Three go-to-market approaches for banks to play in the Embedded Finance space; API Banking Ecosystem; Alipay & Revolut are redefining the future of finance;

In this week’s Fintech Wrap Up, I’m diving into PayPal’s bold reinvention, the rising importance of AI-powered fraud prevention, and the fintech IPO pipeline heating up with Stripe, Chime, and more.

Insights & Reports:

1️⃣ Three go-to-market approaches for banks to play in the Embedded Finance space

2️⃣ AI Agents - Identity’s Blind Spot: Non-Human Identities

3️⃣ These Are The Fintech IPOs That Could Follow Klarna’s Debut

4️⃣ AI-Powered Fraud Prevention and Security Solutions in Fintech

5️⃣ Robinhood vs SoFi – Q4 2024 Face-Off

6️⃣ API Banking Ecosystem

7️⃣ Alipay & Revolut are redefining the future of finance

8️⃣ Stablecoins – The future of money

9️⃣ PayPal Surpasses $30B in Global Small Business Lending

TL;DR:

Hey fintech fam 👋

This week’s edition dives deep into the evolving identity of some of fintech’s biggest players—and what that means for the rest of us. I took a closer look at PayPal 2.0 and its ambitious transformation from a payments giant to a full-blown commerce platform. Under new leadership, PayPal is leaning hard into omnichannel checkout, AI personalization, and even turning Venmo into more than just a peer-to-peer app. Big moves, but they’re up against heavy hitters like Stripe and Apple Pay—let’s see how it plays out.

Speaking of strategy, I also unpacked three go-to-market approaches for banks entering the embedded finance space: build, partner, or buy. Each has its trade-offs in speed, control, and cost, but all roads seem to lead to one thing—banks are no longer sitting on the sidelines.

On the tech front, identity and AI security are becoming major pain points, especially when it comes to non-human identities (NHIs)—think APIs, bots, and IoT devices. With 1 in 5 companies already hit by NHI-related security incidents, this is shaping up to be one of the biggest blind spots in IAM systems.

There’s also a growing wave of AI-powered fraud prevention tools—everything from scam detection and deepfake defense to next-gen credit scoring and KYB checks. Companies like SEON, Veriff, and Feedzai are turning compliance and fraud management into AI-first workflows, and it’s changing how the industry operates.

Wondering who might follow Klarna into the IPO spotlight? I rounded up the usual suspects: Stripe, Chime, Circle, and MoonPay, among others. There’s even movement from Asia-Pacific with players like Airwallex, Xendit, and Mynt making noise. Let’s hope the public markets stay receptive.

Meanwhile, in the great fintech showdown—Robinhood vs. SoFi—I broke down their Q4 2024 stats. Robinhood has the edge in margins and capital efficiency, while SoFi is playing the long game with steady growth. Tough call for long-term investors.

In platform news, Alipay and Revolut are redefining what a financial app looks like in 2025. Alipay is now a full-blown super app for 1.6B users, and Revolut is climbing fast with 50M users and a product offering that just doesn’t quit. Both are blueprinting the future of embedded finance—AI, API ecosystems, and seamless UX are now table stakes.

API Banking and BaaS are also pushing traditional finance to open up, share data, and embed services into new digital experiences. It’s all about real-time, always-on, customer-first models now.

And in this week’s headlines: PayPal crossed $30B in small business lending, Mesh launched crypto payments on Shopify, and Charlie Javice was found guilty of defrauding JPMorgan Chase. Yep, it's been a week.

Until next time, stay curious and stay ahead 🚀

Insights

Deep Dive: PayPal 2.0 - Not Only Payments

In this Deep Dive edition of Fintech Wrap Up, we’re taking a closer look at PayPal 2.0—how one of the biggest names in fintech is reinventing itself for the next era of digital commerce. With $1.7 trillion in payment volume and over 400 million active accounts, PayPal has long been a dominant force, but intense competition has forced it to rethink its approach. Under CEO Alex Chriss, the company is moving beyond just payments to become a full-fledged commerce platform. This means a bigger push into omnichannel payments, AI-driven personalization, and merchant tools designed to boost customer acquisition and loyalty. PayPal is also overhauling its tech infrastructure with a unified platform strategy, integrating AI across fraud detection, payments, and customer experience. On the business side, it’s doubling down on branded checkout, expanding in-store payments via a partnership with Verifone, and transforming Venmo from a simple peer-to-peer app into a broader commerce and money management platform. Of course, with big moves come big challenges—PayPal is up against Stripe, Apple Pay, and BNPL players, while also navigating regulatory pressures and shifting consumer behaviors. But if its execution matches its ambition, this could be a defining moment for PayPal’s next chapter. Will it pull off the transformation and cement itself as the go-to platform for digital commerce? The groundwork is being laid in 2025, and we’ll be watching closely.

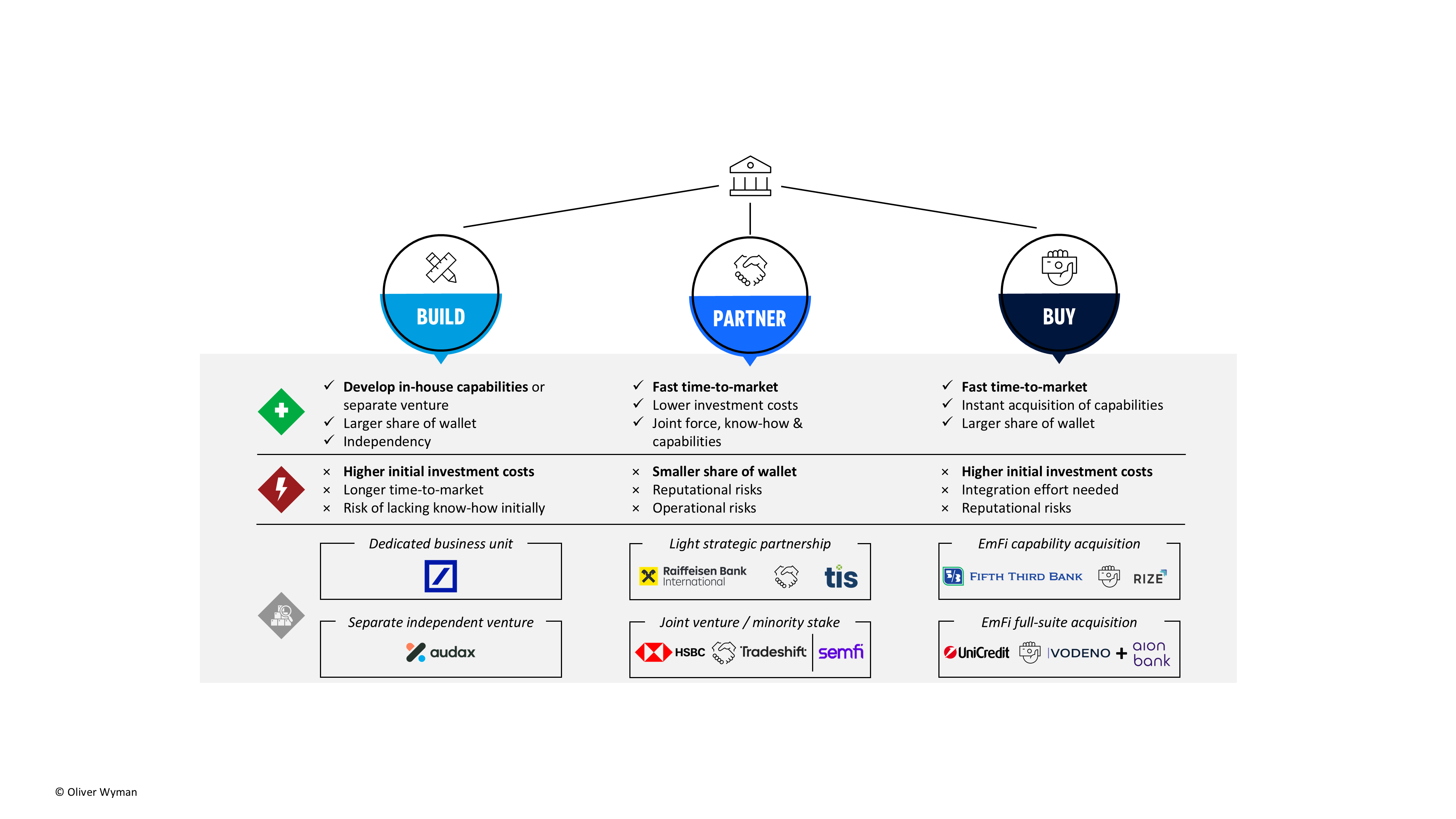

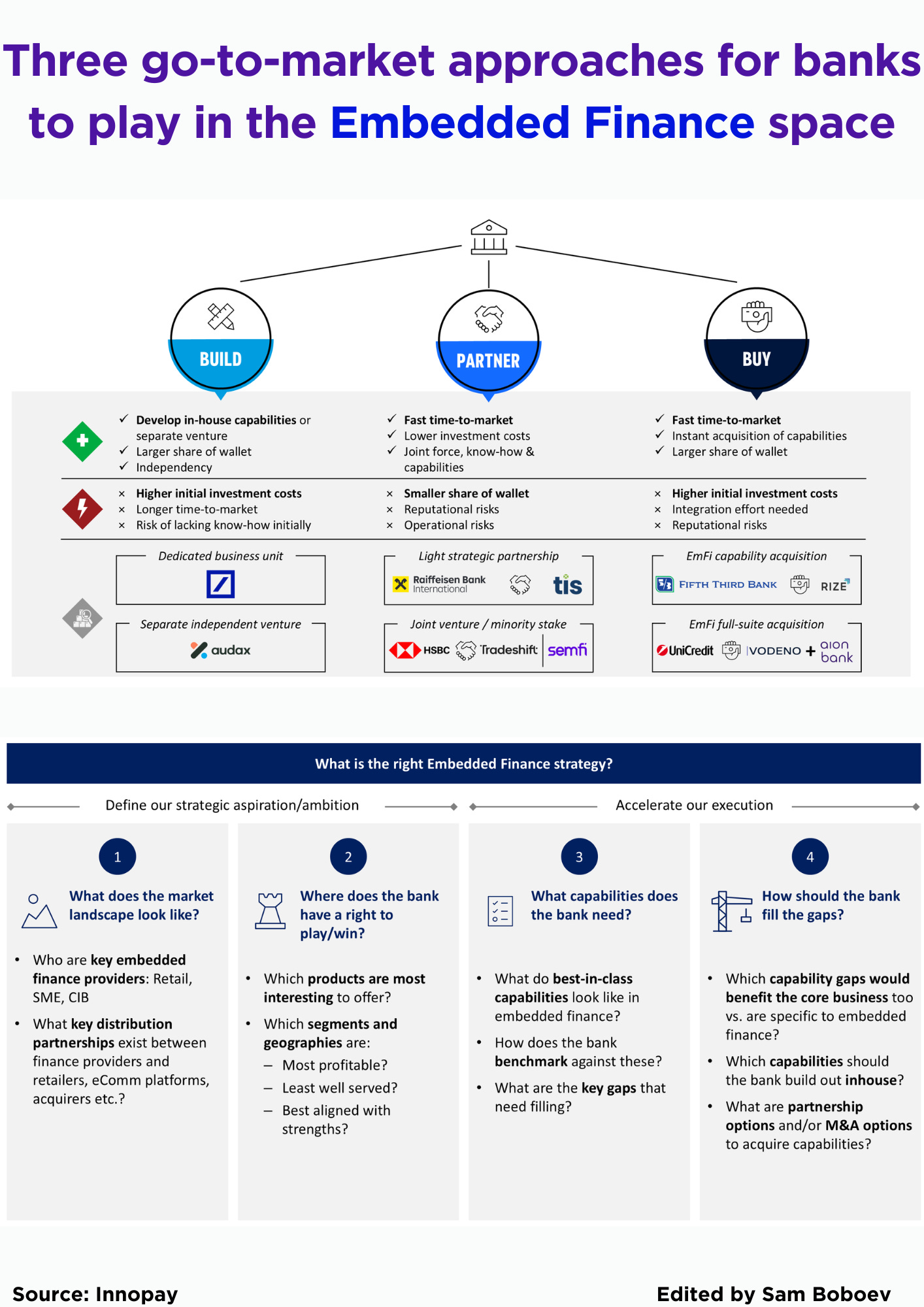

Three go-to-market approaches for banks to play in the Embedded Finance space

A. Build

Setting up a dedicated business unit or launching a new venture within a group can help to bundle resources to build capabilities and know-how in-house. This mitigates the risk of dependencies with other partners or acquired businesses. Furthermore, full share of wallet remains at the bank. Typically, banks either keep the business unit in-house or separate it into an independent venture, that is not burdened by corporate processes. This approach can also change along the way, as described in the case study further below in this blog.

However, this is typically associated with higher investment costs and longer time-to-market, as capabilities need to be developed in-house and require therefore patience, senior executive commitment and willingness to invest.

B. Partner

A less investment-heavy approach is to join forces with other relevant tech providers – thus combining capabilities and know-how of both parties.

Keep reading with a 7-day free trial

Subscribe to Fintech Wrap Up to keep reading this post and get 7 days of free access to the full post archives.