Visa's strategy map is not about payments; Five essential uses of agentic AI in banking; Three Layers of Crypto Card Infrastructure

Video of the Week

Deep Dive of the Week

Global Payments’ Merchant Solutions Strategy

Global Payments’ merchant solutions business is built on a three-pronged product architecture designed to serve merchants of all sizes and verticals. The three segments are POS & Software, Integrated & Embedded, and Core Payments. Each segment represents a distinct product line within the merchant ecosystem, with its own software capabilities and go-to-market channels. This segmented architecture allows Global Payments to address different merchant needs from full point-of-sale systems with business software, to embedded payments in third-party platforms, to high-volume payment processing under one unified merchant solutions umbrella.

This week’s reports

1️⃣The 2025 state of AI and fraud

2️⃣How European Payment Companies Must Design Settlement Infrastructure

3️⃣A practical guide for banks operating in 2026

4️⃣Interoperability Standards for Digital Assets

5️⃣From the Unbanked to the Unbrokered

6️⃣Europe’s Digital Euro Just Entered the Live Payments Phase

7️⃣Accenture’s Top Banking Trends 2026

This week’s insights

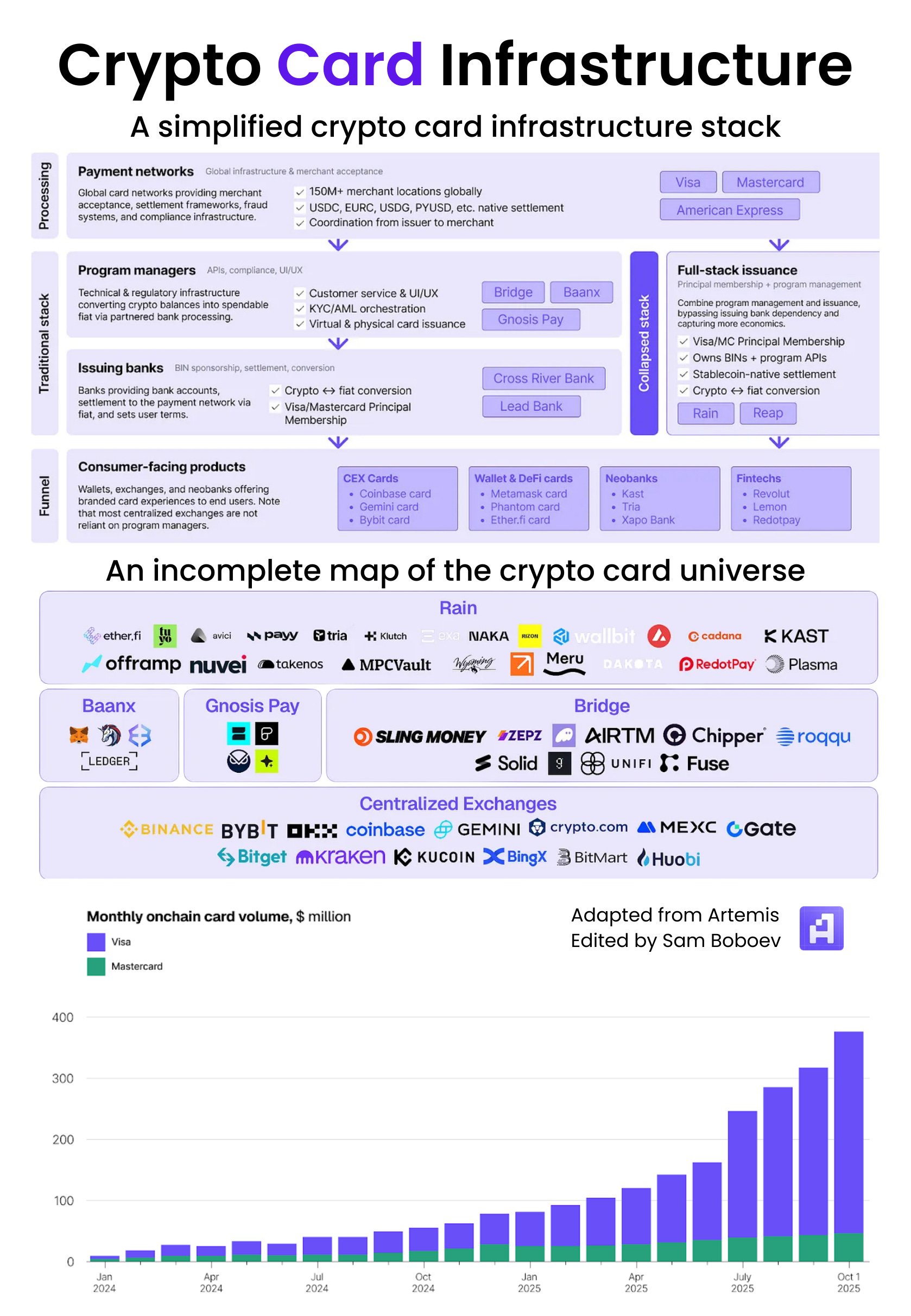

1️⃣Three Layers of Crypto Card Infrastructure

2️⃣Stablecoins and merchant settlement

3️⃣Five essential uses of agentic AI in banking

4️⃣What is Fintech 3.0 and How Did We Get Here?

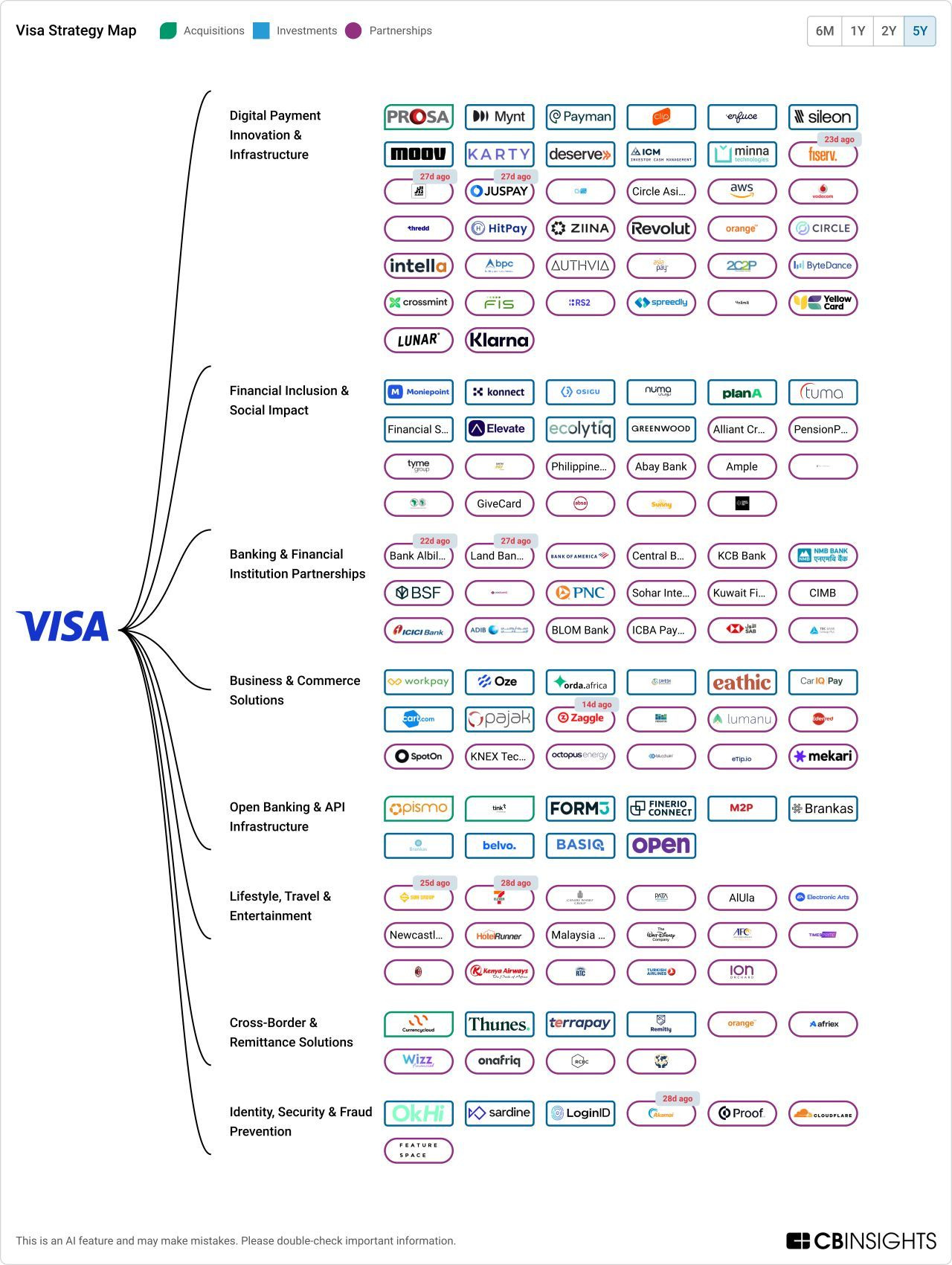

5️⃣Visa’s strategy map is not about payments

6️⃣Mega-rounds drive more than half of all Q4’25 fintech funding

7️⃣A clearer view of stablecoin payment activity

Three Layers of Crypto Card Infrastructure

Layer 1: Payment Networks

Visa and Mastercard control over 70% of global card network market share (Nilson Report, 2024). In crypto cards, their share is effectively ~100%, with rare exceptions such as the Coinbase One Card issued on American Express.

Despite similar program counts, Visa captures a larger share of onchain-linked card volume. This is a distribution outcome, not a product difference.

Visa prioritized early partnerships with crypto-native program managers and infrastructure providers such as Rain and Reap. One integration unlocks dozens of downstream card programs, allowing Visa to scale alongside new issuers entering the market.

Mastercard focused more heavily on direct partnerships with large centralized exchanges. Revolut, Bybit, and Gemini all operate Mastercard-branded programs. Volume here tracks exchange user bases and trading cycles more tightly.

The strategies overlap in practice. Networks often coexist within the same issuer stack.

Visa’s volume advantage suggests infrastructure-first distribution scales more efficiently than exchange-by-exchange deals.

____

Layer 2: Card Issuing Infrastructure

Issuing infrastructure splits into two models: program managers and full-stack issuers.

Program managers work with sponsor banks holding Visa or Mastercard Principal Membership. They manage BIN sponsorship, compliance, settlement, and the conversion of crypto or stablecoins into fiat-compatible flows. They operate white-label platforms that enable third parties to launch branded cards. Examples include Baanx, Bridge, and Gnosis Pay.

Full-stack issuance platforms such as Rain and Reap collapse this stack. As Visa Principal Members, they issue cards directly on the network without intermediary sponsor banks. They combine BIN ownership, settlement, compliance, and often Lender of Record responsibilities into a single platform.

This structure captures value that traditionally leaked to banks and intermediaries. It also aligns with a stablecoin-native settlement future.

Both models coexist, but they compete for different layers of value.

Keep reading with a 7-day free trial

Subscribe to Fintech Wrap Up to keep reading this post and get 7 days of free access to the full post archives.