Global A2A/real-time payments developments – from adoption to trends; Visa’s Q2 2024 results; The key components of building a card program;

In this edition, we’re diving into the surge in global A2A and real-time payments adoption, the essentials of building personalized fintech products, and the transformative impact of AI on the banking

Insights & Reports:

1️⃣ Global A2A/real-time payments developments – from adoption to trends

2️⃣ Building beyond banking ecosystems and hyper-personalized offerings

3️⃣ The key components of building a card program

4️⃣ Africa’s Banking and Lending Tech Sector

5️⃣ Visa’s Q2 2024 Results

6️⃣ Digitalization Trends in the Cross-Border Checkout Revolution

Curated News:

1️⃣ ECB Is Pushing UK Fintech Revolut to Bolster EU Bank Controls Amid Review

2️⃣ Chase to Decline Credit Card Payments for Third-Party BNPL Plans

3️⃣ Fintech startup Coast lands $40M just 4 months after its last $25M raise

TL;DR:

The adoption of Account-to-Account (A2A) and real-time payments is surging globally. In the U.S., high interchange fees are pushing the shift towards ACH, which, despite longer confirmation times, remains cost-effective and widely used on platforms like Venmo. The newly introduced FedNow system is expected to revolutionize this space with instant settlement and low fees. Europe, however, is leveraging A2A for unique use cases like egaming and high-value transactions, with initiatives like Bizum offering instant mobile transactions and the European Payments Initiative working towards a unified A2A solution and digital wallet. Latin America's Pix system, accounting for 20% of the region's total ecommerce transaction value in 2023, continues to impress with its cost-effectiveness and strong authentication, and upcoming features like Pix Agendado Recorrente aim to democratize recurring payments. In the Asia-Pacific region, real-time payment systems like India’s UPI, China’s IBPS, and Australia’s New Payments Platform are setting the standard with widespread adoption and interoperability.

We're also exploring how to build personalized fintech products. By leveraging Third Party Providers (TPPs) and customer data, banks can create hyper-personalized offerings that meet specific customer needs, driving retention and satisfaction. For example, a bank can use transaction history to preemptively meet the credit needs of SMEs, improving customer relationships and retention. Understanding the regulatory landscape and investing in technology, such as standardized APIs for secure data sharing, are crucial for these innovations.

Additionally, we cover the essentials of launching a card program, highlighting the need for network licenses, regulatory approvals, and robust payment processors. In Africa, fintech companies are addressing the needs of a largely unbanked population with innovative digital solutions, offering both challenges and opportunities.

On the corporate front, Visa's Q2 2024 results showcase strong financial performance, with GAAP net income at $4.7 billion, driven by a 10% increase in net revenue to $8.8 billion. Payments volume and cross-border transactions saw significant growth, contributing to this success. Meanwhile, AI continues to revolutionize banking by enhancing workforce productivity, optimizing software code, and improving risk management and customer retention. AI-powered digital agents are reducing customer wait times and enhancing the overall customer experience.

In our curated news, we look at the European Central Bank's push for Revolut to bolster its EU bank controls, Chase's new policy on credit card payments for third-party BNPL plans, and fintech startup Coast's impressive fundraising efforts, securing $40 million just four months after their last raise.

Insights

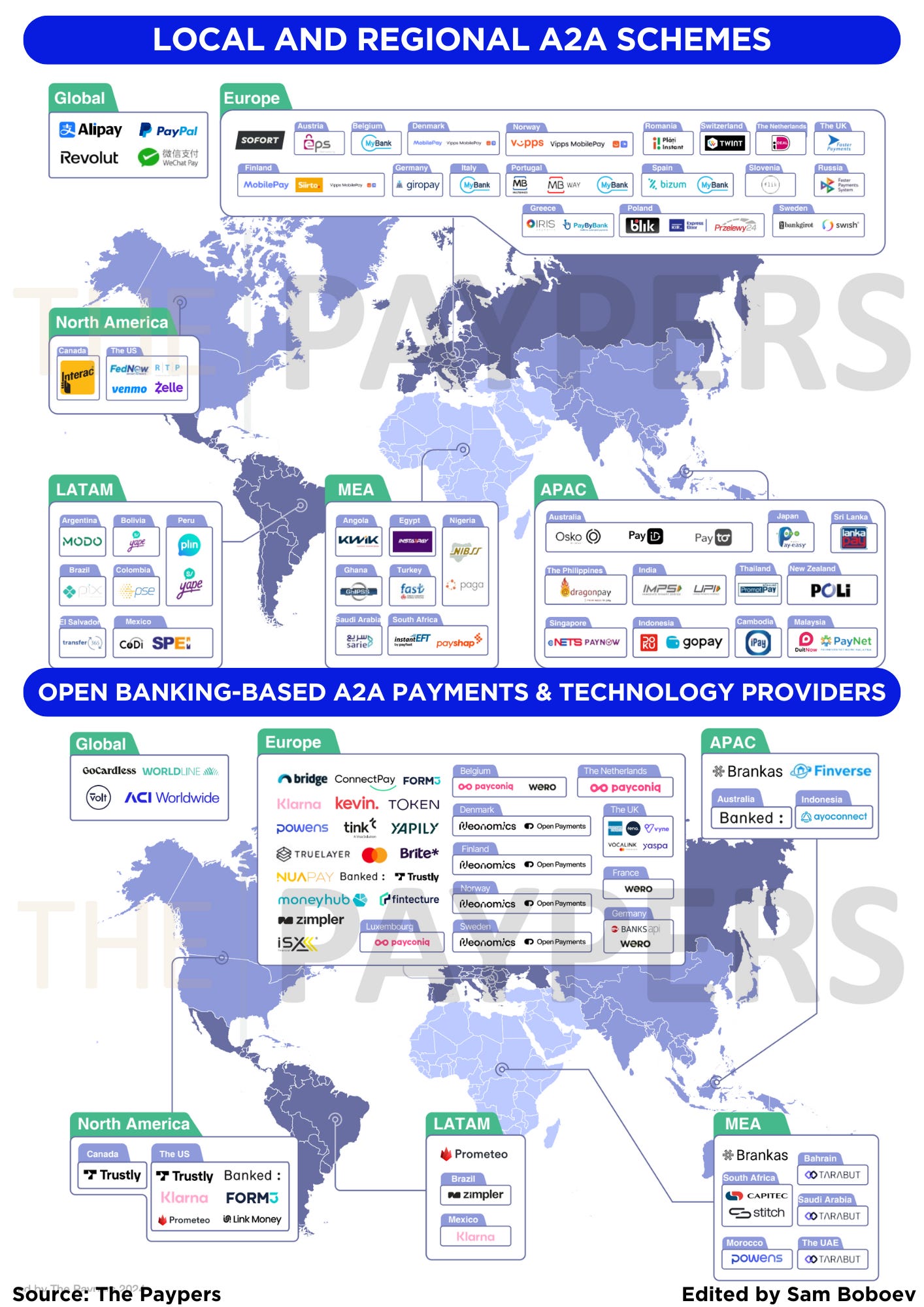

Global A2A/real-time payments developments – from adoption to trends

In the United States, the adoption of Account-to-Account (A2A) payment rails is primarily driven by the high interchange fees associated with card payments, as these fees are not capped and remain significant. The primary A2A rail has been the Automated Clearing House (ACH) network, known for its cost-effective transactions despite longer confirmation times. ACH is widely integrated with platforms like Venmo to reduce costs and improve margins. The introduction of the FedNow system in 2023 is expected to revolutionize this space, offering both low fees and instant settlement.

In Europe, the cost of card payment processing is significantly lower than in the US, so businesses are less concerned with processing costs. Consequently, A2A payments in Europe focus on other use cases, such as supporting high-risk businesses like egaming and betting, which benefit from Open Banking. A2A payments are also vital for high-value transactions, utilities, and recurring bills. While Open Banking payments are not yet recurring, the industry is working towards this goal. The most widely adopted A2A payment method in Europe is direct debit, valued for its ease of use, reliability in recurring transactions, low cost, and low friction for users. Notable developments include Bizum, a Spanish banking sector initiative offering instant mobile transactions, and the European Payments Initiative (EPI), which aims to create a unified A2A solution and digital wallet (wero) for Europe.

In Latin America, A2A payments accounted for 20% of total ecommerce transaction value in 2023. Brazil leads the region with its Pix system, introduced by the Central Bank of Brazil, offering cost-effectiveness, instant settlement, and strong authentication. Despite its success, Pix faces challenges in handling recurring payments due to the need for strong authentication for each transaction. The Central Bank is addressing this with new developments such as Pix Agendado (scheduled Pix), Pix Agendado Recorrente (recurring scheduled Pix), and Pix Automático (automatic Pix) set to launch in October 2024, aiming to democratize access to recurring payments.

The Asia-Pacific (APAC) region is characterized by the widespread adoption of real-time payments and interoperability. China launched its Internet Banking Payment System (IBPS) in 2010, ranking second worldwide in transaction volume of real-time payments by 2021. Australia’s New Payments Platform (NPP) is another notable example. In Southeast Asia, Singapore’s PayNow and Thailand’s PromptPay offer QR code-based real-time payments. India’s Unified Payments Interface (UPI) is a comprehensive real-time payment solution that supports interbank transactions, consolidates multiple accounts into a single app, and enables both P2P and merchant payments.

Source The Paypers

Keep reading with a 7-day free trial

Subscribe to Fintech Wrap Up to keep reading this post and get 7 days of free access to the full post archives.