Using Data and AI to Combat Account-to-Account Payments Fraud; MiCA’s rules - what does MiCA hold for crypto businesses?; How Instant A2A Payment Wallets Challenge Card Dominance;

This week, we’re exploring the rise of instant A2A payment wallets challenging card dominance, AI’s role in fraud prevention, and the global evolution of Open Banking and crypto regulation

Insights & Reports:

1️⃣ How Instant A2A Payment Wallets Challenge Card Dominance

2️⃣ Using Data and AI to Combat Account-to-Account Payments Fraud

3️⃣ Design and Implementation of mCBDC Corridor Networks

4️⃣ Trends in Regional Adoption of Open Banking and Open Finance

5️⃣ AI Agents: Rival Frameworks and Their Design Choices

6️⃣ MiCA’s rules - what does MiCA hold for crypto businesses?

7️⃣ Exploring the Future of AI Agents in Crypto

8️⃣ India lifts WhatsApp payment curbs

9️⃣ Do Kwon pleads not guilty to US fraud charges in $40 billion crypto collapse

TL;DR:

In this edition of Fintech Wrap Up, we’re diving into some groundbreaking developments shaking up the payment, banking, and crypto ecosystems. Instant A2A payment wallets are on the rise, offering a compelling alternative to traditional cards. With features like merchant-funded rewards and pre-approved credit lines (think India’s UPI), they’re blending speed, security, and cost-effectiveness while tackling niches like micropayments and operational efficiency. However, challenges like interoperability and entrenched card systems still pose hurdles, especially in markets like the U.S. and U.K.

Fraud prevention is getting a high-tech upgrade as AI steps up to tackle real-time payment scams. From mule accounts to cross-network fraud schemes, AI’s dynamic, real-time capabilities are proving invaluable. Plus, customizable and explainable AI systems are helping financial institutions align with compliance and build trust.

We’re also spotlighting the mCBDC corridor network, which promises to revolutionize cross-border payments. By cutting out intermediaries, enabling 24/7 atomic settlements, and integrating advanced features like pre-validation and FX trade settlements, mCBDC networks aim to solve the inefficiencies of correspondent banking while maintaining financial system stability.

Open Banking is expanding globally, with regions taking diverse approaches. Europe sticks with regulation-led models, while APAC and Sub-Saharan Africa lean towards market-driven methods. Meanwhile, MiCA is setting the stage for crypto regulation in the EU, covering token offerings, stablecoins, and market abuse under a unified framework, leaving no corner of the crypto space untouched.

In the headlines, India lifted its WhatsApp payment limits, giving Meta a huge win in its largest market. Do Kwon pleaded not guilty to U.S. fraud charges over his infamous $40 billion crypto collapse, and Checkout.com’s collaboration with Noqodi is set to streamline payment processes and boost digital payments in the UAE.

Exciting times ahead in fintech! Let’s keep exploring the future together!

Insights

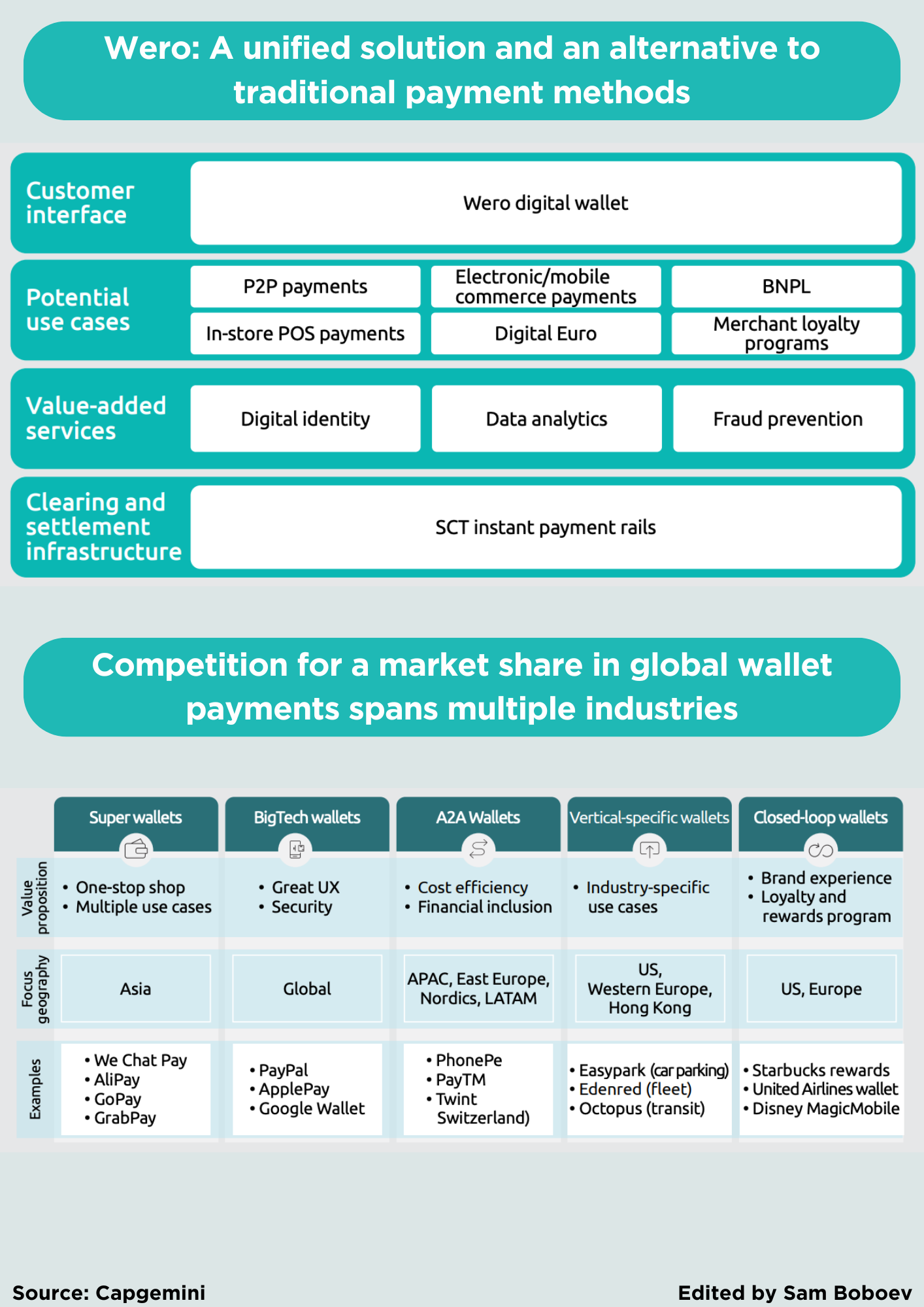

How Instant A2A Payment Wallets Challenge Card Dominance

Currently, card systems thrive on robust reward programs, structured dispute resolution mechanisms, and profitability derived from interchange fees. In 2022, the top six U.S. credit card issuers paid $68 billion in rewards while netting $32 billion in interchange fees. This profitability enables banks to maintain customer loyalty through travel points, cashback, and dispute resolution processes, which enhance the trustworthiness of card payments.

Emerging Opportunities for A2A Payments

Regulatory interventions, such as interchange fee caps in the EU, have created openings for merchant-funded reward systems (MFRs). Unlike traditional card rewards, MFRs incentivize A2A payment use by allowing merchants to pass on savings from lower transaction fees to customers as cashback or discounts. Additionally, innovations like India’s Unified Payments Interface (UPI) pre-approved credit lines, offering flexible repayment terms and lower fees, blur the lines between A2A wallets and credit cards. These developments demonstrate how A2A payments can combine speed, security, and cost-effectiveness while potentially replicating card-like functionalities.

Micropayments and Operational Efficiency

A2A wallets offer advantages in areas like micropayments, which are becoming a preferred alternative to traditional subscription models. Their lower fees make them ideal for small transactions, enhancing utility for businesses and gig workers. Furthermore, A2A payments improve operational efficiency by reducing fraud and chargebacks through direct account validation, which avoids the authorization complexities associated with card transactions.

Global Examples of A2A Innovation

In Europe, the European Payments Initiative (EPI) launched Wero, a mobile wallet aimed at simplifying person-to-person payments and reducing reliance on BigTech wallets like Apple Pay. With plans to expand into small business payments and loyalty programs, Wero seeks to consolidate Europe's fragmented payment landscape under a unified system. Similarly, the U.S. consortium behind Zelle is developing Paze, a card-based wallet to counter BigTech’s dominance, highlighting the increasing

Keep reading with a 7-day free trial

Subscribe to Fintech Wrap Up to keep reading this post and get 7 days of free access to the full post archives.