Reports: Blockchain for banks; 2026 Global AI in Financial Services Report; The new stack for global finance: Stablecoins edition

This week’s fintech reports highlight a major shift in global financial infrastructure driven by stablecoins, AI, blockchain, and vertically integrated fintech models. The core theme across the reports is that finance is moving toward programmable, real-time systems where payments, treasury, lending, and settlement increasingly converge into unified infrastructure layers. Stablecoins are evolving from crypto tools into foundational financial rails, while blockchain is being adopted as a settlement and reconciliation upgrade for banks rather than a speculative technology. At the same time, AI adoption across financial services is accelerating globally, with both institutions and regulators embedding AI into operations and governance. Emerging markets across Africa and MENA continue expanding rapidly beyond payments into lending, SME finance, and digital infrastructure, while companies like Ant International demonstrate how integrated fintech ecosystems combining payments, wallets, treasury, and embedded finance are shaping the future of global commerce.

Video of the Week

Deep Dive of the Week

Ant International’s Multi-Product Commerce Infrastructure

In recent years, Ant International has evolved into a unified techfin platform powering global commerce. Its core stack combines cross-border payments (Alipay+ and Antom), digital wallets, global account services (WorldFirst), embedded finance (Bettr), plus an AI-driven layer for compliance and fintech services. As a result, the company now connects 2 billion consumer accounts to over 150 million merchants worldwide through Alipay+, processes 20+ million transactions daily, and spans 300+ payment methods across 220+ markets. WorldFirst and Bettr provide global account services to 1.6 mn SMEs, and over 30 mn underserved businesses and individuals access credit. This article breaks down the technology and product strategy behind Ant International’s platform convergence.

The platform supports 300+ payment methods, all major card schemes, 50+ wallet and bank apps, 10+ national QR systems in 220+ markets. This means consumers can use preferred local payment options, for example, SGQR, DuitNow, PromptPay, QRIS, etc., while merchants connect through one integration.

Antom’s merchant gateway serves businesses in 50+ countries, enabling them to accept payments in 100+ currencies and reach customers in over 200 markets. Its services go beyond payments to include digital marketing and store digitization. WorldFirst’s global account and treasury services provide one-stop cross-border accounts, payments, FX conversion, and even supply-chain financing. In combination, WorldFirst and Bettr serve 1.6+ million small businesses and provide credit access to 30+ million underserved MSMEs and consumers.

Together, these products form a converged infrastructure layer: all facets of commerce transactions, payment acceptance, wallets, corporate accounts, and lending are integrated via APIs and common services. For example, Alipay+ links global bank apps and e-wallets to merchants via SWIFT rails and ISO 20022 messaging. Antom supports card and alternative payments through an enterprise-grade gateway, including APM checkout and digital wallets. Bettr provides embedded finance APIs to accelerate merchant growth, and WorldFirst offers treasury APIs such as a multi-currency account and fund management for cross-border trade. All services share identity, risk, and funds movement flows on Ant’s unified stack.

This week’s reports

1️⃣The BaaS Wreckage and Regulatory Thaw That Cleared the Way for Nubank’s US Entry

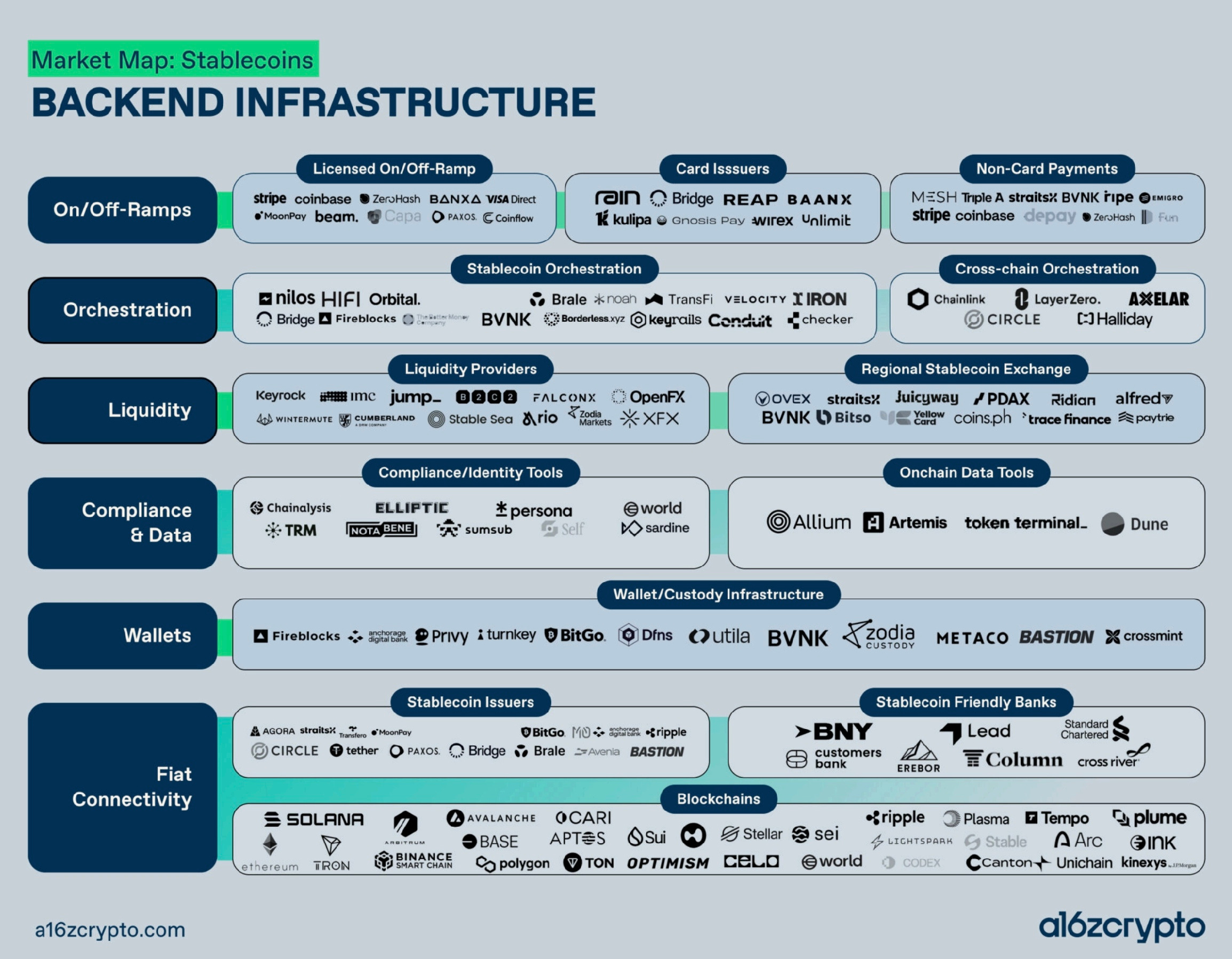

2️⃣The new stack for global finance: Stablecoins edition

3️⃣The global expansion of stablecoins

4️⃣2026 Global AI in Financial Services Report

5️⃣Blockchain for banks

6️⃣Unlocking Africa’s Second FinTech Wave

7️⃣The next phase of MENA fintech growth

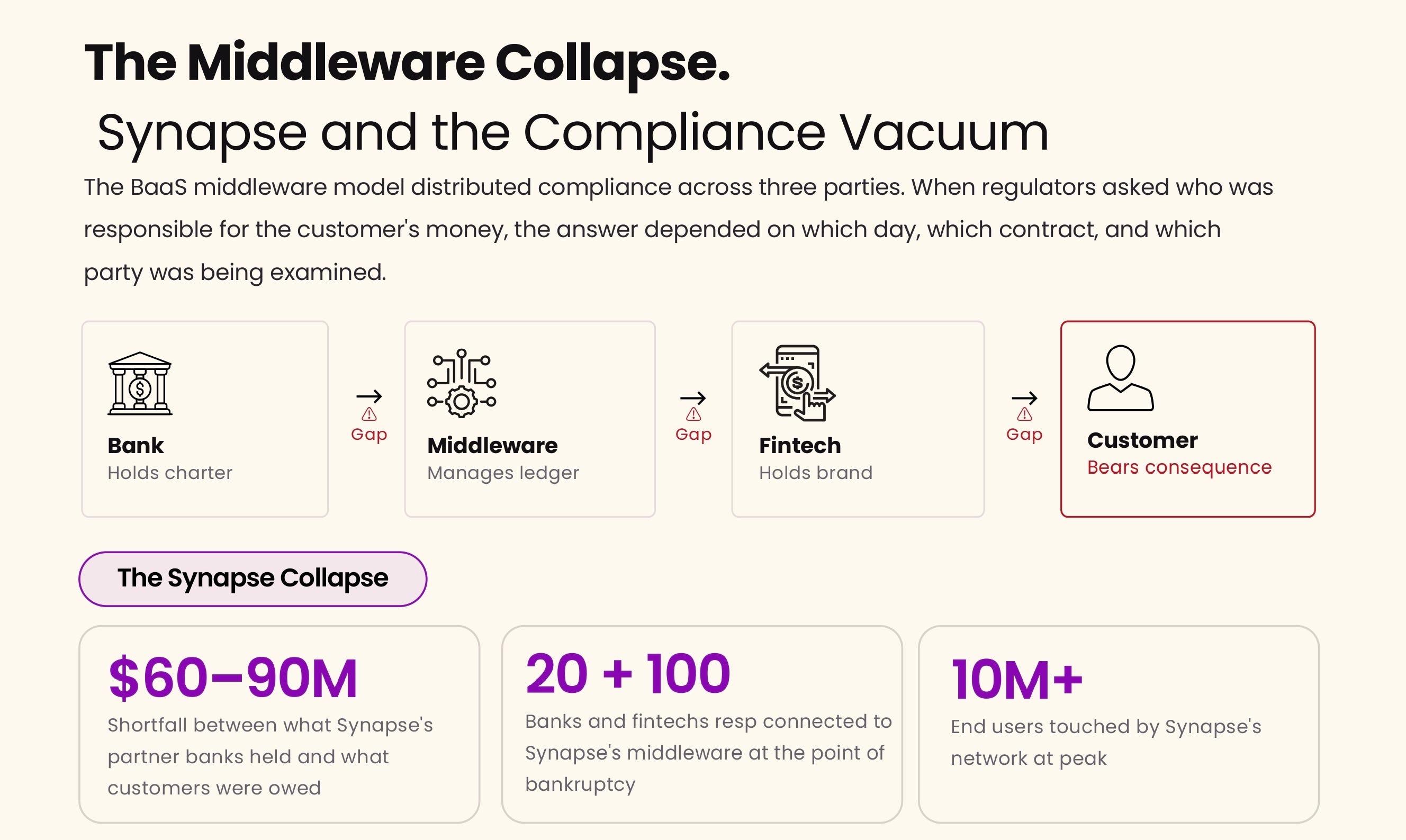

The BaaS Wreckage and Regulatory Thaw That Cleared the Way for Nubank’s US Entry

The most important idea in this report is not Nubank’s entry. It is that failure removed optionality.

The BaaS model did not evolve. It collapsed under its own structure. Compliance was fragmented, ownership was unclear, and when stress hit, no single entity could answer for the system. The Synapse failure exposed this directly: money, ledger, and responsibility were split across parties that could not reconcile reality when it mattered .

That is not a product failure. That is a design failure.

What followed was predictable. Regulators did not just tighten rules. They forced a reversion to clear ownership. The system moved from distributed responsibility back to vertically integrated accountability.

At the same time, the co-branded model failed for a different reason. Economics, not compliance. Banks funded risk they did not control, while fintechs controlled distribution without holding balance sheet consequences. The result was mispriced risk and sustained losses. When the assumptions broke, the partnerships unwound.

Two different models. Same outcome. Misalignment between control and responsibility.

The key shift is what survived.

The licensed digital bank model did not win because it is more innovative. It won because it is structurally coherent. One entity holds the charter, the balance sheet, the compliance, and the customer. That alignment is what regulators can supervise and what markets can price.

Everything else was filtered out.

The report frames this as a “regulatory thaw,” but the more accurate framing is a reset. The system cleared unstable abstractions before allowing new entrants. Nubank did not just arrive at the right time. It avoided every failure mode before the reset happened .

That is the real advantage.

Keep reading with a 7-day free trial

Subscribe to Fintech Wrap Up to keep reading this post and get 7 days of free access to the full post archives.