How Agent Tokenization will work; Digital banks scale in five stages; Evolution of Financial Big Data Platform Architecture;

Welcome to the latest edition of Fintech Wrap Up — your go-to source for what’s next in fintech, from AI agents and tokenized payments to big data and digital banks

Insights:

1️⃣ How Agent Tokenization will work

2️⃣ Evolution of Financial Big Data Platform Architecture

3️⃣ Digital banks scale in five stages

4️⃣ Which eCommerce Company Is Dominating Cross-Border Activities?

5️⃣ Can Tokenized Money Solve the Cross-Border Puzzle?

6️⃣ What Is Network Tokenization and Why It Should Be on Your Radar

7️⃣ A Digital Euro Could Cost Banks Billions — Are They Ready?

8️⃣ E-Wallets, Big Tech, and the Future of Payments: What’s Next?

9️⃣ Stripe Acquires Privy to Bolster Its Cryptocurrency Game

TL;DR:

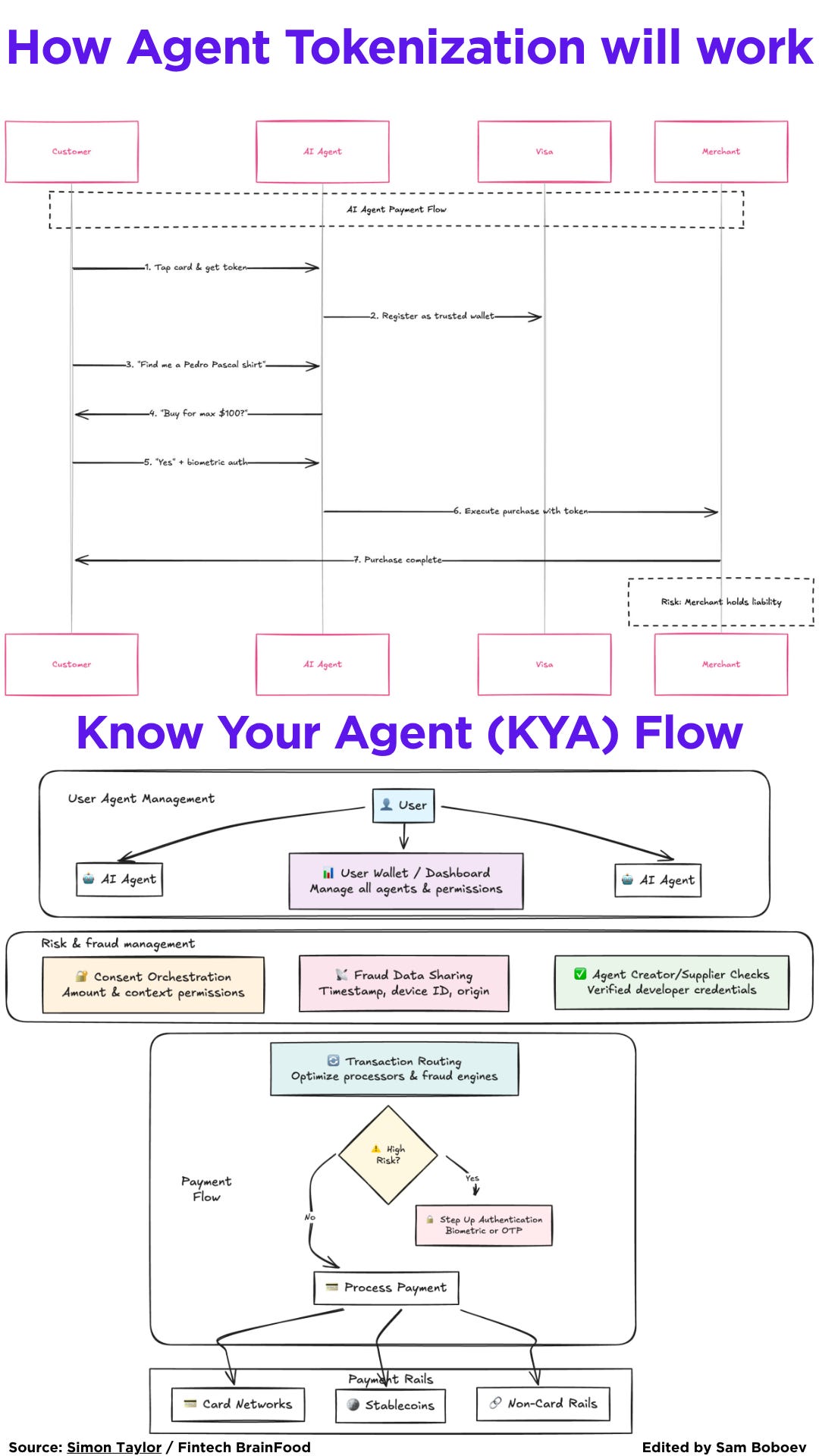

Let’s start with the future of payments: Agent Tokenization. As AI agents begin making purchases on our behalf, they’ll use tokens tied to both the agent and device, registered with networks like Visa. Users will chat with their agent to approve purchases, set limits, and define when extra verification is needed. But there are challenges ahead—especially around liability and interoperability across rails like cards, bank payments, and stablecoins. That’s where Know Your Agent (KYA) comes in: a framework to manage agent identity, permissions, fraud data sharing, and user dashboards.

In infrastructure, financial firms are embracing lake-warehouse convergence. This hybrid architecture unifies structured and unstructured data processing while cutting costs and boosting performance. Decoupled compute and storage, real-time analytics, and global file systems are making data platforms more scalable, efficient, and resilient.

Meanwhile, digital banks scale through five clear stages—from single-product launches to full financial ecosystems. Monzo, Nubank, and Revolut show how layering value, not just features, creates long-term growth across regions and verticals.

In eCommerce, Amazon dominates cross-border trade, generating $360B in 2023—more than any other platform. Alibaba holds four of the global top 10 cross-border marketplaces, but Amazon’s global reach and logistics edge are tough to beat.

Back in the lab, Hong Kong’s e-HKD+ pilot is testing how tokenized money like e-HKD and deposits can power instant, programmable cross-border payments. Using smart contracts and cross-chain bridges, the project aims to cut risks and increase compliance in global fund flows.

And don’t ignore network tokenization—it’s becoming a payment essential. By replacing raw card data with secure tokens, businesses can cut fraud by 50% and boost approvals by nearly 5%, while avoiding vendor lock-in and outdated credentials.

Finally, a stark reality: Europe’s banks may face over €2B in costs to prepare for the digital euro. With upgrades needed across apps, ATMs, compliance systems, and more, this shift isn’t just technical—it’s a massive financial and strategic challenge.

That’s your wrap. Fintech’s future is getting smarter, faster, and more connected—are you keeping up?

Reports

Insights

E-Wallets, Big Tech, and the Future of Payments: What’s Next?

I joined Igor Tomych to unpack some of the most exciting trends shaping fintech right now.

Mastercard’s Shift - From Plastic to Platforms

Mastercard is far more than a credit card company – it’s a lynchpin of the modern financial system and a bellwether in fintech’s evolution. In an era where digital payments are surging and new technologies like artificial intelligence are redefining commerce, Mastercard’s role has never been more crucial. The company operates a massive global network that quietly powers transactions for billions of consumers and millions of businesses, across over 210 countries and territories. Indeed, Mastercard’s worldwide reach – with 3.4 billion Mastercard cards in circulation and acceptance at some 150 million merchant locations – underpins the daily flow of commerce on a breathtaking scale. Even today, a large majority of transactions globally are still done in cash (around 85% by some estimates), which highlights why Mastercard matters: it sits at the forefront of the secular shift toward cashless, digital payments. As fintech readers know, who enables and captures this shift is key – and Mastercard, with its vast network and adaptive strategy, has positioned itself as an indispensable platform in the fintech landscape.

But scale is only part of the story. What makes Mastercard truly interesting now is how it has transformed its business beyond traditional card swipes. Over the past decade, the company has aggressively diversified – expanding into new payment rails, new markets, and new value-added services. It’s innovating in areas like open banking, real-time bank transfers, and even AI-driven payments. In short, Mastercard is no longer just a payments processor; it’s becoming a broad fintech solutions provider. This deep dive explores Mastercard’s business model evolution, its strategic priorities (from digitization to B2B payments), its latest innovations such as Agent Pay in AI commerce, the rise of its services business, and its financial performance and global positioning. The picture that emerges is of a company leveraging its heritage and network strengths while reinventing itself to stay ahead in a rapidly changing fintech world.

How Agent Tokenization will work

1. Agent Token is generated: The AI Agent at the point of intent will ask customer to tap card to a device. A token will be given to agent that is "device" and "agent" specific.

2. Agent registers with Visa: The AI Agent then becomes “trusted” in the way a mobile wallet does with tokenization today.

3. The customer initiates a conversation with their Agent that involves shopping: e.g. holiday, new office equipment, a used Pedro Pascal shirt from the set of The Last of Us.

4. Auth instructions are finalized: eg Agent can buy the Pedro Pascal shirt at eBay for a maximum of $100.

5. Auth instructions define if human-step-up is required: If it’s over $100 for example.

6. Auth instructions are matched at the merchant: If the tokens match, the payment is authorized

7. Liability remains with the merchant: Expect merchants to revolt and decline a lot of transactions of this remains true. (This may be different in Europe where SCA makes issuers more likely to bear liability).

This all implies tokenization is embedded in the chat interface somehow, or that there’s a link between the chat interface and a digital wallet.

But what happens if you want to use pay by bank, or stablecoins? Visa and Mastercard would argue, you can use their tokens on those rails too. But the practical reality is, there will never be one token network to rule them all.

👉 Know Your Agent (KYA)

1. One framework emerging is Know Your Agent (KYA) - a concept I helped explore at Sardine with PayOS.

Keep reading with a 7-day free trial

Subscribe to Fintech Wrap Up to keep reading this post and get 7 days of free access to the full post archives.