From embedded to orchestrated finance; Traditional banking vs. platform banking; What’s behind Stripe International’s $1bn losses?;

In this edition, we explore the transformative shift toward platform banking, the evolution from embedded to orchestrated finance, and the scaling strategies fintechs use to achieve rapid growth

Insights & Reports:

1️⃣ Traditional banking vs. platform banking

2️⃣ From embedded to orchestrated finance

3️⃣ Scaling from $1 to $10 million ARR

4️⃣ Airwallex’s business model

5️⃣The Bank of Thailand's (BOT) Retail CBDC pilot program

6️⃣ Evolution of the European Digital Identity Framework

7️⃣ What’s behind Stripe International’s $1bn losses?

8️⃣ Walmart Plans Instant Bank Payments, Cutting Out Card Networks

9️⃣ AtoB Raises $130 Million to Fuel Transportation Payments Services

TL;DR:

Welcome back to another edition of Fintech Wrap Up! This week, we’re diving into some exciting trends reshaping the banking and fintech landscape.

First, we take a closer look at the rise of platform banking, where banks shift from traditional models to offering customers a digital marketplace of services. This new approach, driven by regulations like PSD2, allows for better customer experiences and opens up new revenue streams, but it requires careful strategy and investment. Platform banking is set to be a game changer in the financial world.

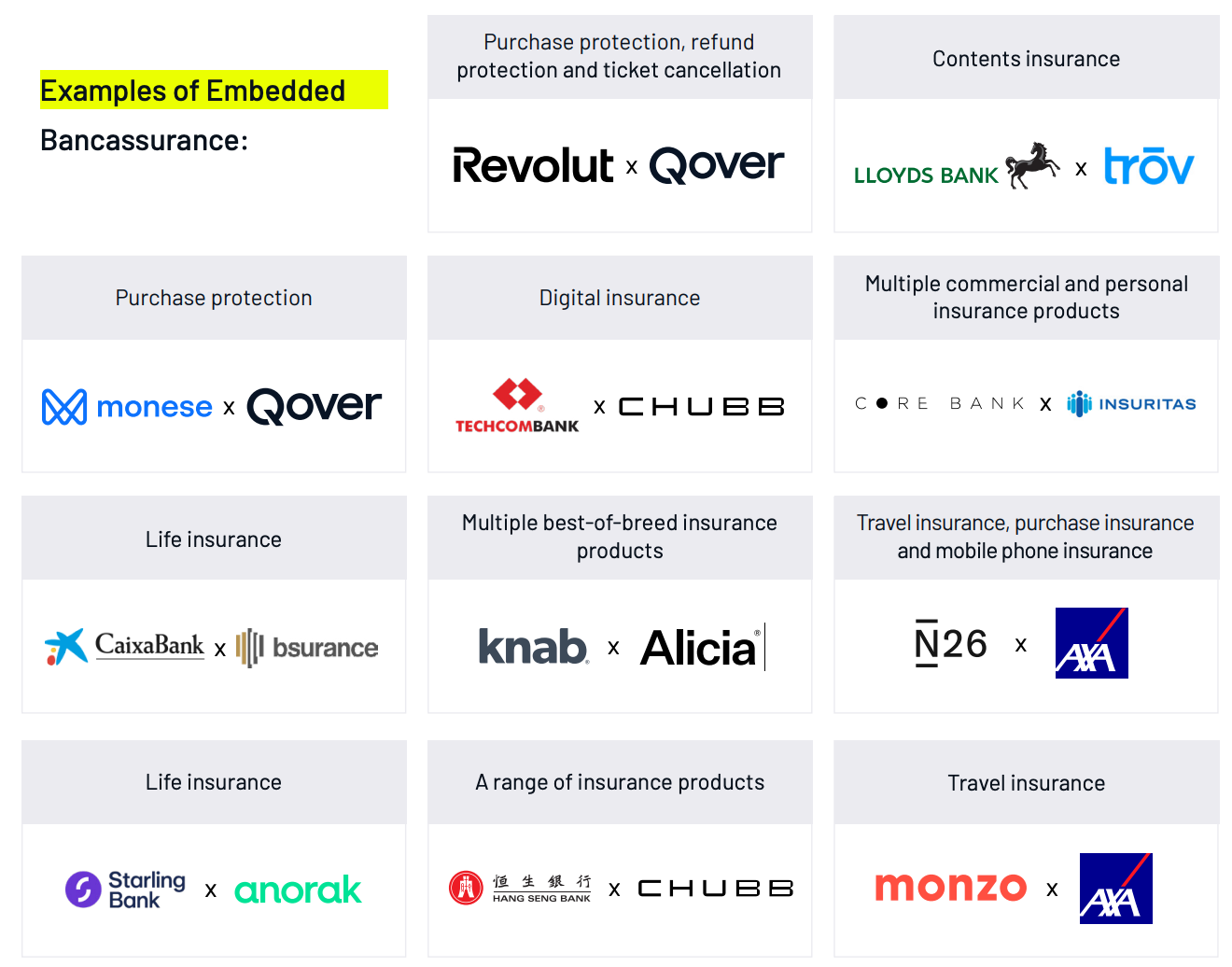

Next up, we explore the transition from embedded to orchestrated finance. As fintech matures, we’re seeing the re-bundling of services. Companies like Wise and Revolut are great examples of how fintechs expand by integrating additional products, creating a seamless ecosystem for their users. This bundling trend is particularly relevant for bancassurance, where the embedded finance model allows for personalization and increased loyalty.

Then, we shift gears to scaling fintechs. Moving from $1 million to $10 million ARR is the critical stage where companies go from a feature-driven business to a full-fledged platform. Companies like Netlify and Twilio illustrate how adding features and upsell opportunities can help fintechs expand their customer base and solidify their presence in the market.

We also take a deep dive into Airwallex’s business model. Founded in 2015, Airwallex grew rapidly by offering affordable cross-border payments, and now, it’s evolving into an embedded finance platform. Their ability to process transactions through their own network gives them a unique advantage, allowing faster, cheaper international transfers and positioning them as a leader in cross-border finance.

Lastly, we explore the Bank of Thailand’s Retail CBDC pilot, where over 4,000 users and 140 merchants tested a digital currency across live transactions. The test results offer a glimpse into the future of retail payments, showcasing the technical capabilities and real-world potential of central bank digital currencies.

Insights

Traditional banking vs. platform banking

Platform banking is a digital marketplace, owned and operated by a bank or another third party, that provides banking and nonbanking services. As with open banking, sharing of customer data happens only with customer’s consent. Moreover, platform banking also requires secure data transmission via APIs. The premise behind platform banking is that banks can serve customers better, engender more trust, and retain the customer relationship. Open banking enables and amplifies platform banking.

As described above, platform banking helps banks to better serve their customers by offering a suite of banking products and services in a marketplace model, where an existing customer can pick and choose products offered by different financial institutions. Platform banking may, in fact, be poised to change banking as dramatically as other digital trends has over the past decade. Figure below depicts how the relationship between a customer and their bank transforms from a one-to-one relationship to a one-to-many relationship.

A host of factors and trends are driving banking towards platform banking. Globally, regulators have been on the forefront of change; for example, the European Union introduced the Second Payment Services Directive (PSD2), leading to a disruption of the payments landscape. In the United States, though a regulatory push is not on the horizon, emerging market forces, such as declining profitability, a desire to find new revenue sources, and the entrance of “big tech” into financial services, are making a case for platform banking. In order to prepare and exploit opportunities presented by platform banking, banks will have to review near-term and long-term business goals and determine the optimal platform banking strategy. Banks will gravitate, based on their business, organizational, and technology maturity and goals, toward one of the three platform strategies: marketplace owner, marketplace partner, and utility provider. Each strategy requires varying degrees of investment and will have varying degrees of transformative impact.

Keep reading with a 7-day free trial

Subscribe to Fintech Wrap Up to keep reading this post and get 7 days of free access to the full post archives.