury to disbursement, and FX clients will find it compelling to consolidate their flows through Citi’s ecosystem. And with the global footprint already in place, Citi can capture the worldwide shift to electronic payments, e-commerce, and instant funds movement at scale.

This week’s reports

1️⃣PwC Global Crypto Regulation Report 2026

2️⃣CB Insights’ State of Fintech 2025

3️⃣How Agentic Commerce Changes Discovery, Trust, and Payments

4️⃣Payments Are a $354B Engine of the US Economy

5️⃣Fintech & Payments Public Comp Sheet and Valuation Guide

6️⃣How Blockchain Infrastructure Can Transform the Future of Financial Services

7️⃣The Financial Services Guide to Building Autonomous AI Agents

This week’s insights

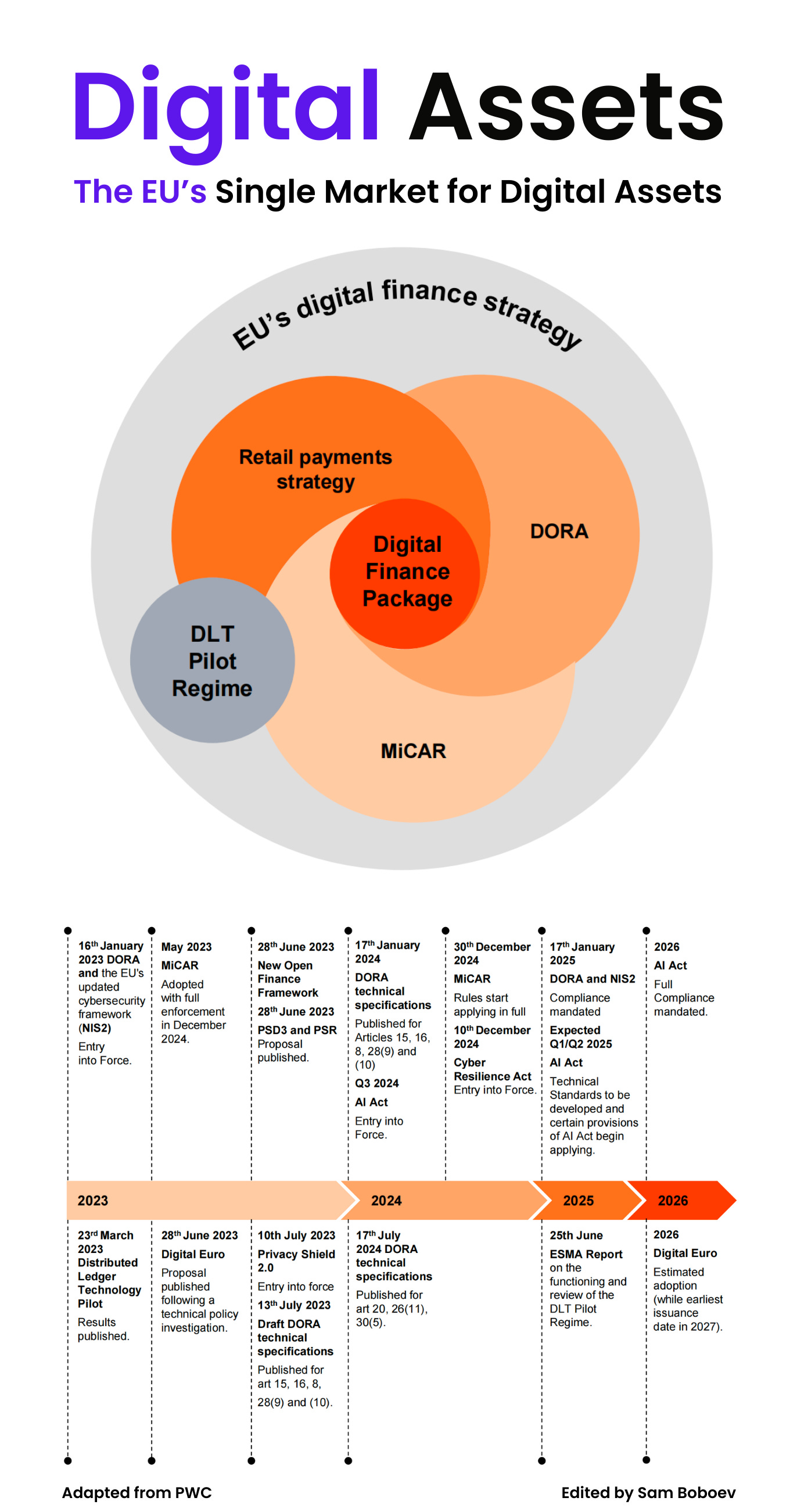

1️⃣The EU’s Single Market for Digital Assets

2️⃣How Fintechs Should Approach Stablecoins in 2026

3️⃣An AI-enabled current account opening journey

4️⃣Comparison of successful digital payments systems

5️⃣Paypal’s Strategy Map

6️⃣Why Most Payment Data Fails to Drive Decisions (and How Teams Fix It Over Time)

7️⃣Crypto Card Transaction Flow Mechanics

The EU’s Single Market for Digital Assets

The impending regulatory framework, comprising MiCAR, AMLR and DORA represent a significant step towards a well-regulated and resilient crypto-asset market within the EU but with possible higher barriers to entry or those seeking to access or otherwise do business with EU established market participants.

By addressing authorisation, transparency, consumer protection, AML compliance and operational resilience, these regulations collectively aim to foster a secure and trustworthy environment for crypto-asset activities.

Firms operating within or considering expanding to this sector must prepare to meet this comprehensive set of requirements to ensure compliance.

____

Digital Finance Package (DFP)

The European Commission adopted the DFP to support the innovation and competition of digital finance. Aiming to ensure consumer protection, mitigating risks and boosting financial stability.

____

DLT Pilot Regime

The DLT Pilot Regime created a controlled, EU-wide regulatory sandbox for core market infrastructures to handle tokenized financial instruments using DLT. It also put tokenized financial instruments firmly under the MiFID II remit and remains the subject of ongoing policy discussions and updates.

____

Retail payments strategy

Retail payments strategy aims to achieve a fully integrated retail payment system in the EU, including instant crossborder payment solutions.

____

Digital Finance Strategy

Sets out the European Commission’s key priorities and objectives over the next four years and how it plans to achieve them. The four stated priorities are:

Keep reading with a 7-day free trial

Subscribe to Fintech Wrap Up to keep reading this post and get 7 days of free access to the full post archives.