Reports: Tokenization 2030; The Race for Frictionless Machine Payments; The emerging architecture of on-chain money

This week’s reports highlight the convergence of AI, digital assets, and next-generation payment infrastructure. Citi’s Tokenization 2030 projects tokenized assets could reach $5.5–8 trillion by 2030, driven by tokenized equities, treasuries, and the growing adoption of digital money for settlement. The Race for Frictionless Machine Payments examines how AI agents are creating demand for a new payment stack built on stablecoins and low-cost blockchain rails, with protocols such as x402, MPP, AP2, and Visa’s initiatives forming the foundations of machine-to-machine commerce. Meanwhile, McKinsey’s The Emerging Architecture of On-Chain Money argues that while stablecoins continue to gain attention, tokenized deposits and bank-led digital money networks are already processing significantly larger volumes, suggesting the future financial system will likely consist of interoperable layers of stablecoins, tokenized bank deposits, and eventually central bank digital money. Together, these reports point to a future where programmable assets, autonomous agents, and on-chain settlement infrastructure reshape how money moves across both consumer and institutional markets.

Video of the Week

Deep Dive of the Week

The Directory Of The UK and European Card Issuing and Program Management Platforms

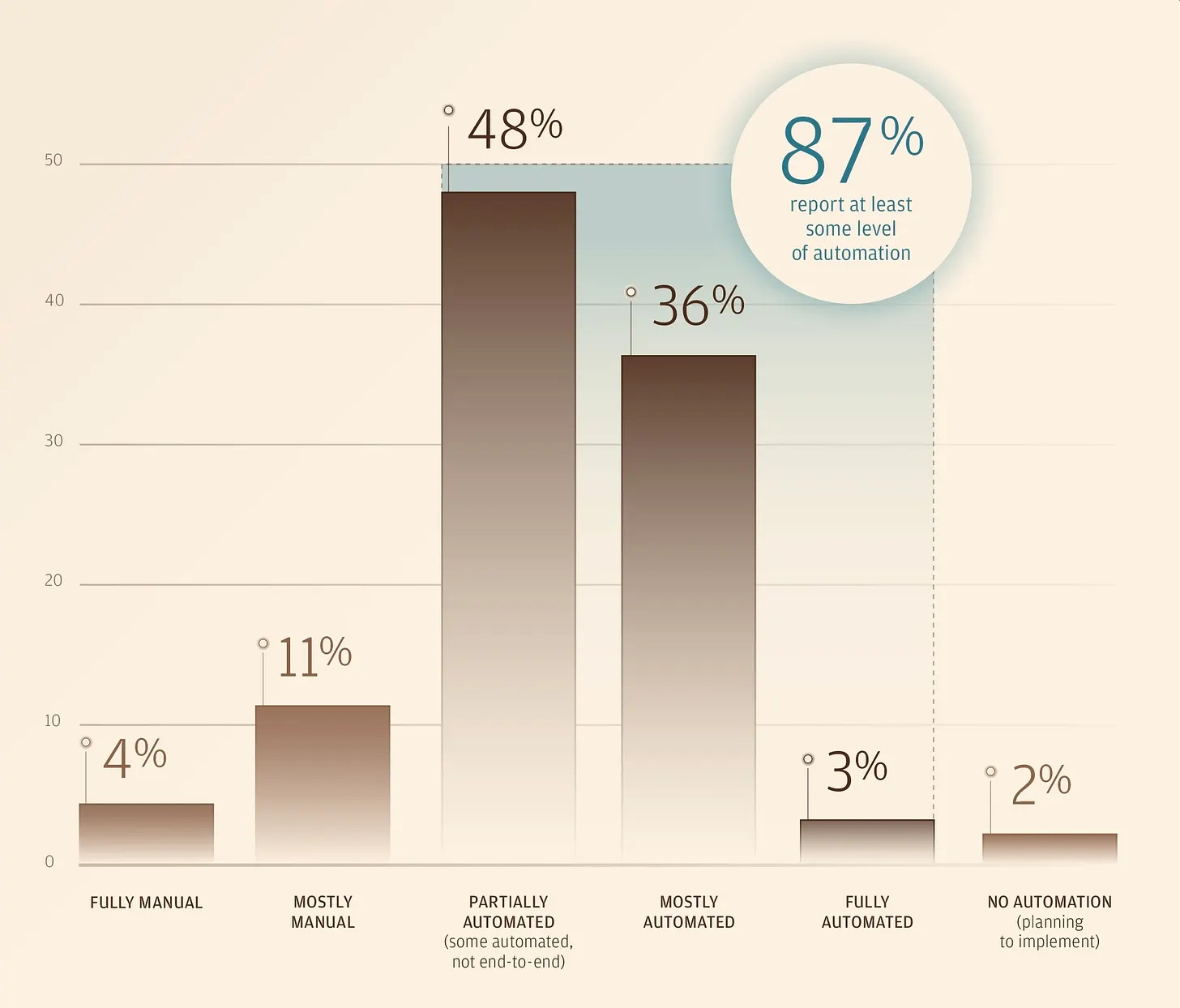

The card issuing space has never been harder to read from the outside. Platforms that look similar on the surface have fundamentally different license structures, network relationships, regional coverage, and feature depth. I built this guide to cut through the noise mapping 22 companies across every dimension that actually matters when choosing a card issuing partner. If you are building a card program, migrating an existing one, or doing competitive due diligence on this market, this is the reference you need. The companion Excel file gives you the full comparison in filterable form.

What this guide covers

This deep dive profiles 22 card issuing processors and program management platforms in the UK and Europe across six structured dimensions: license type and issuing jurisdiction, card network membership, card types supported, key platform features, and geographic coverage. Every profile is built from publicly available information and official company documentation as of June 2026. Where data is not publicly disclosed, I mark it as “Not disclosed” rather than guess.

The accompanying file has seven tabs: Overview, Licenses, Card Networks, Card Types, Features, Regions, and a Master Table with all dimensions combined and filterable.

This week’s reports

1️⃣Five shifts powering payments

2️⃣The Race for Frictionless Machine Payments

3️⃣The emerging architecture of on-chain money

4️⃣Digital Assets & the Future of Wholesale Banking

5️⃣SWOT Assessment of Agentic Commerce for Retailers

6️⃣Tokenization 2030

7️⃣x402: Unlocking The Internet’s Missing Payment Layer

Five shifts powering payments

One of the interesting insights for me is that by 2030, agentic commerce is expected to total around $2-$5 trillion, representing between 3-7% of global payment volumes.

In this omnichannel world, a new form of shopping has the potential to change the way people shop forever—agentic commerce.

Agentic AI is expected to be responsible for up to a quarter of the U.S. e-commerce market by 2030. Consumers can use agentic AI to autonomously perform a range of shopping tasks including searching for products; searching for where to buy those products; reading reviews or product specifications; making recommendations; and finally, completing the purchasing journey on their behalf.

For now, agentic commerce is primarily used for product discovery: 30% of consumers now use AI tools to research products and compare options.34 However, we believe agentic AI will rapidly move up the commerce value chain, starting with repeat, low-risk items like groceries, before including more high-value items like tickets, travel and even automobiles.

For businesses, adapting to agentic commerce means adopting “sell-side” AI agents that will manage inventory and pricing, and interacting with “buy-side” AI agents by marketing their goods to them and ensuring their products are chosen over a competitor’s. In a world where AI agents are making purchase decisions, the concept of brand loyalty may no longer be as powerful. AI agents may turn their focus on objective factors such as price, stock availability and how fast purchases can be delivered. This can be both a challenge and an opportunity for merchants.

These processes may not only exist online. AI is also going to transform areas such as customer support, where AI-powered chatbots or virtual assistants can provide on-demand or proactive support to help customers with queries or resolve issues such as returns or payment problems. Gartner believes that by 2028, 60% of brands will use AI agents to interact with customers, which will act like “digital concierges.”

Keep reading with a 7-day free trial

Subscribe to Fintech Wrap Up to keep reading this post and get 7 days of free access to the full post archives.