How does dynamic currency conversion work?; Can stablecoins bridge the Traditional and New Monetary Systems?; Adyen’s Approach to Augmented Unit Test Generation with LLMs

Welcome to the latest edition of Fintech Wrap Up, where we decode the pulse of modern financial innovation.

Daily news on Payments Wrap Up

This week’s reports

Dynamic currency conversion vs. tradition currency conversion

1️⃣ Generative AI in Financial Services: From Hype to Real-World Impact

2️⃣ Stablecoins: Turning Money Into Programmable Infrastructure

3️⃣ Stabelcoin regulations: Where we are today, and what challenges lie ahead

4️⃣ How does dynamic currency conversion work?

5️⃣ AI: The Missing Piece In Small-Business Banking

6️⃣ Stabelcoin Summer: Hype, Regulation, and What Comes Next

This week’s insights

1️⃣What Changes Could Stripe L1 Blockchain Bring?

2️⃣The Rise of Alternative Payment Methods (APMs)

3️⃣Adyen’s Approach to Augmented Unit Test Generation with LLMs

4️⃣Can Digital Identification Enable Seamless, Secure and Borderless Digital Services and Payments?

5️⃣Can stablecoins bridge the Traditional and New Monetary Systems?

6️⃣How does dynamic currency conversion work?

7️⃣How will digital wallet interaction happen in the agentic AI flow?

The Great Stablecoin Chain Grab: Circle’s Arc vs. Stripe’s Rumored “Tempo”

Imagine sipping coffee with a fellow fintech nerd when they drop this bombshell, “Did you hear Stripe and Circle are both building their own Layer-1 blockchains?” It sounds crazy, but it’s true. In the past few months, payments giant Stripe (yes, that Stripe) and stablecoin issuer Circle have each unveiled plans for custom L1 blockchains – Stripe’s project reportedly called “Tempo” and Circle’s chain known as “Arc.” This is like Visa and PayPal each deciding to build their own version of Ethereum. What’s going on here, and why now? Let’s break it down.

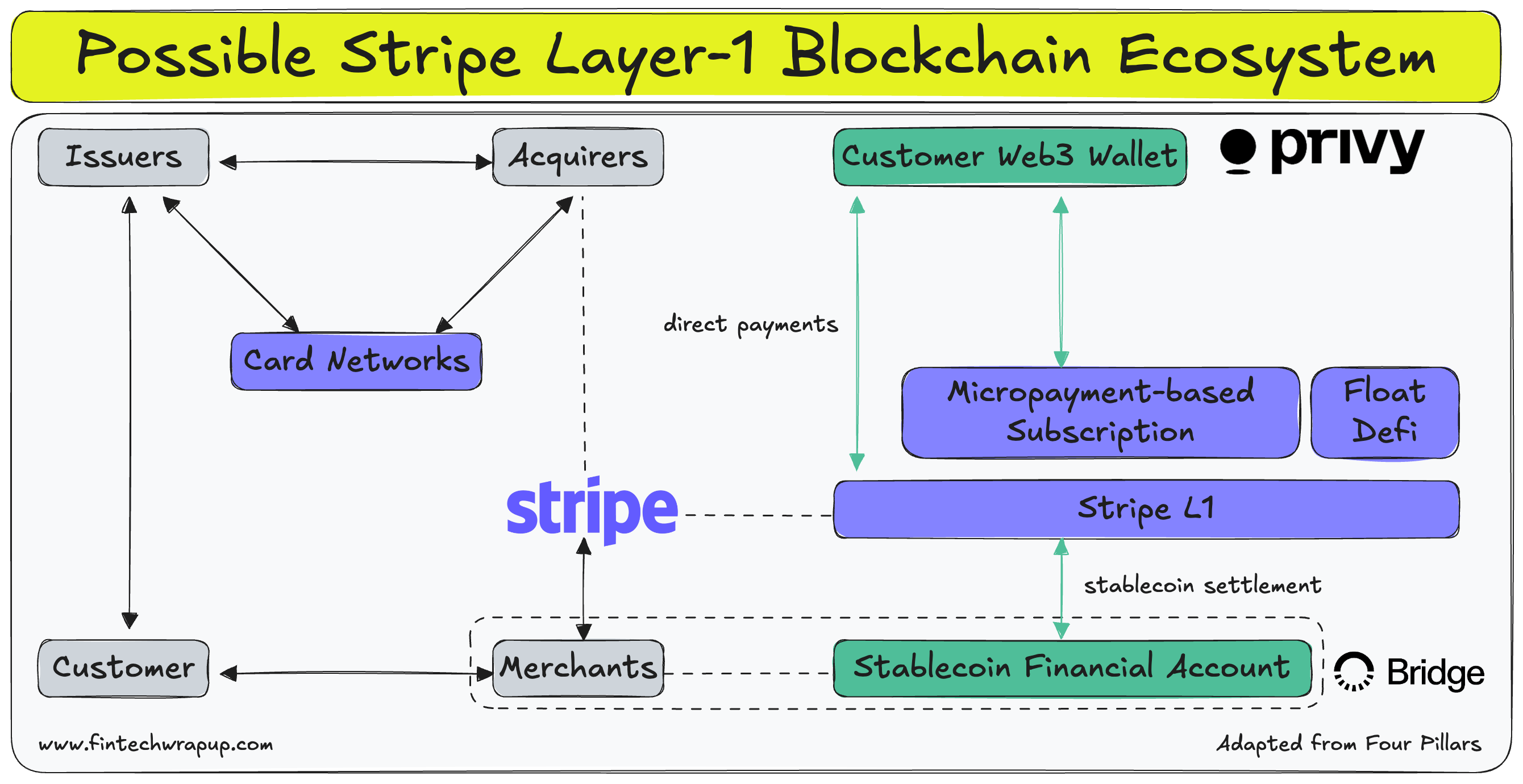

What Changes Could Stripe L1 Blockchain Bring?

If Stripe does launch an L1, how could it improve existing services, and what new ones might it enable?

👉 Base Case

🔹 Integration of Merchant Stablecoin Accounts with Stripe L1

Stripe offers stablecoin financial accounts to merchants in 101 countries, letting them hold USDC/USDB and move funds via ACH, SEPA, and multiple blockchains. If Stripe L1 launches, deposits and withdrawals could also flow through it, with merchants using balances for on-chain financial activities.

🔹 Stablecoin Settlement for Merchants

Stripe, as a PSP or acquirer, settles merchant proceeds. With Stripe L1, merchants may choose settlement in dollar-based stablecoins—a major benefit for those with high dollar demand but limited access.

🔹 Wallet Services for Customers

Stripe acquired Privy, a wallet infrastructure provider. While Stripe has focused on merchants, Stripe L1 could let individuals create wallets, use stablecoins for payments, and participate in financial activity within its ecosystem.

🔹 Stablecoin Payment Option for Customers

Currently, Stripe users pay mainly via cards and banks. Stripe L1 could allow linking Web3 wallets (Stripe’s or third parties) and paying with stablecoins.

👉 Bull Case

🔹 Direct Payments Between Customers and Merchants

Traditional payments rely on card networks and banks. Stripe L1 could enable direct stablecoin payments, eliminating intermediaries, lowering fees, and speeding settlement. Since blockchain payments are harder to reverse, safeguards for cancellations and refunds would be required.

🔹 Micro-Payment Subscription Services

Blockchains support micro-payments and streaming-based billing, unlike monthly renewals common today. Stripe L1 could power subscriptions billed by the minute, with smart contracts automating payments. This could unlock entirely new service models.

🔹 DeFi Utilization of Short-Term Deposits

In current systems, settlement is delayed to manage fraud or refunds. Even with Stripe L1, funds may be held temporarily. These deposits—likely large in scale—could be deployed as liquidity in DeFi protocols, lending markets, or bonds, boosting capital efficiency and generating returns.

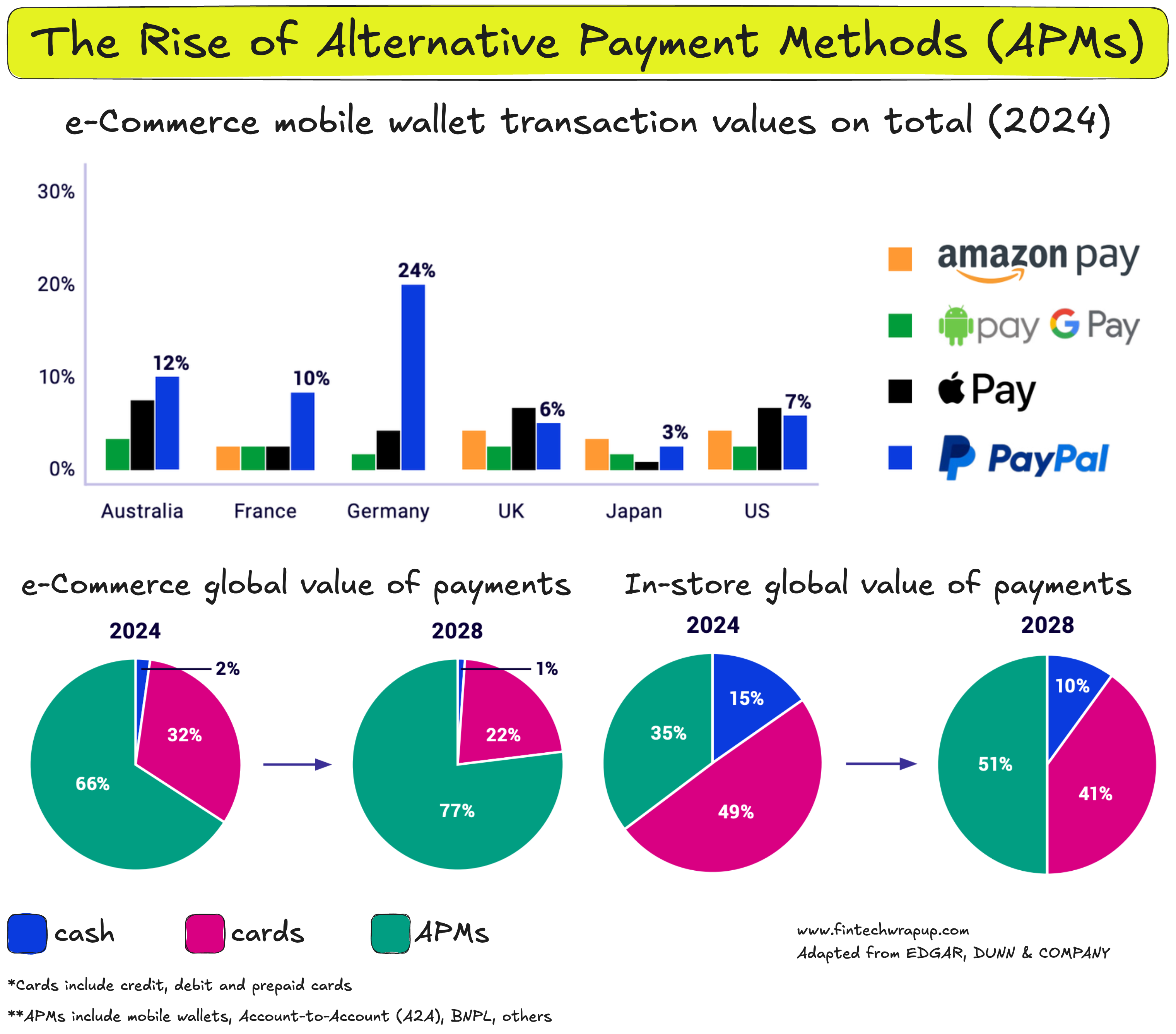

The Rise of Alternative Payment Methods (APMs)

APMs are dominating global e-commerce transactions

APMs refer to any means of making a payment other than cash or credit/debit/prepaid cards from major card networks.

They include:

- Mobile wallets

- Buy Now, Pay Later (BNPL)

- Bank-to-bank transfers

- Cash-based payments (e.g., Boleto in Brazil)

- Cryptocurrencies

The main benefits of APMs are convenience, higher conversion rates, transaction speed, and enhanced security.

APMs have been gaining popularity worldwide and are expected to continue growing, reducing the share of payment cards in both transaction volumes and values. They already hold a dominant position in the global e-commerce landscape and are projected to reach 77% of global transaction value by 2028.

APM usage trends vary significantly across markets

APM adoption differs across regions and countries.

- Regions with advanced digital infrastructure—such as Asia-Pacific, North America, and Europe—have already seen a significant shift toward digital payments.

- Asia-Pacific leads with the highest APM penetration, largely driven by mobile wallets, which accounted for 70% of global mobile wallet transaction value in 2023.

- In contrast, other regions may take longer to transition due to technological limitations or cultural preferences.

APMs will not completely replace physical cards

While APMs are becoming the preferred payment method for many consumers, especially digital wallets, they are not expected to fully replace physical cards or traditional methods. Instead, they indicate a shift from card-centric models to digital-first solutions.

Digital wallets are also expanding beyond payments into services such as:

- Loyalty programs

- Customer satisfaction surveys

- Authentication

Factors contributing to high growth of APMs

Benefits for consumers and businesses

- Secure transaction environment (e.g., biometric identification)

- Reduced online payment friction (no need to re-enter payment details for every purchase)

- Increased revenue through higher conversion rates

- Improved cash flow via faster and more efficient transactions

Advancements in technology

- Proliferation of smartphones and internet connectivity has accelerated adoption.

- Consumers are embracing mobile technology and streamlined payment experiences, driving APM growth.

Factors slowing APM adoption

Cultural and demographic factors

- Preference for traditional methods such as cash and cards.

- Lack of trust in new methods or insufficient education about them.

Remaining technological barriers

- Limited access to smartphones and internet connectivity in some regions.

- For businesses, integrating multiple APMs can be costly and complex.

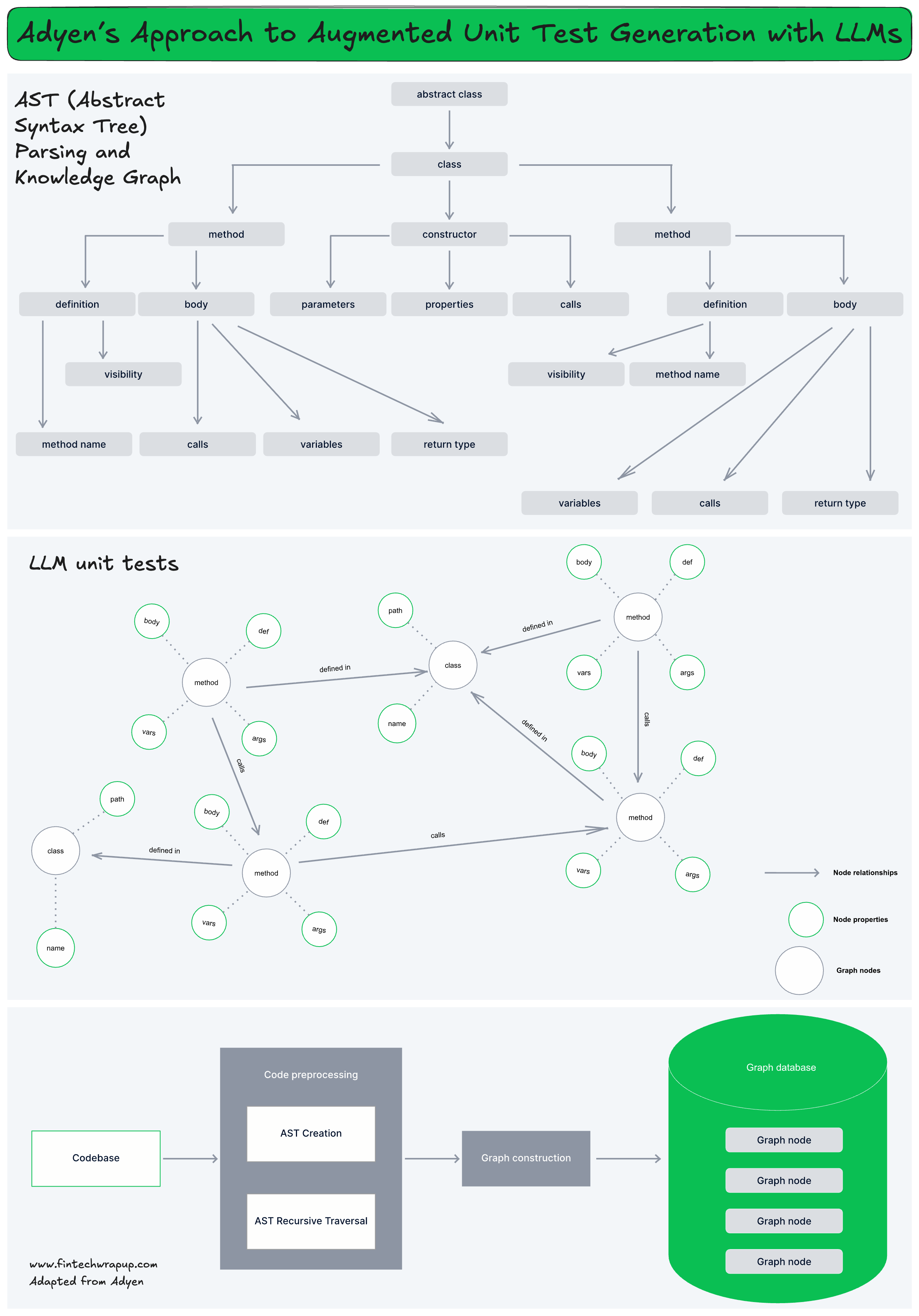

Adyen’s Approach to Augmented Unit Test Generation with LLMs

At Adyen, code quality is non-negotiable. As their systems grew in complexity, ensuring consistency and reliability in unit testing became both more important and more resource-intensive. This sparked a question: can Large Language Models (LLMs) do more than generate boilerplate code? Could they augment the creation of high-quality unit tests?

The answer led them to a unique approach that goes beyond traditional text-driven AI.

👉 The Problem with Conventional LLM Use in Code

LLMs like GitHub Copilot are great at writing small functions or snippets. But in real-world engineering, code lives inside large, interconnected frameworks. Writing meaningful unit tests requires more than recognizing patterns; it demands understanding dependencies, state management, and how methods interact within the wider codebase.

Traditional Retrieval-Augmented Generation (RAG) helps provide context, while fine-tuning sharpens accuracy. Yet both approaches hit limits in code: embeddings miss subtle semantics, and fine-tuning is resource-heavy for fast-moving repositories. Code isn’t just text—it’s architecture.

✅ Adyen’s Breakthrough: ASTs and Knowledge Graphs

To bridge this gap, Adyen moved beyond plain embeddings to structural and semantic representations of code.

🔹 Abstract Syntax Trees (ASTs)

ASTs break source code into a hierarchical tree. Each node represents constructs like variables, methods, or conditions. This allows them to see the scope of variables, sequence of function calls, and control flow—things that raw text can’t capture.

ASTs give the LLM a map of the code’s skeleton, ensuring it doesn’t just guess but understands logic and architecture.

🔹 Knowledge Graphs (KGs)

They extend ASTs by constructing Knowledge Graphs. Here, entities (functions, classes, objects) are nodes, and relationships (inheritance, dependencies, interactions) form edges. Unlike embeddings, which rely on semantic similarity, KGs reveal actual connections across the codebase.

This lets the system answer questions like: Which methods depend on this variable? How does this class interact with others?—insights critical for generating unit tests that reflect real functionality.

👉 The Workflow

🔹 Parse the codebase into ASTs → expose syntax and structure.

🔹 Build Knowledge Graphs → enrich ASTs with semantic links.

🔹 Store graphs in a database → enabling precise, context-aware queries.

🔹 Feed relevant context to the LLM → not just snippets, but full structural understanding.

🔹 Generate unit tests → consistent, logically sound, and aligned with Adyen’s standards.

👉 Why It Works

This hybrid approach solves the two biggest hurdles:

🔹 Context sensitivity → ASTs and KGs together capture dependencies, 🔹 hierarchies, and hidden flows.

🔹 Consistency → the system reduces variability in test quality by giving LLMs the right context every time.

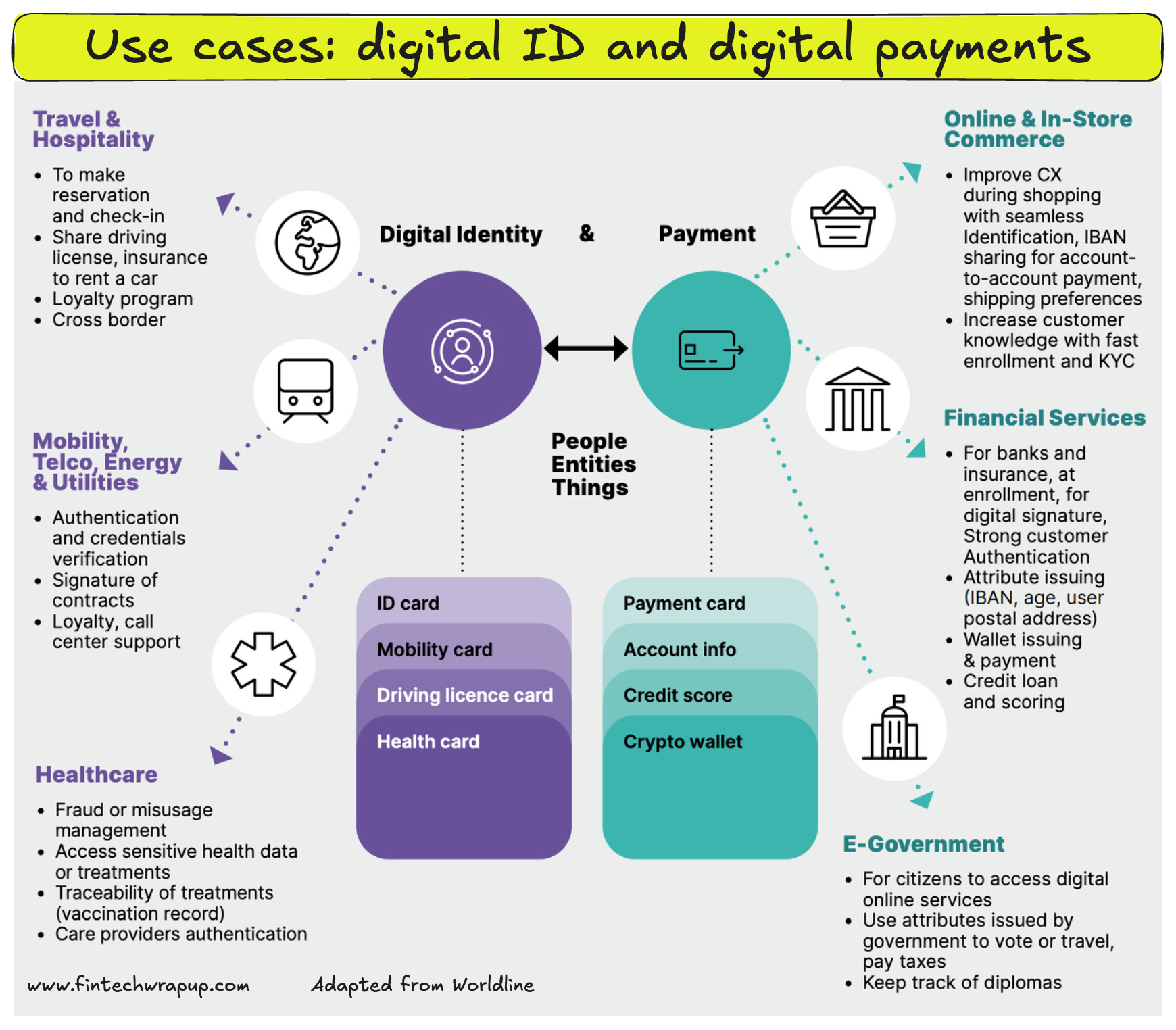

Can Digital Identification Enable Seamless, Secure and Borderless Digital Services and Payments?

The rapid evolution of the global digital society is unstoppable. With it comes a tremendous demand for secure digital identification—a foundation that touches every sector, from banking and healthcare to retail and mobility. The challenge is balancing two opposing forces: offering a frictionless user experience that boosts conversion rates, while maintaining robust security to fight fraud.

Today, identity still takes many forms: paper, plastic, QR codes, and increasingly, biometrics. But the question is—what comes next? Will digital identification unlock standardisation, cross-border acceptance, and universal adoption? And more importantly, are we ready for it—whether as consumers, businesses, or regulators?

🔹 Standardisation of Identity

Several countries have already launched national digital ID programs. The European Union is leading the charge with eIDAS 2.0, a regulation that will grant every EU citizen access to a digital identity wallet under their control. This wallet will store trusted attributes such as a driver’s licence, age, or diploma, usable across both public and private services. Acceptance by service providers will be mandatory, creating a harmonised framework across all Member States.

Other major economies, from the U.S. to India and Brazil, are advancing similar programs. The World Bank’s ID4D initiative and the UN’s work on digital ID also show that the move toward global standards is accelerating.

🔹 Future Development

Technology will play a pivotal role. Biometrics, wearables, and self-sovereign identity models (SSI) are set to make digital ID both more secure and user-centric. Web3 frameworks may even allow individuals to reclaim control of their credentials, reducing reliance on third parties.

But digital ID won’t just be about people. Objects, companies, and even vehicles will have digital identities to access services autonomously. For example, a car could authenticate its driver and initiate payments for tolls or charging without human intervention.

🔹 Overcoming Privacy and Trust Barriers

Privacy concerns remain a major barrier. Fears of data cloning, misuse, or surveillance could slow adoption. Regulation will therefore be essential—not just for security, but to build trust. eIDAS in Europe, Aadhaar in India, and the UK’s Digital Identity Trust Framework are early examples of frameworks tackling these concerns.

🔹 Real-World Benefits

The use cases are compelling. Age-restricted purchases alone demonstrate the value: UK retailers spend an estimated £4 billion annually on manual age checks, much of it through customer service interventions. A secure digital identity could automate these processes, reducing costs while improving customer experience.

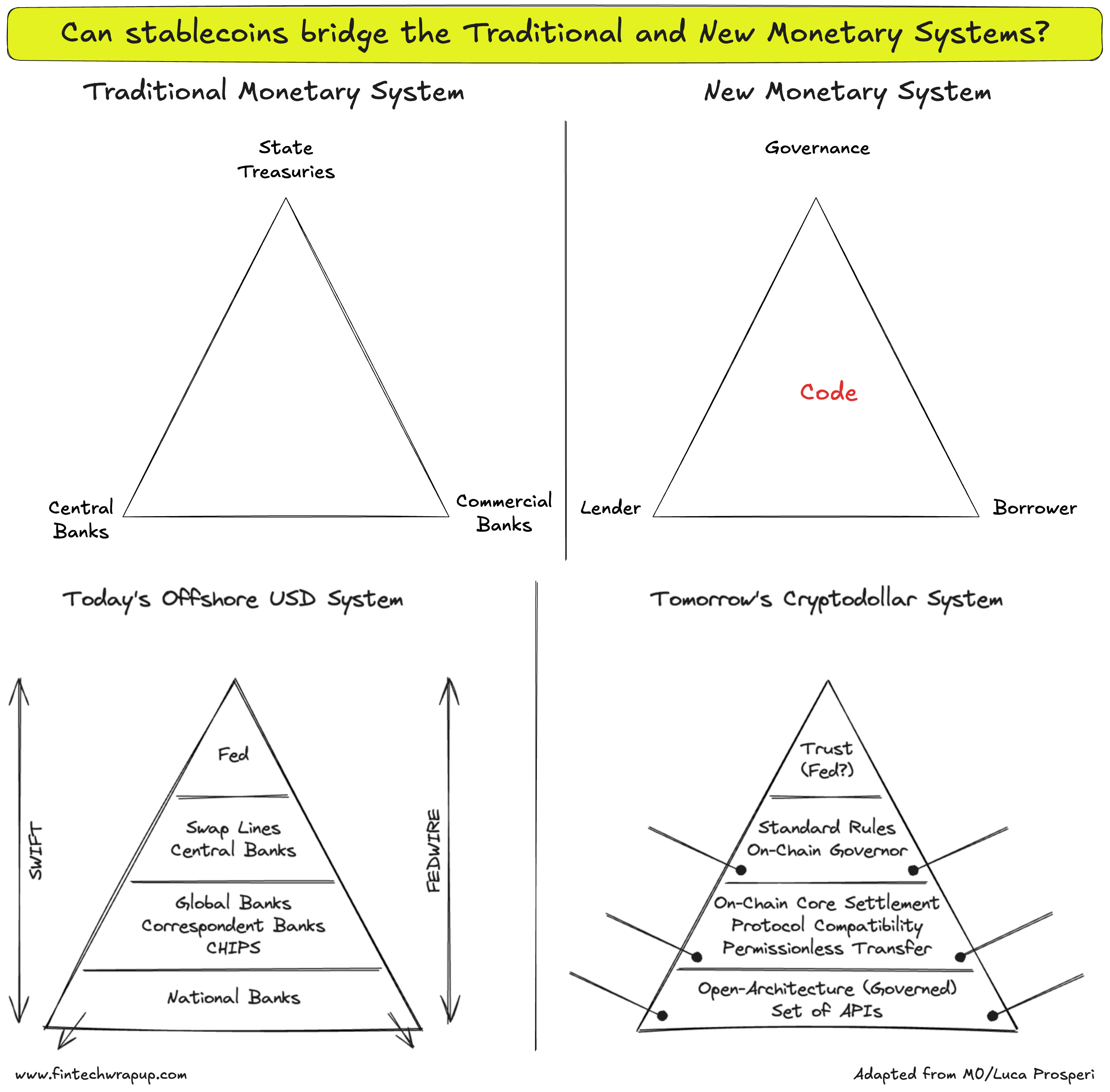

Can stablecoins bridge the Traditional and New Monetary Systems?

The monetary system we know today is relatively new. It emerged after the collapse of Bretton Woods, built on a tightly interdependent relationship between commercial banks, central banks, and state treasuries.

👉 How the traditional system works

Commercial banks supply liquidity by issuing loans in fiat, while central banks set rules and ensure all banks’ money is interchangeable. Treasuries benefit by borrowing cheaply in exchange for maintaining fiscal stability. The system works because roles are clearly divided: banks handle deposits, lending, and risk; central banks provide oversight and backstops; treasuries fund themselves. Banks, in return, enjoy oligopoly protection and profit spreads.

🚨 Where it fails

🔹 Credit underwriting - Shadow banking emerged as banks struggled with complex credit.

🔹 Risk management - Counterparty risks often spill over to taxpayers through bailouts.

🔹 Distribution/storage - Legacy ledger systems look outdated next to CBDCs and self-custody.

🔹 Returns - Low profitability has depressed bank valuations.

🔹 Tech integration - Banks lag in a world where commerce, data, and machine-to-machine interactions move faster than they can adapt.

The Global Financial Crisis and the failures of 2023 (SVB among them) underscored the fragility of this model. The era of zero rates masked weaknesses—higher rates have exposed them. Banking, as structured today, is broken.

👉 The new system taking shape

DeFi shows how banking can be unbundled—credit, deposits, risk—all re-engineered in code. Imagine the most efficient leverage paired with the safest liquidity pools, reshaping how money is managed and moved. Banks, once central hubs, could shrink into utility-like providers. Treasuries must adapt to digital-native value frameworks. Depositors will increasingly rely on apps with seamless digital money management built in.

This shift isn’t welcomed by all. Traditional players fear loss of control, and many will resist. For incumbents, survival demands not just tech upgrades but cultural reinvention—a tall order.

Stablecoins: the bridge technology

Among DeFi’s experiments, stablecoins stand out. They solve real problems—fast, reliable digital settlement for both retail and institutions. Crucially, most issuers didn’t try to replace banks but layered on top of the existing system, a stance regulators could tolerate.

Their rise also connects to an older phenomenon: eurodollars, or offshore dollars. Stablecoins are effectively tokenized eurodollars—today 70–80% are USD-linked. In a way, they are the modern digital continuation of offshore liquidity instruments, turbocharged by blockchain rails.

We’re watching a paradigm shift. The traditional model of commercial banks as the system’s cornerstone is eroding, while programmable, digital-native forms of money—stablecoins and DeFi protocols—are rising.

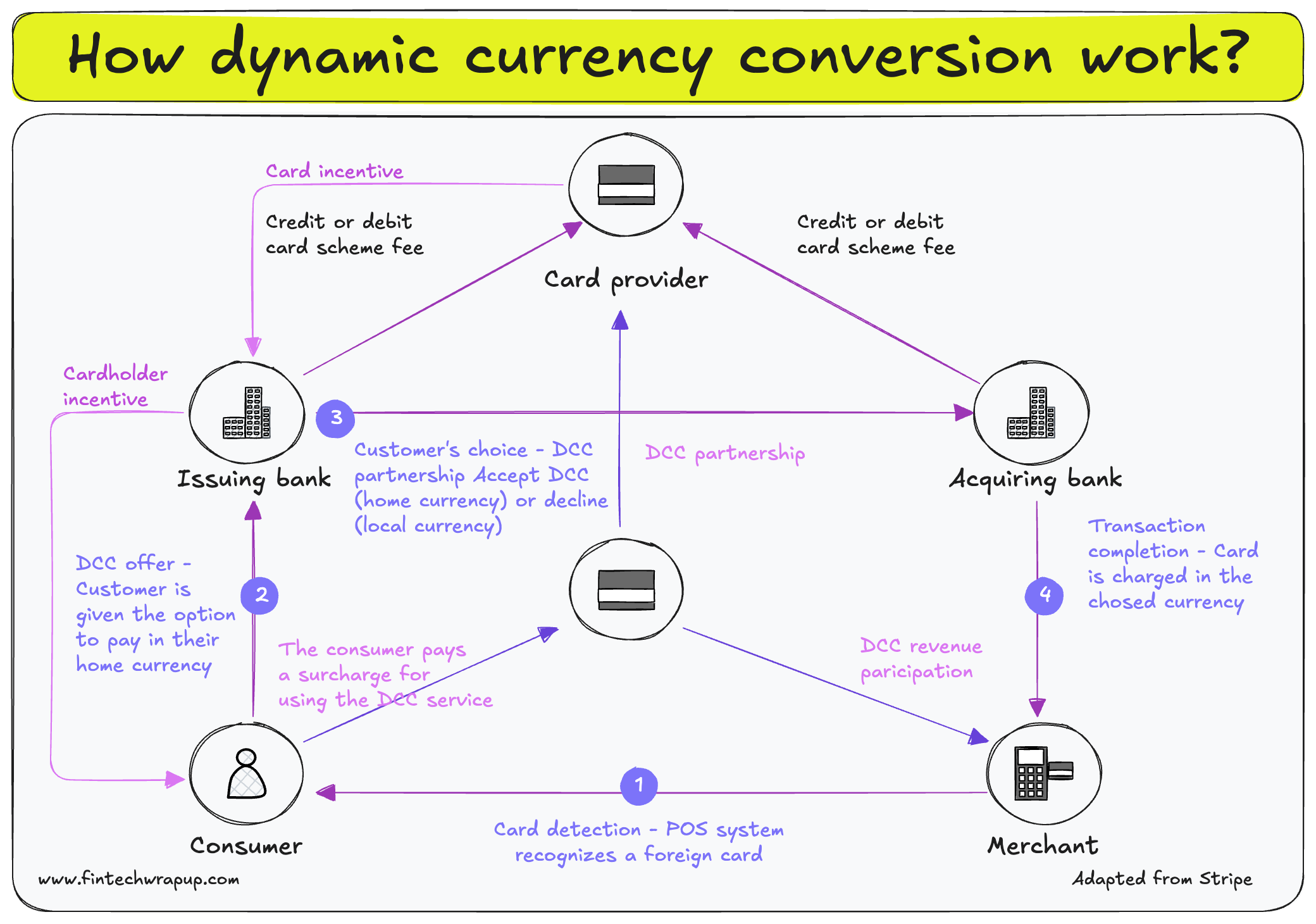

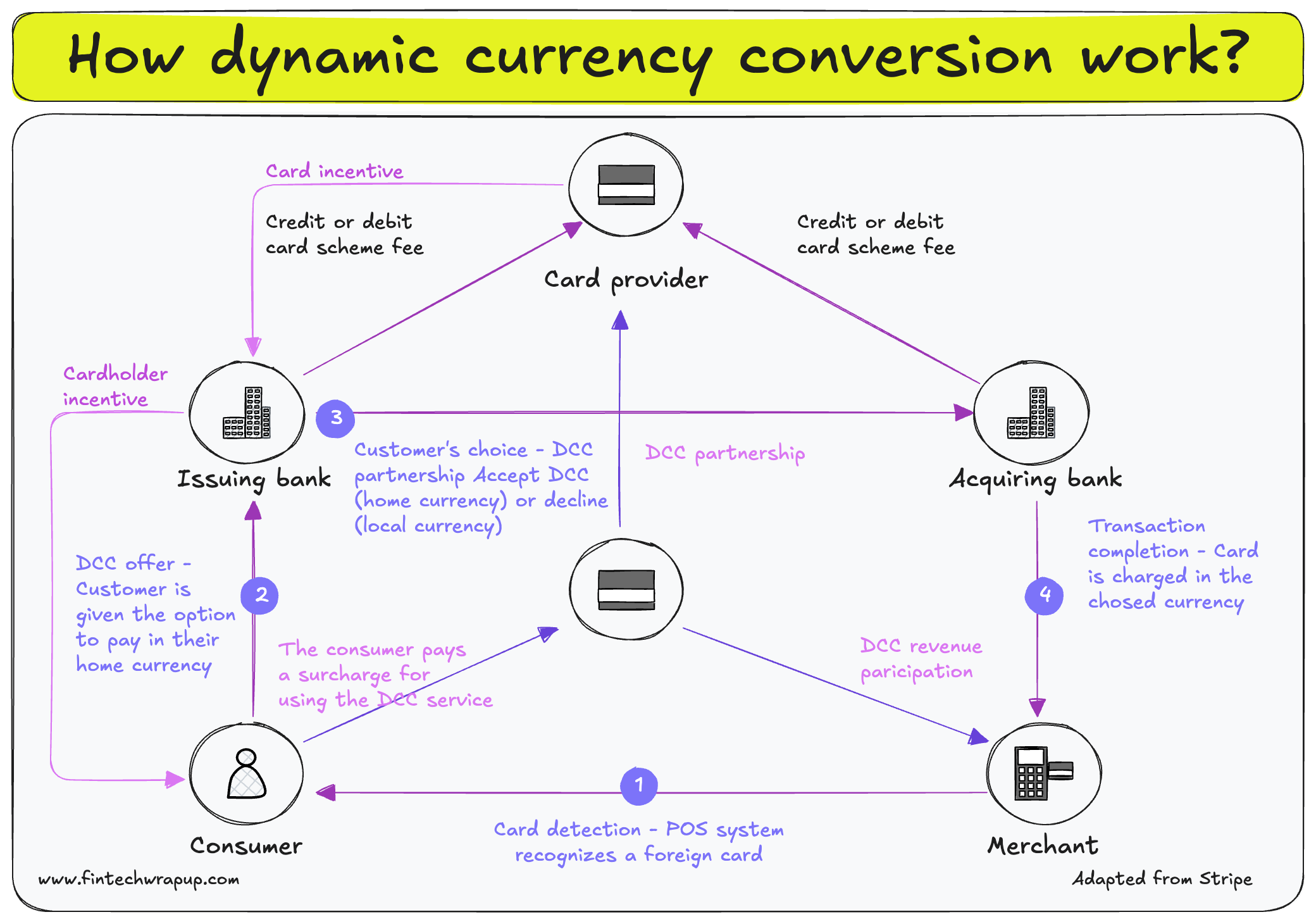

How does dynamic currency conversion work?

Dynamic currency conversion (DCC) is a financial service used in international transactions, when a customer from one country makes a credit or debit card purchase in another. DCC allows the transaction to be processed at the point of sale in the currency of the cardholder’s home country. The global credit card payments market is forecast to jump from $524.9 billion in 2022 to $1.2 trillion by 2032, and cross-border payments are an important piece of that growth.

DCC provides cardholders with a convenient and immediate understanding of transaction costs in their home currency, though it might involve higher costs because of exchange rate markups and fees. For businesses and financial institutions, DCC offers a chance to earn additional revenue. Here’s how it works:

👉 The DCC process

🔹 Card detection: When a customer uses a foreign credit or debit card at a business’s point-of-sale (POS) system or an ecommerce platform, the system identifies the card’s country of origin.

🔹 DCC offer: The business’s system, equipped with DCC technology, automatically offers the cardholder the option to complete the transaction in their home currency. The amount includes the conversion rate and any additional fees involved in the conversion.

🔹 Customer’s choice: The cardholder can accept the DCC offer and pay in their home currency or decline it and pay in the local currency.

🔹 Transaction completion: If the customer chooses DCC, the transaction is processed, and the card is charged in the cardholder’s home currency using the displayed exchange rate. If the cardholder declines DCC, the transaction is processed in the local currency, and the cardholder’s bank will convert it using the bank’s exchange rate.

👉 Roles and benefits

🔹 Businesses: Businesses benefit from DCC by earning additional revenue through commissions or fees associated with the currency conversion process.

🔹 Financial institutions: Banks or financial service providers that offer DCC set the exchange rates and fees. These rates often include a markup over the standard exchange rate.

👉 Technological integration

🔹 Payment processing technology: DCC technology enables the automatic detection of foreign cards and real-time currency conversion, making DCC an easy option at POS systems and online.

🔹 POS systems and ecommerce integration: DCC is integrated into modern POS systems and online payment gateways, letting businesses offer this service to international customers in store and online.

For example, consider an American tourist in Italy who wants to buy an item that costs €100. The POS system recognizes the credit card as American and offers to charge $120 (which includes the DCC exchange rate and fees). The tourist can choose to pay $120, knowing the exact cost in their currency, or pay €100, leaving the conversion to their bank.

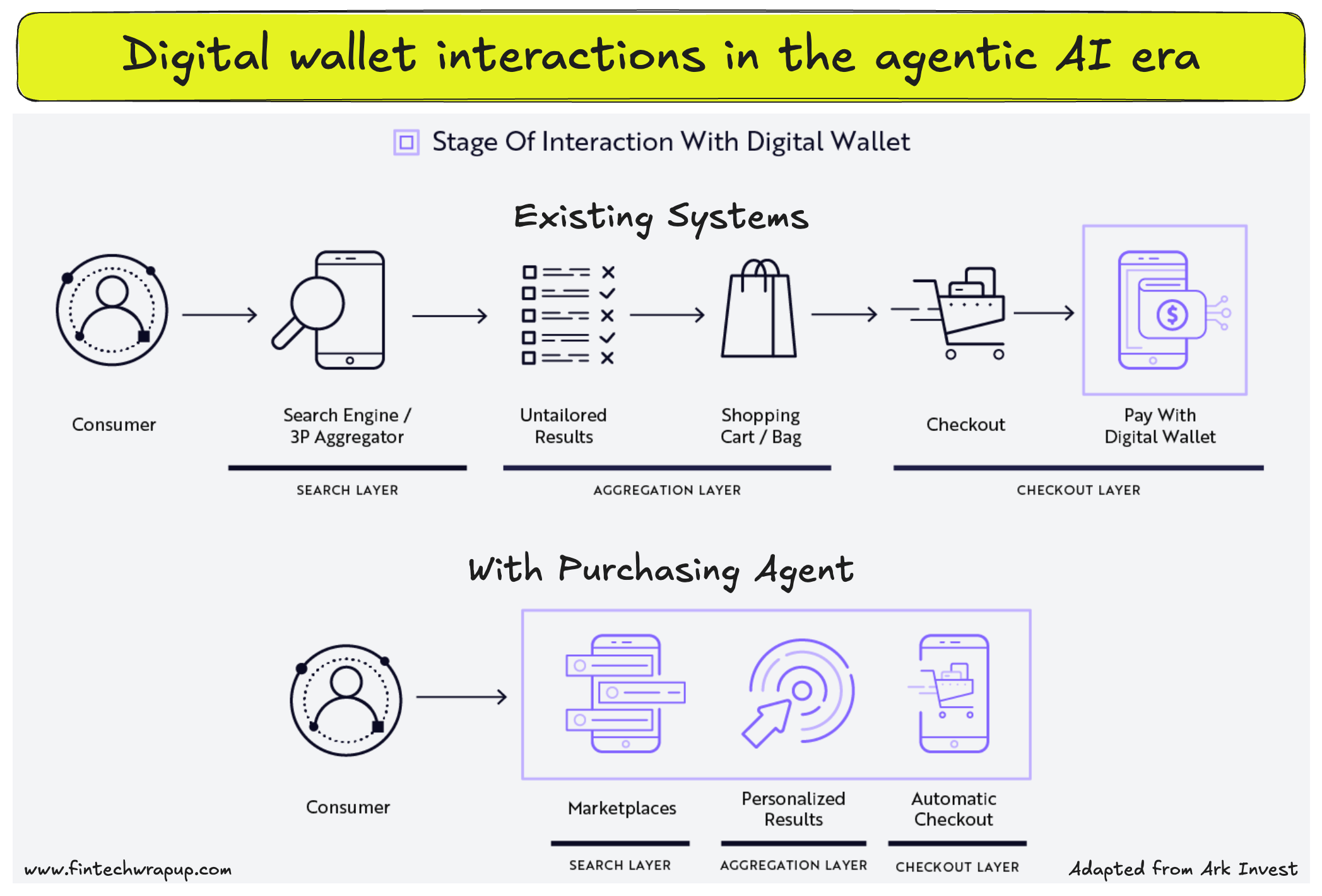

How will digital wallet interaction happen in the agentic AI flow?

As digital wallets increasingly integrate LLM-enabled purchasing agents, consumers are likely to interact with them much earlier in the e-commerce journey.

AI-powered purchasing agents are expected to make one-query purchasing the new industry standard, creating a significant advertising opportunity. For example, Amazon’s “Choice” badges already act as implicit recommenders that boost conversion rates by roughly 25%. One-query purchasing is likely to encourage users to adopt and rely more heavily on purchasing agents for curated suggestions, potentially achieving even higher conversion rates. However, for digital wallets to succeed, sponsors will need to avoid overwhelming consumers with sponsored content and instead build trust by delivering consistently positive experiences.

If digital wallets integrate LLM-backed search, search itself may become commoditized. Research suggests that AI purchasing agents could disrupt the dominance of walled gardens such as Google and Amazon. By automating tasks like product comparisons and purchase decisions, these agents could reduce consumer reliance on search engines and marketplaces for product discovery, effectively disintermediating incumbents. This shift would position AI purchasing agents as challengers capable of breaking the stronghold Google and Amazon currently hold over digital marketplaces.

To drive consumer adoption in this evolving landscape, digital wallets will need to take deliberate steps to disintermediate search and walled gardens. Early adoption will depend on AI-powered purchasing agents offering personalized deals, promotions, discounts, and rewards programs while gathering valuable insights into user preferences and purchase histories. Credit card providers offer a clear precedent: for decades, they have collected consumer data and incentivized behavior through loyalty programs. In 2022 alone, credit card rewards in the United States totaled approximately $40 billion. These loyalty schemes reshaped consumer behavior by directing users toward card portals instead of third-party aggregators. For instance, a large share of younger travelers now book flights and hotels through credit card travel portals rather than online travel agencies.

Digital wallets can replicate this playbook by offering integrated rewards systems that allow users to accumulate and redeem points throughout the e-commerce journey. Retention will be key, as it enables AI purchasing agents to personalize services more effectively. Over time, data-driven insights can fuel hyper-personalized recommendations, strengthening engagement and adoption. Netflix provides a useful parallel: by tailoring content to individual viewing habits and preferences, its recommendation engine now drives the majority of content consumed on its platform. Similarly, in digital commerce, short-term adoption will be essential to securing long-term growth.

Thanks for reading Fintech Wrap Up!

Disclaimer:

Fintech Wrap Up aggregates publicly available information for informational purposes only. Portions of the content may be reproduced verbatim from the original source, and full credit is provided with a "Source: [Name]" attribution. All copyrights and trademarks remain the property of their respective owners. Fintech Wrap Up does not guarantee the accuracy, completeness, or reliability of the aggregated content; these are the responsibility of the original source providers. Links to the original sources may not always be included. For questions or concerns, please contact us at sam.boboev@fintechwrapup.com.