What is Mastercard Track?; Digital Lending: Capabilities-as-a-Service (CaaS); Payment System Modular Functional Flow;

Welcome to this week’s Fintech Wrap Up—where we dive into how banks are cashing in on stablecoins, Mastercard is transforming B2B payments, and Europe’s EPI wallet is making a comeback.

Insights & Reports:

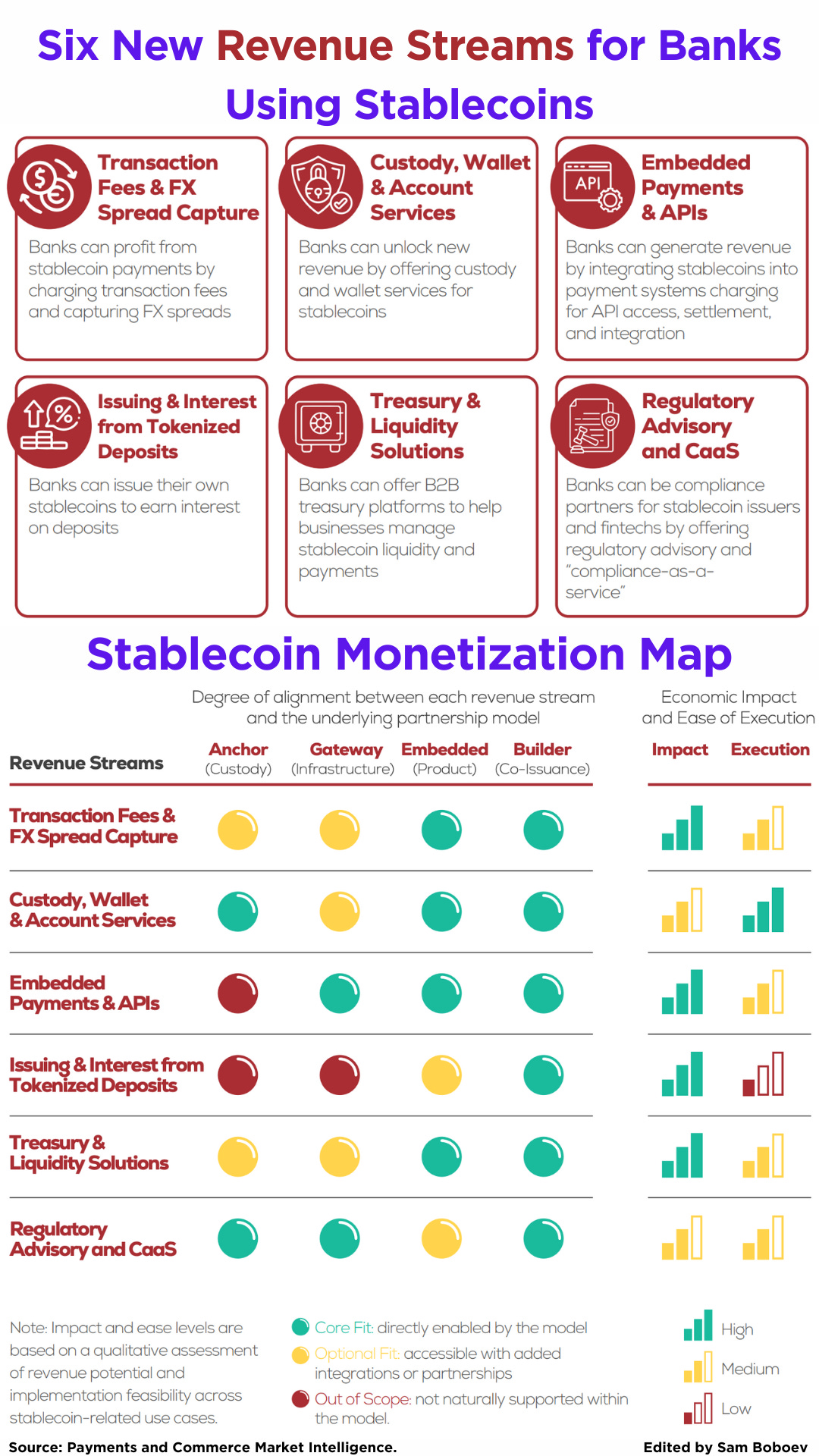

1️⃣ Six New Revenue Streams for Banks Using Stablecoins

2️⃣ What is Mastercard Track?

3️⃣ Stablecoins at Scale: How the UAE is Shaping Institutional Finance in the Digital Age

4️⃣ Payment System Modular Functional Flow

5️⃣ Digital Lending: Capabilities-as-a-Service (CaaS)

6️⃣ How Payment Orchestration Improves Transaction Success Rates

7️⃣ European Payments Initiative (EPI)

8️⃣ Neobank Revolut Actively Exploring Launching Its Own Stablecoin

9️⃣ Fiserv unveils plans to launch stablecoin with Circle, PayPal as partners

TL;DR:

Welcome to this week’s Fintech Wrap Up — your go-to for the latest in payments and digital finance.

Banks are unlocking six new revenue streams from stablecoins, from low-cost FX and transaction fees to custody, embedded payments, and interest income on reserves. With major players like JPMorgan and Stripe already monetizing stablecoin flows, this shift is reshaping bank infrastructure and revenue models.

Mastercard Track is streamlining B2B payments by automating supplier verification, onboarding, and invoice matching—reducing fraud and payment friction across supply chains. Meanwhile, the UAE is emerging as a global stablecoin leader, with strong regulation fueling real-world use cases in FX, trade finance, and treasury.

On the tech side, modular payment systems and orchestration are helping banks and fintechs scale faster, cut costs, and boost transaction success rates. Payment orchestration, in particular, is proving essential for revenue recovery, using smart routing and retries to rescue failed payments.

In lending, Capabilities-as-a-Service (CaaS) is breaking down silos by powering multiple products through a unified, modular architecture. And in Europe, EPI’s Wero wallet is back on track with acquisitions like iDEAL and Payconiq, aiming to go live in more markets by mid-2025.

Thanks for reading Fintech Wrap Up!

Reports

Insights

How Shift4 Is Building a Global Commerce Platform

In the fast-moving world of fintech and payments, few companies have transformed as dramatically in recent years as Shift4 Payments. Born as a small merchant processor in the late 1990s, Shift4 has rapidly evolved into a global “commerce technology” player powering payments for over 200,000 businesses today. Its story matters now because Shift4 is at an inflection point: after years of hyper growth, strategic acquisitions, and expanding beyond its

U.S. base, the company is positioning itself as a serious challenger to payment incumbents worldwide. In 2024 and 2025 alone, Shift4 has embarked on bold moves – from mega-acquisitions in Europe to launching its all-in-one point-of-sale platform internationally – that could reshape the competitive landscape of integrated payments. Moreover, founder and CEO Jared Isaacman is handing over the reins after 26 years, marking a leadership transition just as Shift4 pursues ambitious global targets. For fintech observers, Shift4 offers a compelling case study of software and payments convergence done right, and its next chapter will signal how far an upstart can go in challenging entrenched rivals. This deep dive provides a comprehensive look at Shift4’s background, strategy, financial performance, expansion plans, and competitive context at this pivotal moment.

Six New Revenue Streams for Banks Using Stablecoins

1. Transaction Fees & FX Margins

Stablecoin transactions are cheaper—but not free. While clients save up to 80% compared to traditional transfers, banks still earn on each transaction and FX conversion. Swapping stablecoins like USDC into local currency allows banks to profit from predictable spread margins, reducing client costs (from 3–7% to 0.6–1.4%) while securing volume-based revenue.

2. Custody, Wallet & Account Services

Corporate clients need secure, regulated ways to store and use digital dollars. Banks can offer familiar account-style interfaces, with blockchain infrastructure behind the scenes. Extra charges apply for features like insurance, premium support, or bundled treasury tools. BNP Paribas, for instance, charges custody and account fees for digital assets, including stablecoins.

3. Embedded Payments & API Revenue

Embedding stablecoins in B2B and B2C payments—think supplier payouts, gig worker remittances, or e-commerce—opens up monetization through APIs. Banks can charge for access, settlement, and integration. Stripe already charges 1.5% for USDC payments. Visa and BBVA are embedding stablecoins into cross-border flows, monetizing API infrastructure.

4. Tokenized Deposits & Interest Income

Banks issuing stablecoins backed by customer deposits can invest reserves in low-risk assets and earn interest—just like Circle and Tether. JPMorgan’s JPM Coin clears $1B daily and earns on reserves. Platforms like Bastion even help banks launch branded stablecoins and capture yield.

Keep reading with a 7-day free trial

Subscribe to Fintech Wrap Up to keep reading this post and get 7 days of free access to the full post archives.