Reports: How Digital Assets Are Reshaping the Foundations of Finance; Digital Money – a perspective on stablecoins, tokenised deposits, and CBDCs; Digital Assets

This week’s reports underscore the rapid convergence of digital assets, AI, and traditional finance. Stablecoins, tokenized deposits, and central bank digital currencies are emerging as complementary forms of digital money, supported by improving regulation and institutional adoption. Digital assets are moving beyond crypto speculation into mainstream banking, with tokenized real-world assets, programmable money, and blockchain-based settlement creating new revenue opportunities and operational efficiencies. AI-driven machine-to-machine payments are also gaining traction, enabled by protocols such as x402 that allow autonomous agents to transact without human intervention. Meanwhile, e-commerce continues to reshape banking, as traditional lenders seek to close credit gaps by leveraging richer merchant data and alternative underwriting models. Financial institutions are being urged to capitalize on strong profitability by investing in AI, digital assets, and scalable operating models to drive long-term growth. However, regulatory uncertainty remains a key obstacle, particularly for stablecoins, where differing frameworks across jurisdictions could influence where innovation and capital flow. Collectively, the reports suggest the financial industry is transitioning toward a more programmable, interoperable, and AI-enabled ecosystem, with success depending on modern infrastructure, regulatory clarity, and the ability to integrate digital assets into core financial services.

Video of the Week

Deep Dive of the Week

The Directory of US Card Issuing and Program Management Platforms

I mapped 19 of the platforms that issue and process cards in the US market, because from the outside they all describe themselves the same way and the differences that matter are buried in license structure, network access, and who actually holds the BIN. This guide sorts them into five categories and profiles each one across license type, networks, card types, features, and regional coverage. It ships with a companion Excel file so you can compare every platform side by side and filter on the dimensions you care about. I built it for anyone choosing an issuing partner, migrating a live program, or running competitive diligence on this market. Every data point comes from official sources and public disclosures as of June 2026, and where something is not disclosed I mark it that way instead of guessing.

This week’s reports

1️⃣Banking on e-commerce

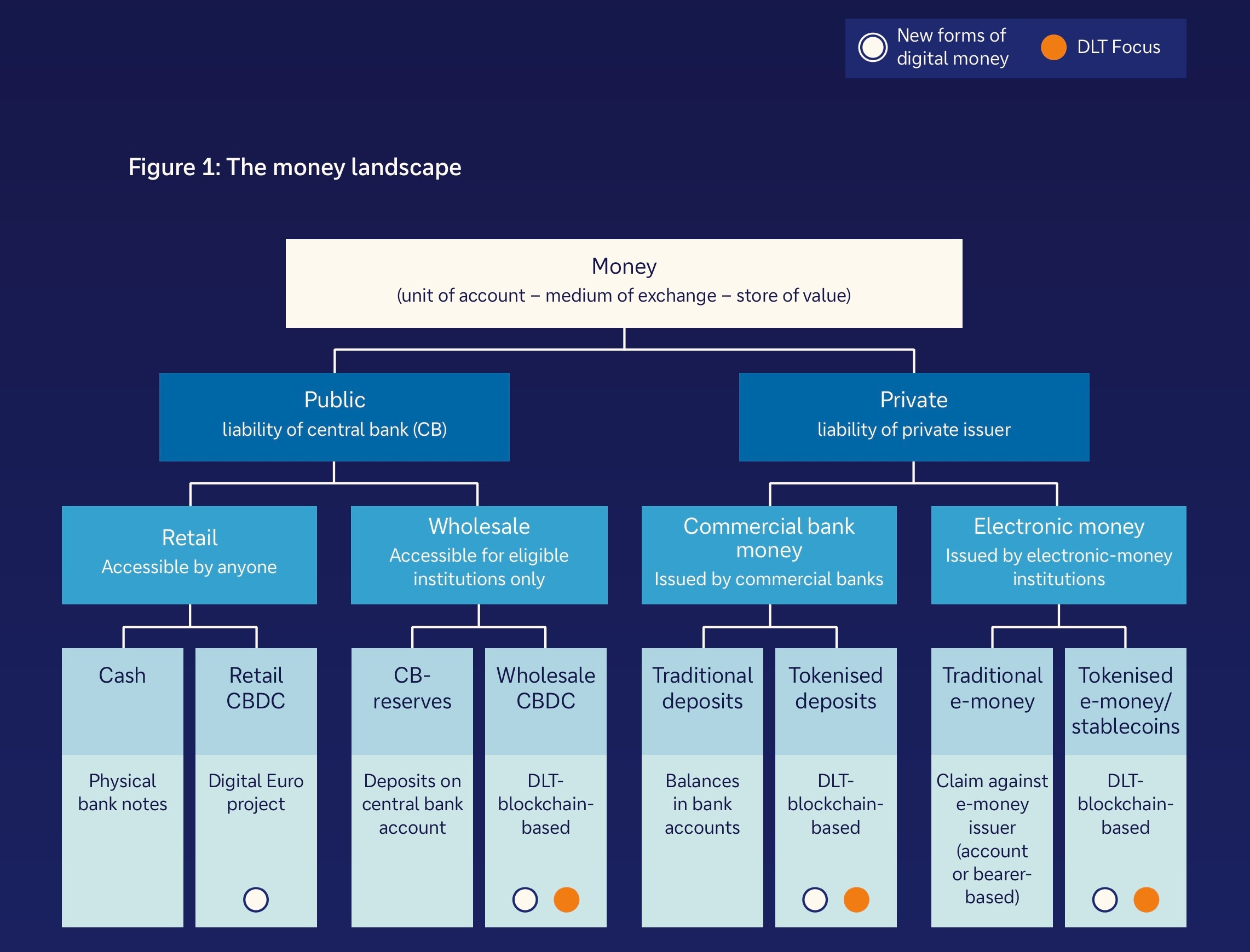

2️⃣Digital Money – a perspective on stablecoins, tokenised deposits, and CBDCs

3️⃣How Digital Assets Are Reshaping the Foundations of Finance

4️⃣Mapping the top 100 stablecoins and their future

5️⃣Time to Shift Gears?

6️⃣Digital Assets

7️⃣Stablecoins: waiting for regulation

Banking on e-commerce

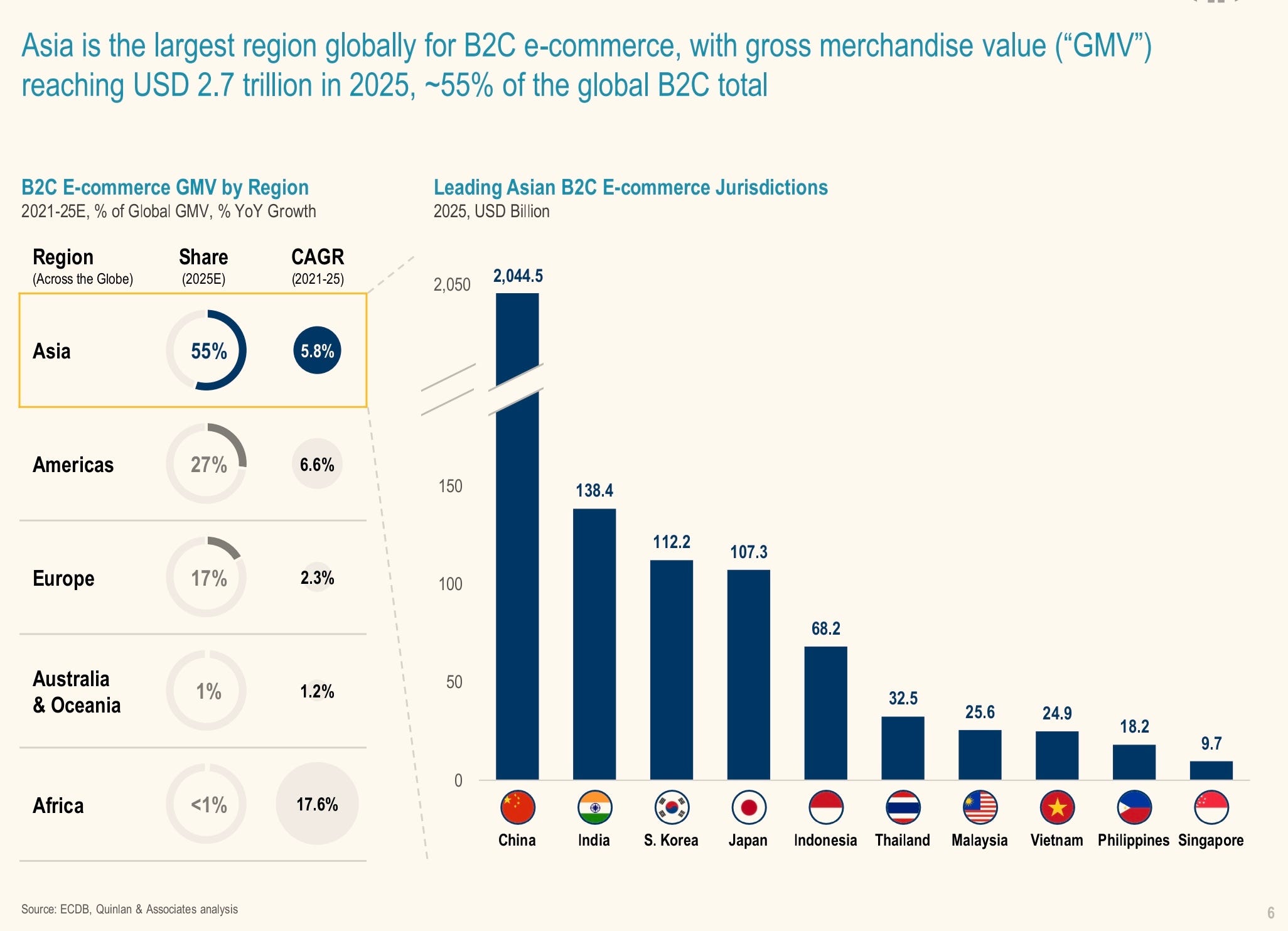

E-commerce has fundamentally changed the way both consumers and businesses shop, with global B2B and B2C e-commerce Gross Merchandise Value (“GMV”) reaching a staggering USD 13.2 trillion in 2025. Capitalising on numerous structural growth tailwinds, the industry has seen the rise of a plethora of third-party e-commerce merchants, numbering over 31 million in 2025 and accounting for the lion’s share of global e-commerce GMV, with an especially outsized GMV contribution in Asia.

Key takeaways:

· E-commerce has fundamentally changed the way both consumers and businesses shop, with global B2B and B2C e-commerce GMV reaching a staggering USD 13.2tn in 2025

· The industry has seen the rise of a plethora of third-party e-commerce merchants, numbering over 31m in 2025 and accounting for the lion’s share of global e-commerce GMV, with an especially outsized GMV contribution in Asia

· Compared to traditional retail, e-commerce platforms generate rich, standardised, and contextualised data by capturing both fund flows and fulfilment, materially enhancing underwriting potential. While this should, in principle, improve access to credit for e-commerce sellers, most banks remain structurally disconnected from the e-commerce ecosystem and lack access to real-time financial and operational data.

· This separation limits visibility into merchant performance and creates several key challenges, including (1) inaccurate credit profiling, (2) incompatible product offerings, and (3) an inability to control platform funds. Coupled with persistent operational frictions and prohibitive onboarding costs, most banks, especially in Asia, have remained on the sidelines, resulting in an estimated APAC e-commerce credit gap of USD 1.2tn in 2025

· Various FinTech lenders have emerged over the past decade to address the MSME e-commerce lending whitespace left by incumbent banks. While a growing number of incumbent banks are providing warehouse financing facilities to these FinTechs, this indirect participation model has seen them surrender ~USD 100bn in annual revenue potential to frenemies. And in the process of funding their digital-native challengers, they have given up owning the client relationship

Keep reading with a 7-day free trial

Subscribe to Fintech Wrap Up to keep reading this post and get 7 days of free access to the full post archives.