The EU’s open finance regulatory framework; The use cases for Super-Apps across industries; How SaaS platforms can unlock the Embedded Finance opportunity;

In this edition of Fintech Wrap Up, we’re exploring the transformative power of open banking, the strategic tech investments reshaping banks, and the exciting rise of super-apps in finance.

Insights & Reports:

1️⃣ Banking Model: Journey from Traditional Digital Banking to Open Banking and Data

2️⃣ The EU’s open finance regulatory framework

3️⃣ Unlocking value from technology in banking: An investor lens

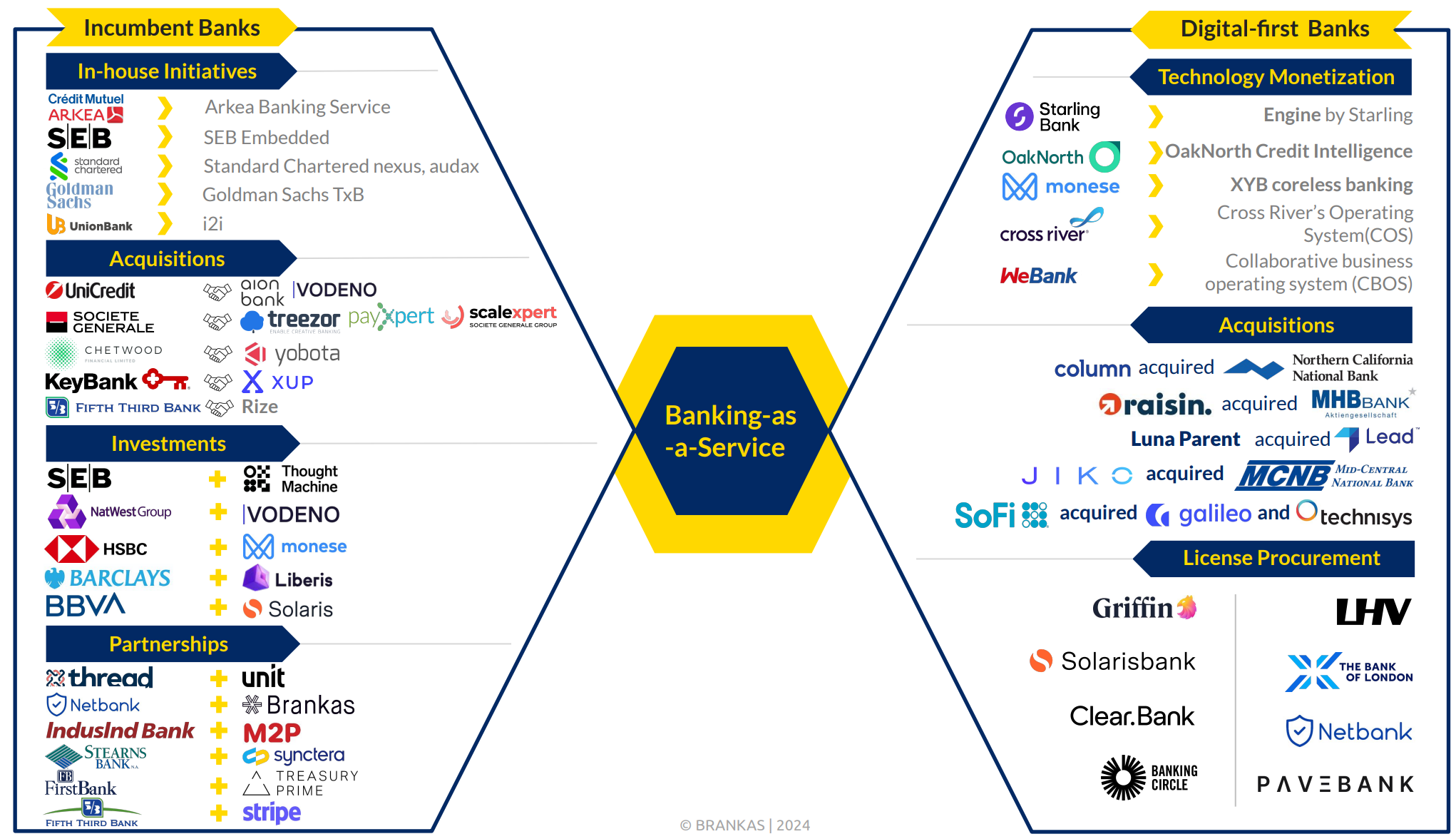

4️⃣ Banks’ BaaS Playbook

5️⃣ Omnichannel Payment Proposition

6️⃣ BaaS in the Crosshair

7️⃣ The use cases for Super-Apps across industries

8️⃣ How SaaS platforms can unlock the Embedded Finance opportunity

9️⃣ Standard Chartered Taps Wise for Faster, Cheaper International Payments

TL;DR:

Hey everyone! Welcome to the latest Fintech Wrap Up!

First up, we’re seeing a fundamental shift as open banking evolves toward open finance and open data, enabling a much wider scope of services by allowing customer data to be securely shared across banks and third parties. While the EU leads with regulatory frameworks like FiDA, PSD3, and PSR, other regions are experimenting with market-driven approaches. The goal? Seamless integration and standardization, making financial services more accessible and innovative for everyone.

Banks are also working to unlock value from massive tech investments, which are rising even as productivity in the sector has stalled. Banks are starting to focus more on strategic, outcome-based tech spending, aligning investments with clear business objectives to drive value—essential for staying competitive in today’s crowded market.

In the BaaS space, large and mid-size banks are teaming up with brands like Amazon and PayPal, blending financial products directly into everyday digital experiences. It’s an exciting time, as these partnerships are opening up new possibilities for underserved segments and offering highly personalized solutions.

Super-apps are gaining traction too, consolidating everything from payments and financial planning to e-commerce and transportation in a single app. This one-stop-shop approach is transforming customer experiences across industries.

On the payments front, omnichannel solutions are a major focus for both small and enterprise merchants, offering unified tools to manage payments across platforms—from POS systems to online shopping carts.

To wrap up, here are some curated updates: Zing just launched automatic top-ups through Visa’s Tink, making wallet refills a breeze. Standard Chartered partnered with Wise for faster, cost-effective international transfers across Asia and the Middle East. And in Singapore, Swift, UBS, and Chainlink piloted a tokenized fund settlement, hinting at the future of blockchain-based finance.

I hope you enjoy this issue and stay tuned for more insights on the latest fintech trends!

Insights

Banking Model: Journey from Traditional Digital Banking to Open Banking and Data

Fundamentally, open banking comes down to who owns data and how to use it. As data is more freely shared, new operating models have begun to emerge, allowing for the development of innovative services and new ways to deliver them to the customer.

Traditionally, banks have been the custodians of customer financial data. With open banking, customers can consent to securely share their data across multiple financial institutions with third parties.

Open banking does not preclude earlier operating models – banks can still offer dedicated apps within their own ecosystems for customers who do not consent to data sharing. Instead, open banking widens the scope of what is possible.

Open banking itself can be seen as an intermediate step towards what many executives refer to as open finance or open data. In a fully realized open data system, not only financial data but data across a multitude of sources – including utilities, government, and others – can be securely aggregated into an innovative ecosystem. This allows for the provision of a wide range of services to customers and businesses, conveniently accessible via their preferred digital platform.

Four key steps in the open banking journey:

🔹 Digital Banking, with one bank providing its own digital banking services to its own customers.

🔹 Walled Garden, with one bank providing enhanced services including from third-party providers (TPP) all via its own customer app.

🔹 Open Banking, as data is more freely shared, customers access financial services from any bank or TPP via their preferred third-party or bank app.

🔹 Open Data, whereby customers can now access financial as well as a wide range of other services provided by banks and TPPs via any third-party or bank app.

Keep reading with a 7-day free trial

Subscribe to Fintech Wrap Up to keep reading this post and get 7 days of free access to the full post archives.