The card payments ecosystem and the 4-party model; Generative AI in Accounting: Jobs To Be Done (JTBD); How B2B payment processing works;

In this edition of Fintech Wrap Up, we’re diving into the latest trends in fintech mergers and acquisitions, the transformative potential of asset tokenization, and the booming embedded finance market

Insights & Reports:

1️⃣ Unveiling fintech M&A deal details

2️⃣ The Asset Tokenization Process

3️⃣ How B2B payment processing works

4️⃣ Generative AI in Accounting: Jobs To Be Done (JTBD)

5️⃣ The card payments ecosystem and the 4-party model

6️⃣ The Embedded Finance Market Will Be Worth More Than $320 Billion in Revenues by 2030

Curated News:

1️⃣ Goldman Sachs Deploys Its First Generative AI Tool Across the Firm

2️⃣ Point72 Ventures ditches fintech team

3️⃣ Rainforest lands $20M to challenge Stripe with embedded payments for SaaS providers

TL;DR:

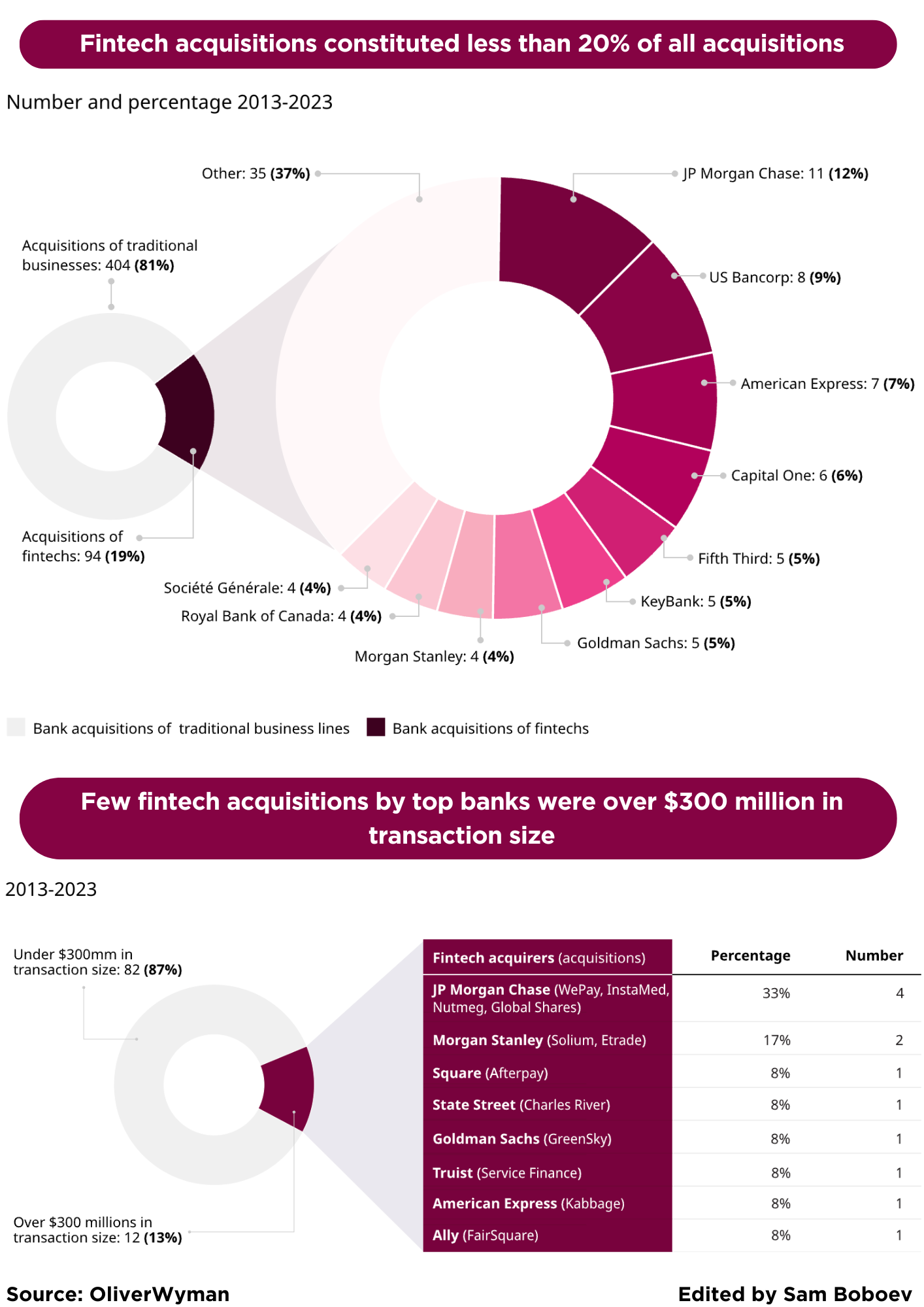

Have you noticed all the buzz around fintech M&A lately? We’ve got the scoop on why, despite an average of $3.5 trillion in global acquisition activity per year over the last decade, a whopping 90% of these deals fail due to poor implementation. Fun fact: bank-fintech acquisitions make up less than 1% of all fintech transactions. Among the top 50 U.S. and top 15 international banks, only 94 out of 500 acquisitions since 2013 were fintechs, with payments and lending tech firms leading the charge. Most deals are small, like under $300 million, making them easier to integrate.

Switching gears, let’s talk about asset tokenization. This process, from deal structuring to secondary market trading, is pretty cool. It involves creating a digital twin of a physical asset on the blockchain, boosting liquidity and simplifying ownership records. Imagine owning a piece of real estate as a token!

Now, onto B2B payment processing. These transactions are between businesses and often involve big sums and long payment terms. The shift to electronic invoicing is speeding things up, and security measures like encryption are crucial for protecting data. Compliance with regulations like AML and KYC is also a big deal to avoid legal headaches.

Generative AI is making waves in accounting too. It’s automating data collection, enhancing research accuracy, and helping accountants provide ongoing financial advice. This means more time for accountants to focus on value-added services.

Ever wondered how card payments work? The four-party model, involving the merchant, cardholder, issuer bank, and acquirer bank, is key. Marqeta is shaking things up with innovative transaction authorizations and API integrations that make the process smoother and more efficient.

Embedded finance is another hot topic. This market is projected to hit $320 billion in revenue by 2030. It’s all about integrating financial services into everyday interactions, making transactions seamless. Stripe and Adyen have already crossed the trillion-dollar mark in payment volumes, and the growth in embedded lending and insurance is impressive too.

In our curated news, Goldman Sachs is rolling out a generative AI tool for code generation, Point72 Ventures is making some big changes to its fintech team, and Rainforest has raised $20M to challenge Stripe with embedded payments for SaaS providers.

Stay tuned for more insights and updates!

Insights

Unveiling fintech M&A deal details

Have you noticed or read any news on fintech M&A, lately? In this post, we will learn the details of fintech M&A deal details

Mergers and acquisitions in general are common — the last 10 years saw an average of $3.5 trillion per year in acquisition activity worldwide and in 2022, an average year, 50,000 deals were completed. However, deal volume is not correlated with success, as 90% of M&A transactions fail long-term due to poor implementation and post-deal strategy complications, according to the Harvard Business Review.

Despite the synergies, banks have often been a lower priority for fintech boards and executives looking to exit compared to the public markets, private equity, enterprise technology, and other fintechs. Overall, out of all fintech transactions in the market, bank-fintech acquisitions account for less than 1% of deals.

Among the approximately 500 whole-company acquisitions undertaken by the top 50 US and top 15 International and Canadian banks since 2013, only 94 or less than 20% were fintech acquisitions. The top acquirers were US based, ranging from across Global Systemically Important Banks (GSIBs) to regional banks and other institutions. Most of the remaining 400-plus deals were acquisitions of traditional lines of business such as lending, wealth management, or investment banking.

Over half of the 94 bank-fintech acquisitions consisted of payments and bank / lending tech firms, with financial management solutions, wealth tech, and healthcare fintechs making up the remainder.

Bank-fintech acquisitions skewed toward the smaller end of the deal spectrum: across the 94 deals in total, only 13% had announced deal sizes greater than $300 million. This figure represents the midpoint of the materiality hurdle cited in expert interviews and is in line with capital requirements and goodwill impacts cited by experts with both bank and fintech backgrounds. While there are exceptions, such as Goldman Sachs’ acquisition of GreenSky for $1.8 billion and Morgan Stanley’s acquisition of E*Trade for $13 billion, the vast majority of bank and fintech combinations are relatively small because smaller deals are more easily integrated, less dilutive and less impactful to bank performance overall. Even the most prolific bank acquirers have mostly followed the same pattern of pursuing smaller transactions.

Successful deals are unlocked when banks see value greater than the cost of acquiring a fintech, and good deals remain the exception to the rule from the bank point of view. With this perspective, deal size and volume over the past decade is rational, though we note that 77% of the 94 deals in the cohort have taken place since 2018. We expect this pace to continue as banks refine M&A-ready use cases and fintech valuations continue to fall

Source Oliverwyman

Keep reading with a 7-day free trial

Subscribe to Fintech Wrap Up to keep reading this post and get 7 days of free access to the full post archives.