The Credit Decisioning Process; Stablecoins: Bridging Traditional Finance and the Digital Economy; Neobanks - Users vs Revenue per User

This week in Fintech Wrap Up, we explore MENA’s rising fintech infrastructure, Shopify’s unstoppable growth, and the evolving role of stablecoins in global finance

Insights & Reports:

1️⃣ MENA’s Financial Future Demands a New Kind of Financial Software

2️⃣ A six-point plan for navigating the new reality for consumer finance companies

3️⃣ The Credit Decisioning Process

4️⃣ Deep Dive: Enhancing the Travel Booking and Payment Process with Blockchain and AI

5️⃣ Future Distributed Ledger Technology (DLT) - Based Ecosystem

6️⃣ Stablecoins: Bridging Traditional Finance and the Digital Economy

7️⃣ How do Stablecoins Work?

8️⃣ Neobanks - Users vs Revenue per User

9️⃣ Robinhood To Acquire WonderFi

TL;DR:

Welcome to a new edition of the Fintech Wrap Up newsletter!

MENA is undergoing a major financial transformation, and the push toward digitization—especially in countries like Saudi Arabia—is accelerating fast. With digital payments growing by 75%, there’s a rising need for modern financial infrastructure. Yet, the region lacks a clear leader equivalent to Marqeta or Unit. Stitch aims to fill that gap with a unified, modular platform that caters first to licensed players, flipping the global playbook by embedding compliance from the start. It’s positioning itself as the “CNAPP of BFSI”—simplifying fragmented infrastructure into one system for banks and fintechs to build, launch, and scale products seamlessly.

Meanwhile, Shopify continues to dominate the global commerce ecosystem, reporting $2.4B in Q1 2025 revenue and facilitating $1.2T in GMV since its inception. The company now powers over 12% of U.S. ecommerce, and its merchant-first model is proving resilient with consistent 20%+ YoY growth. Its scale, coupled with high merchant engagement (875M shoppers in 2024), cements its role as the operating system for modern commerce.

Consumer finance firms are also at an inflection point. A new six-point strategy—from funding diversification and embedded credit to AI-powered collections—is essential for staying relevant in an evolving landscape. Real-time underwriting and personalized experiences will separate tomorrow’s winners from the rest.

Credit decisioning has come a long way from manual processes to advanced AI models and SaaS platforms. Today, it's all about combining structured data, predictive models, and configurable rules to enable instant, scalable, and compliant credit workflows.

On the travel front, blockchain and AI are teaming up to revolutionize how we book and pay for trips. Imagine AI agents autonomously booking trips using stablecoins—with built-in budgets and automated reimbursements. This is more than futuristic talk; it’s a glimpse into how Web3 and AI will reshape user experiences across sectors.

That same vision extends to DLT in capital markets. Despite potential in tokenization and digital securities, fragmented infrastructure and regulatory inconsistencies remain serious hurdles. Success depends on industry-wide collaboration and standards.

Stablecoins are also stepping into the spotlight, bridging traditional finance with the digital economy. With over $230B in circulation and rapid adoption across cross-border payments, merchant transactions, and DeFi, they are becoming foundational to next-gen financial infrastructure. Trusted coins like USDC and USDT dominate the space, but the ecosystem continues to evolve rapidly.

And finally, neobanks are revealing a clear divide: scale vs. revenue per user. While players like Nu and WeBank focus on mass adoption, Starling and Wise lead in monetization. As the sector matures, sustainable unit economics—not vanity metrics—will shape the next era of digital banking.

That’s it for this edition. As always, thanks for reading Fintech Wrap Up!

Insights

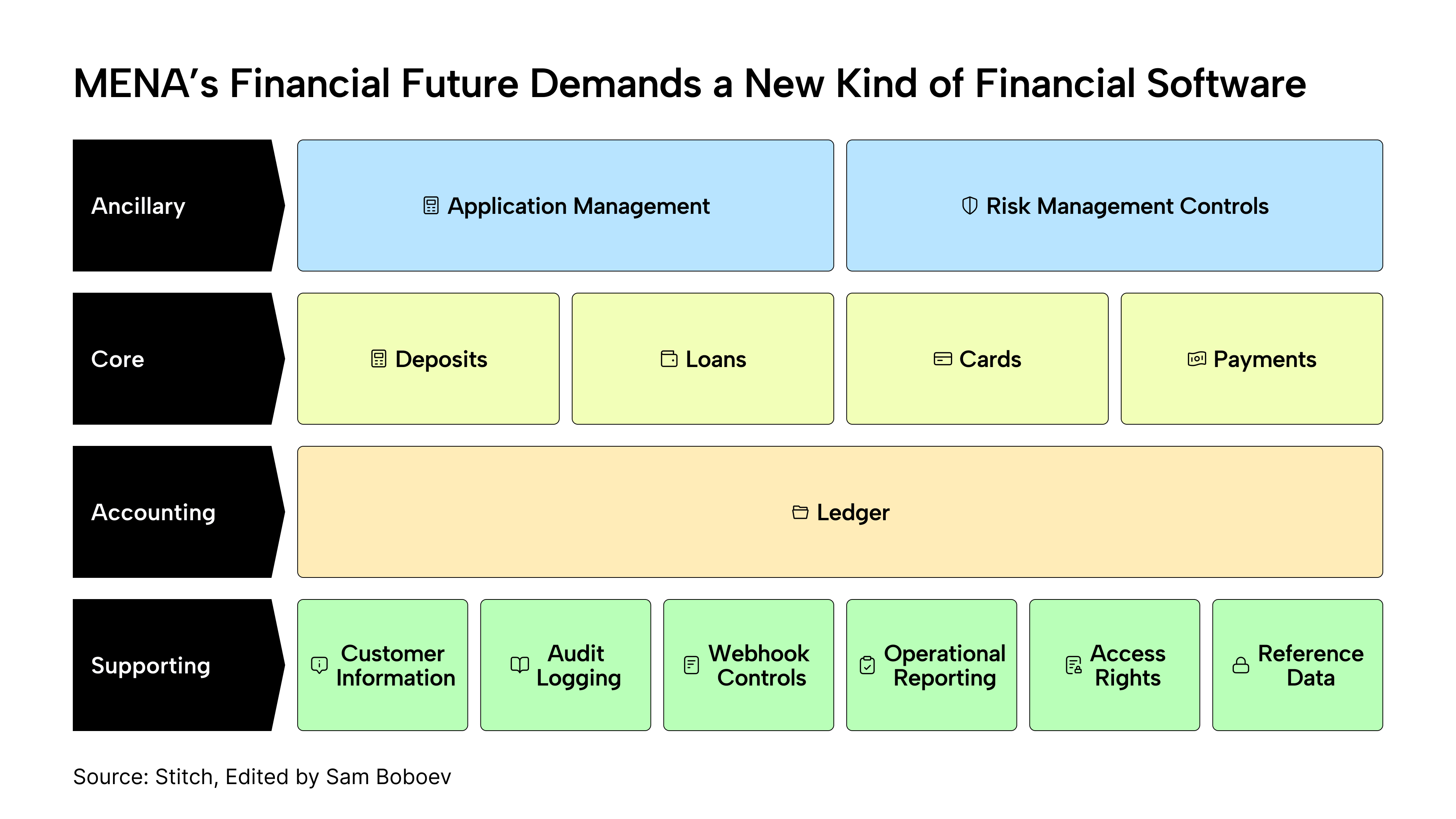

MENA’s Financial Future Demands a New Kind of Financial Software

The MENA region is moving fast. Take Saudi Arabia as an example. What was once an oil-driven economy, is redefining its digital future through Vision 2030 with the FSDP at the heart of it. And the impact is already clear with non-cash transactions and digital payments growing by 75%.

But what’s powering this growth behind the scenes?—Modern financial infrastructure.

🔹 A $65B Opportunity—With No Regional Leader

Across MENA, institutions are bumping up against the same problem: legacy tech. The region has no dominant player building infrastructure for regulated financial institutions, an equivalent of what Marqeta is to card issuing or what Unit is to embedded banking in the U.S.

And yet, the need is massive.

The global BFSI software market is projected to hit USD 221.39 billion by 2033, driven by a growing demand for infrastructure that’s built for regulation, scale, and modern product delivery. But instead, they’re met with fragmentation—having to juggle vendors for ledgering, compliance, onboarding, risk, and more.

🔹 Compliance vs Product—What Comes First?

Globally, infrastructure providers like Marqeta, Highnote, and Synctera have followed a common playbook: start with unregulated players, solve for compliance, then build the tech to follow.

One player, Stitch, is flipping the playbook. Stitch is the first unified platform purpose-built for the MENA region—a full operating system, offering modular infrastructure across key financial verticals; ledgers, deposits, cards, lending, and beyond.

This approach—starting with licensed players and solving the technology layer first—is Stitch’s answer to the region’s infrastructure gap. Why? Because this is where long-term stability lives.

The platform soon will extend support to non-regulated businesses too—by building compliance and onboarding directly into the platform. They’re creating a regulatory wrapper that allows institutions to plug in, stay compliant, and go to market with confidence.

The goal? A single platform for any business—licensed or not—to create, launch, and operate a financial product.

Stitch is to banking infrastructure what CNAPP was to cybersecurity

In cybersecurity, CNAPP unified fragmented security tools into one platform. Stitch is doing the same for BFSI infrastructure in MENA.

Even licensed financial institutions don’t want to operationally juggle multiple technical partners, nor does ‘going the system integrator route’ truly solve the problem. Integrators just stitch together a patchwork of tools, leaving institutions with the same problems.

What these institutions need is a product-led partner. And that’s what Stitch delivers.

🔹 Building the Financial Backbone of MENA

As the wider MENA region enters the next phase of financial transformation, the winners won’t be those with the most flashy front-ends. They’ll be the ones with unified infrastructure allowing them to move fast, integrate seamlessly, and ship with confidence.

Deep Dive: Shopify - The Operating System of Commerce

Shopify’s scale in commerce is staggering. The company reported $2.4 billion in revenue in Q1 2025, a 27% year-over-year jump. Gross merchandise volume (GMV) flowing through Shopify’s platform continues to surge – since its 2006 launch, Shopify has facilitated over $1.2 trillion in global commerce. In 2024 alone, more than 875 million unique shoppers purchased from Shopify merchants. Shopify now powers millions of merchants across 175+ countries, giving it an over 12% share of the U.S. ecommerce market – an extraordinary penetration for a company that started as a tiny Canadian snowboard shop’s website.

Shopify’s growth at scale is notably robust. In 2023, revenue grew about 20%, and in 2024 it accelerated to 24% year-over-year. GMV has also expanded at ~26% yearly in recent years, reaching roughly $292 billion in 2024 GMV. This means Shopify is not only growing, but gaining market share in global retail. As management notes, the company has sustained 20%+ GMV and revenue growth at scale for the past two years – a feat in a maturing ecommerce landscape. Shopify’s model of sharing in merchant success (“when our merchants become more successful, Shopify becomes more successful”) is clearly working.

Shopify Snapshot (Q1 2025): Shopify’s recent investor deck highlights its scale and growth – $2.4B revenue in Q1 2025 (27% YoY), $1.2T in total commerce since inception, 875M+ shoppers in 2024, and >12% of U.S. ecommerce share. These figures underscore Shopify’s outsize presence in global commerce.

Keep reading with a 7-day free trial

Subscribe to Fintech Wrap Up to keep reading this post and get 7 days of free access to the full post archives.