Open Banking on AWS; Metrics for banks to measure engineering team performance; The paths to multi-product for payment companies;

This week, we're exploring the rise of open banking on AWS, the transformation of cross-border payments with real-time integration, and the evolving demands of risk and compliance in fintech

Insights & Reports:

1️⃣ Open Banking on AWS

2️⃣ Emerging alternative models poised to revolutionize cross-border payments

3️⃣ Risk and Compliance Model for Payments

4️⃣ Fintech 100: The most promising fintech startups of 2024

5️⃣ The paths to multi-product for payment companies

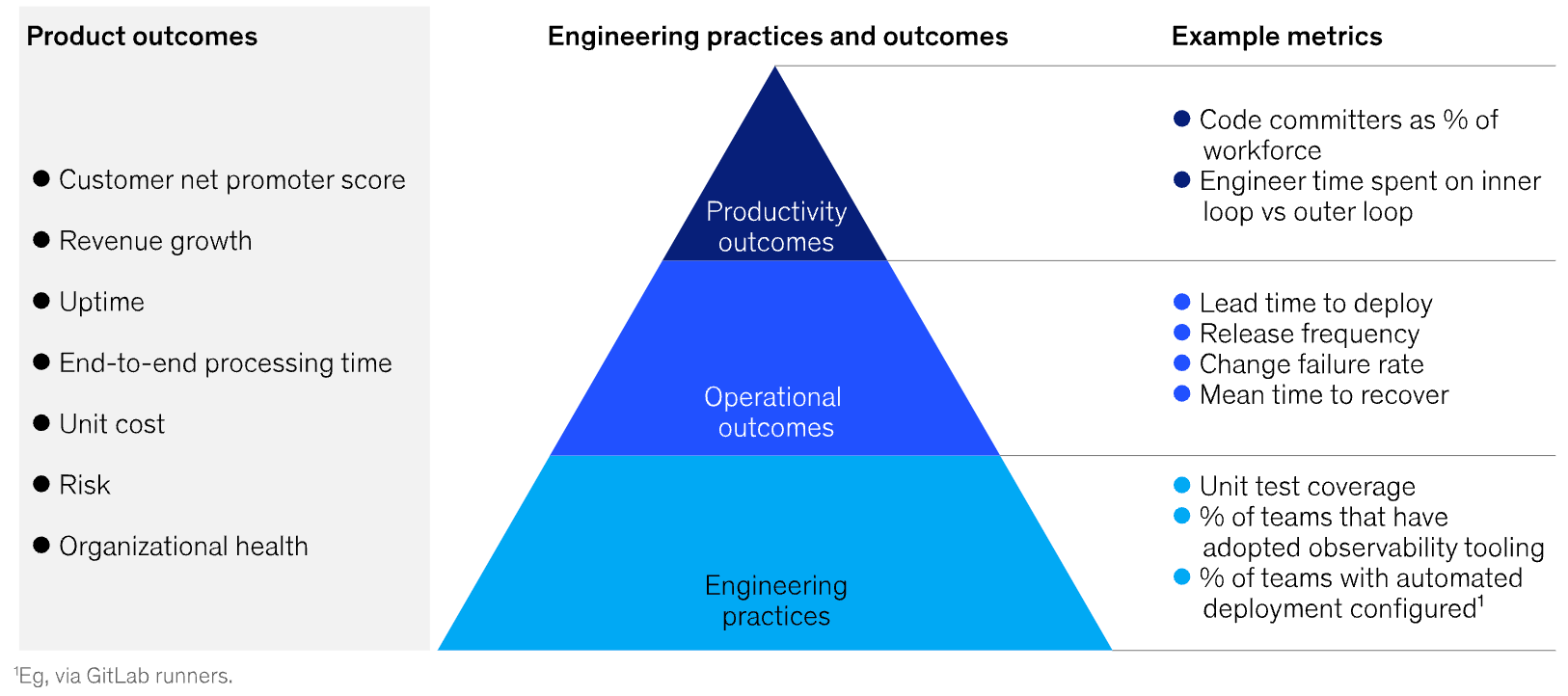

6️⃣ Metrics for banks to measure engineering team performance

7️⃣ Designing payment workflows for industry-specific needs

8️⃣ Cross-Border Payments 24x7: How Can Banks Be Future Ready?

9️⃣ Affirm beats on top and bottom lines

TL;DR:

This week’s edition brings you fresh insights into some of the most dynamic trends shaping fintech and payments. First up, open banking continues to evolve, with AWS becoming the go-to platform for banks to build secure, scalable API frameworks that power new revenue streams and innovative models like Banking-as-a-Service and embedded finance. With customer consent, data can now be shared almost instantly, enabling banks to monetize their ecosystems with minimal friction.

Cross-border payments are ripe for disruption, with fintechs and non-bank alternatives stepping up to streamline processes bogged down by traditional banking networks. New tech-enabled models are reducing fees, boosting transparency, and speeding up transfers—initiatives like BIS’s Project Nexus and ASEAN’s Cross-Border Payments Interoperability Network are setting the stage for global real-time payments integration, signaling a new era for international transactions.

On the risk and compliance front, payments companies are being urged to adopt a more expansive approach to risk, engaging boards in regular reviews and making substantial investments in risk management functions. This shift isn’t just about regulatory boxes; it’s about operational resilience and agility in a fast-evolving landscape.

Our Fintech 100 feature showcases this year’s top startups, with impressive funding figures and emerging tech in wealth management, embedded finance, and insurance. Despite a challenging market, nearly half of these companies are early-stage, pointing to strong innovation potential globally, with new leaders in payments, capital markets, and alternative lending making waves.

Lastly, we explore the complexities of going multi-product, highlighting why only a few companies manage to extend beyond their core offering due to the demands on resources and company focus. We also delve into how banks are measuring engineering productivity, using data-driven insights to enhance speed, efficiency, and output, yielding customer-centric innovations faster.

In curated news, UBS’s blockchain pilot for domestic and cross-border transactions is promising, Affirm exceeded expectations in its GMV report, and Brazil’s PicPay is revolutionizing instant payments through partnerships with Meta and Microsoft.

Let’s keep our pulse on the fintech revolution and make sense of these powerful shifts together!

Insights

Open Banking on AWS

In open banking, banks use an API messaging framework to securely share their customer data (with consent from customers) to third-party developers and service providers, which allows for automated and secure access to the data in their core banking environment. While open banking initially started as a regulatory requirement in the United Kingdom (UK) and other regions around the world, it has now transformed into a new revenue stream for banks, as they look to monetize their data and core functionality by exposing their core environment through APIs and building new business models such as Banking as a Service (BaaS) and embedded finance on top of the APIs. Banks often choose AWS to build their open banking environment because of its inherent scalability, cost effectiveness, and the speed at which they can build. Open banking architectures supporting these use cases share the following characteristics:

🔹 Data is shared to third parties only after consent from the customer using OAuth 2.0.

🔹 Secure and limited third party access (with mutual Transport Layer Security (mTLS)).

🔹 API-driven infrastructure and an elastic and scalable environment.

🔹 Instant or near-instant access to customer account data.

Keep reading with a 7-day free trial

Subscribe to Fintech Wrap Up to keep reading this post and get 7 days of free access to the full post archives.