Open finance and the future of the payments industry; Cross-border payments: Money transmitters vs Payment aggregation; Breaking it down: key pain points in client onboarding;

Welcome to this week's Fintech Wrap Up, where we'll explore the power of open finance, delve into the rise of embedded finance ecosystems, and uncover innovations in cross-border payments

Insights & Reports:

1️⃣ Open finance and the future of the payments industry

2️⃣ Relationships between different Embedded Finance stakeholders

3️⃣ Breaking it down: key pain points in client onboarding

4️⃣ Interoperability Scenarios for Fast Payment Systems and CBDC Systems

5️⃣ Cross-border payments: Money transmitters vs Payment aggregation

6️⃣ How are banks investing in cross-border payments?

7️⃣ Fintech Plaid’s Product Stack

8️⃣ The landscape of financial services super-apps

9️⃣ Revolut Co-Founder Nik Storonsky Hints at US Banking License Application

TL;DR:

The latest edition of Fintech Wrap Up is here, let’s dive in!

The payments industry is undergoing a massive shift, with open finance poised to reshape how we transact. Building on the success of open banking, open finance is fueling innovations like account-to-account (A2A) payments and digital wallets, which continue to dominate the e-commerce landscape. A2A payments are gaining traction thanks to standardized APIs and seamless integrations, while digital wallets are projected to grow at an impressive 15% CAGR through 2027. With open APIs simplifying wallet top-ups and enhancing security, it’s no surprise they’re winning over consumers and businesses alike. Meanwhile, BNPL services are becoming smarter and more personalized, leveraging open data to improve credit assessments and offer a more tailored experience.

Embedded finance is another game-changer, with embedders, providers, and enablers collaborating to integrate financial services directly into everyday platforms like e-commerce sites, apps, and even social media. Whether it’s BNPL on a retail site or savings accounts embedded into an app, the goal is a seamless experience that brings value to users without added complexity. This ecosystem is redefining how financial products reach consumers, making them more accessible and integrated into our daily lives.

Client onboarding is still a challenge, especially for corporates. The process can take up to 120 days, with manual bottlenecks, fragmented workflows, and complex risk assessments slowing things down. By contrast, individual onboarding is increasingly automated, highlighting the potential for technology to transform corporate onboarding too. With automation and streamlined processes, banks and fintechs can drastically reduce onboarding times and costs.

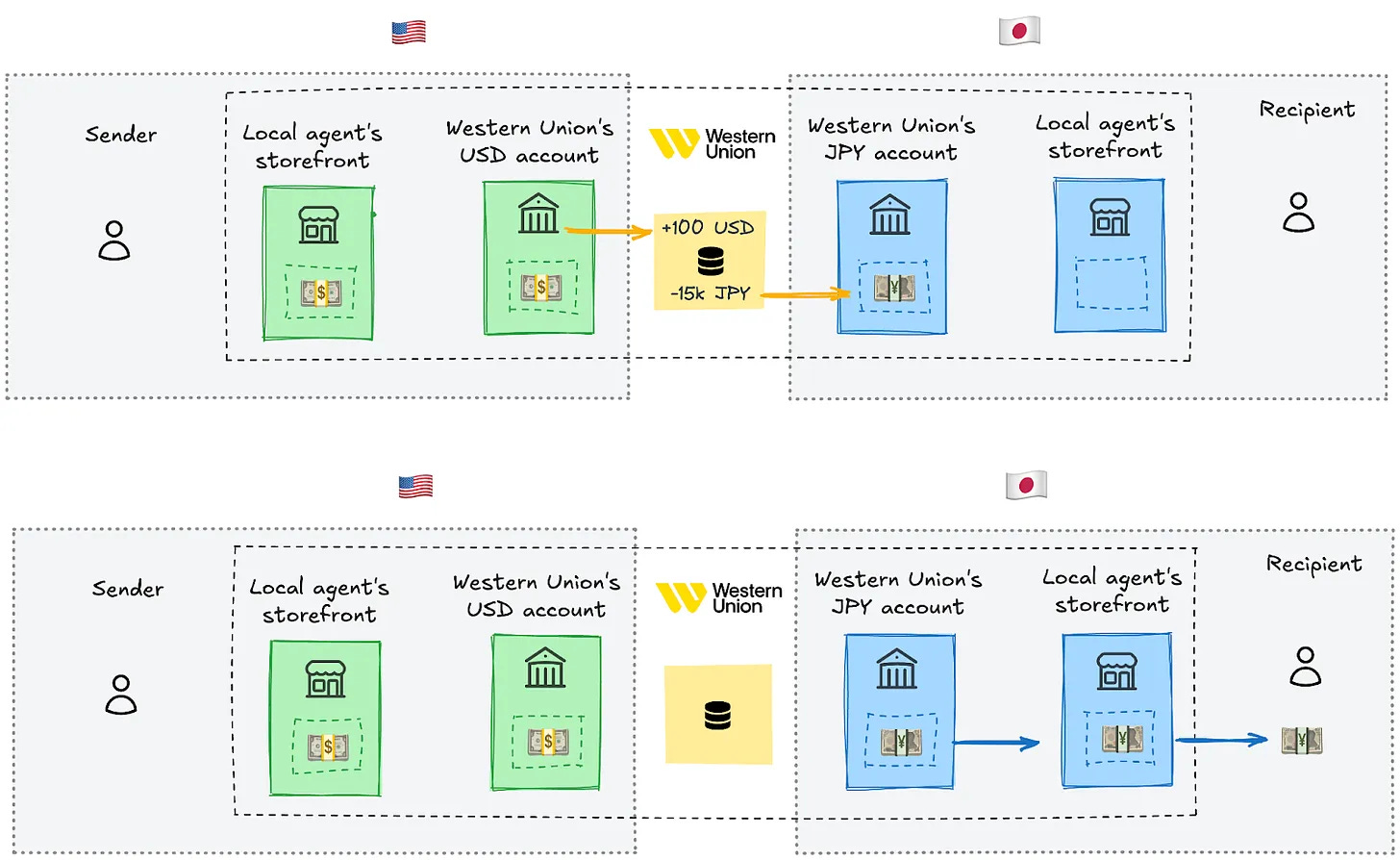

On the cross-border payments front, money transmitters like Western Union continue to provide accessibility for the unbanked, but newer players like Wise are disrupting the space with faster, more affordable digital solutions. By reducing intermediaries and leveraging local accounts, these aggregators are setting a new standard for speed and efficiency. Banks are also investing heavily in this space, with Citi leading in cross-border payments investments and blockchain innovators like Fnality and Form3 attracting major backing.

The rise of financial super-apps is another big story, blending banking, payments, lending, and investments into a single platform. Apps like Revolut and WeChat are making it easier than ever to manage money, track expenses, and make payments, all in one place. Features like QR code payments and budgeting tools are driving their popularity and setting a high bar for user convenience.

Insights

Open finance and the future of the payments industry

Open finance to bolster the payments sector similar to open banking

The payments industry is poised for significant transformation under open finance, which will entail substantial revenue increases. However, the industry is also facing intense competition from a broader range of financial industry players, including FinTech startups, traditional banks, card networks, and super apps. This heightened competition will drive consolidation in payment usage, with customer preferences playing a critical role in shaping market dynamics. To thrive amidst this competitiveness, institutions must focus on meeting and anticipating customer needs and making seamless and integrated payment experiences essential. As the industry evolves, select payment solutions are also gaining traction by aligning closely with these changing customer expectations. This alignment not only reinforces their importance but also highlights the promising growth projected for these solutions.

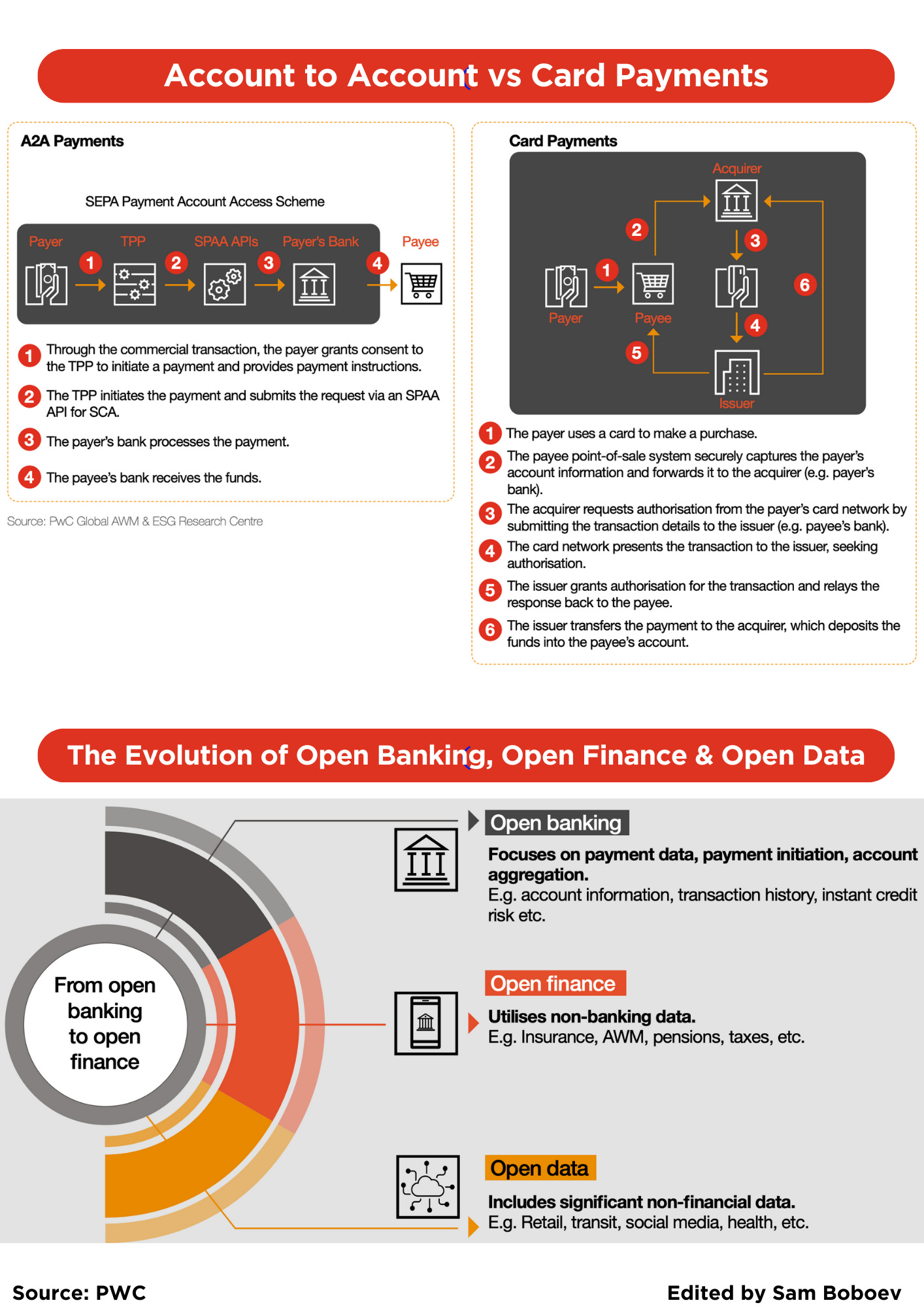

Account-to-account payments (A2A) to gain popularity

Despite their existence prior to open banking, A2A payments gained mainstream traction with the advent of regulated third- party financial service providers. Regulatory developments such as the SEPA Payment Account Access scheme invite any EU bank or regulated FinTech to offer A2A payments and data services via APIs, benefiting merchants and consumers alike.

Open finance data sharing will further expand A2A models, enabling common APIs for payments between service providers and fostering an interconnected ecosystem of instant payment apps. Strong customer authentication measures and standardised APIs will facilitate seamless payments across

platforms.

Mobile and digital wallets to extend their growth through open APIs

Digital wallets-inclusive of pass-through wallets, stored value wallets, and mobile money wallets- continue to dominate the global e-commerce landscape, accounting for 50% of total transaction value in 2023.11 As the fastest-growing payment method in e-commerce, digital wallets are projected to grow at a CAGR of 15% through 2027.12 The integration of open finance functionality into digital wallets allows users to top up their wallets with just a few clicks, without incurring additional costs. This combination of convenience and security is driving their popularity among consumers and businesses alike

BNPL solutions will become more personalised

Keep reading with a 7-day free trial

Subscribe to Fintech Wrap Up to keep reading this post and get 7 days of free access to the full post archives.