Digital Commerce Payment Platforms; Not All Rails or Stablecoins are Equal; Fiat-to-crypto infrastructure is not a payments problem

Video of the Week

Deep Dive of the Week

The hidden liability of agentic commerce

In the last decade, we have watched the global financial system transition from physical cards to digital wallets and from manual bank wires to real-time rails. Each of these shifts was marketed as a convenience play for the consumer. In reality, each shift was an architectural reset for the merchant. We are now entering the most volatile phase of this evolution: agentic commerce. This is not just another checkout button. It is a structural rewiring of how demand is captured, how intent is verified, and how liability is distributed. I define agentic commerce as the transition from a world where humans click “buy” on a screen to a world where autonomous software agents initiate, authorize, and settle transactions on behalf of users.

For the fintech founders, CEOs, and payments strategists reading this, the promise of a frictionless $1 trillion market is enticing. But I am here to tell you that the current payment infrastructure is fundamentally broken for this new reality. The industry is currently ignoring a massive hidden liability. When an AI agent buys the wrong product or acts without explicit consent, the merchant is the one left holding the bill. Traditional fraud detection is dead in this environment. If your risk model still relies on monitoring typing cadence or mouse movements, you are already obsolete. We are moving into a “fifth participant” model where the AI agent acts as a new layer of intermediation between the cardholder and the merchant. This fifth actor breaks the historical four-party model of liability and pushes risk downstream to you.

This week’s reports

1️⃣How Retail Banks Can Put AI Agents to Work

2️⃣How crypto cards quietly became the main bridge between stablecoins and real-world spending

3️⃣Blockchain, Graph Theory, and the Path to Streaming Financial Services

4️⃣From AI-Assisted Banking to Autonomous Banks

5️⃣Agentic AI will compress margins and reshape financial infrastructure

6️⃣Next-Gen Acquiring Processing

7️⃣Deep Dive into Fintech Mercury

This week’s insights

1️⃣Not All Rails or Stablecoins are Equal

2️⃣Fiat-to-crypto infrastructure is not a payments problem. It is a ledger problem

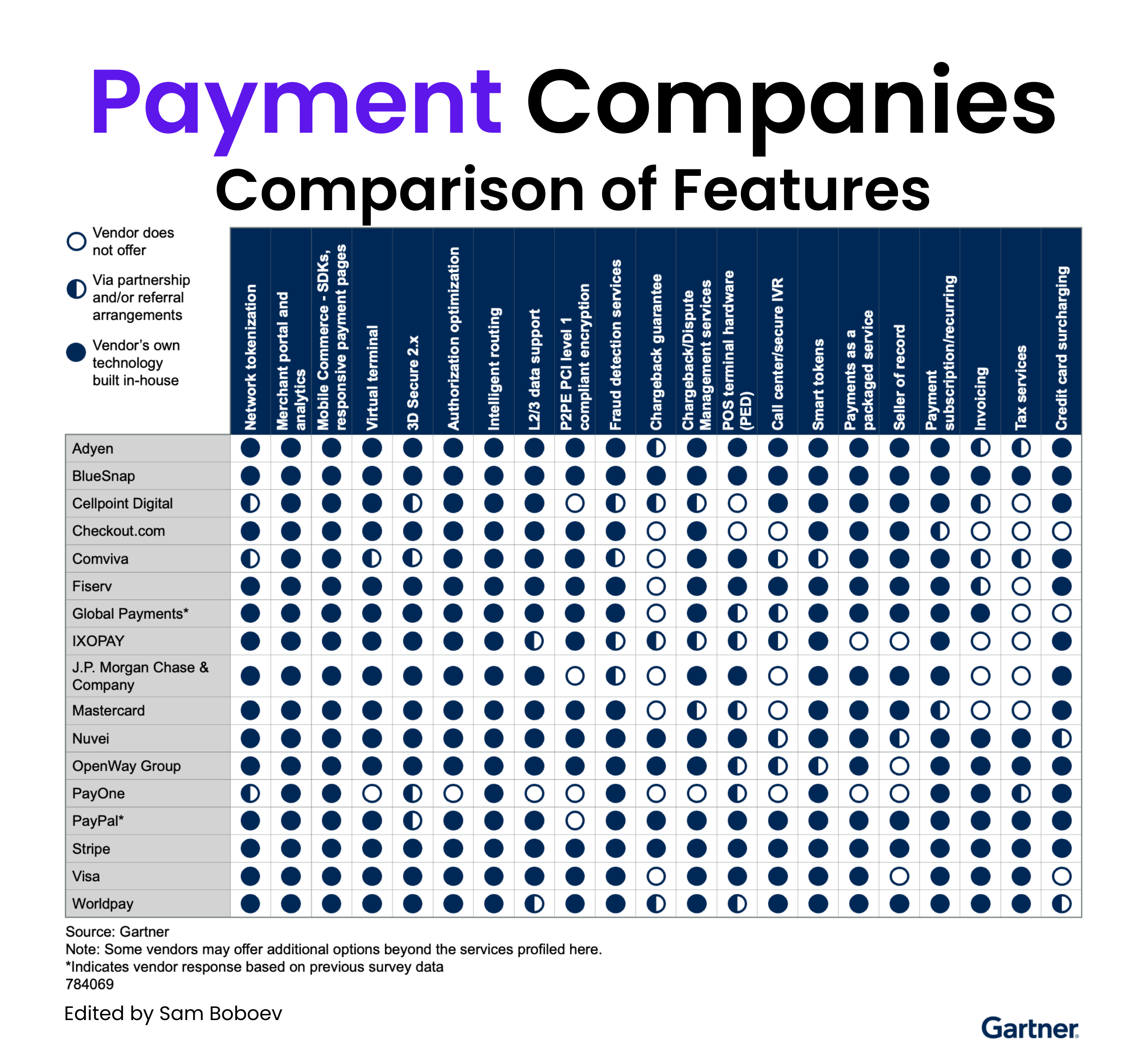

3️⃣Digital Commerce Payment Platforms

4️⃣Understanding custody models for tokenized assets

5️⃣Agentic Commerce as a Proportion of Total E-commerce

6️⃣One of the fastest-growing financial institutions globally

7️⃣4 Payment KPIs That Reveal Where Revenue Is Actually Leaking

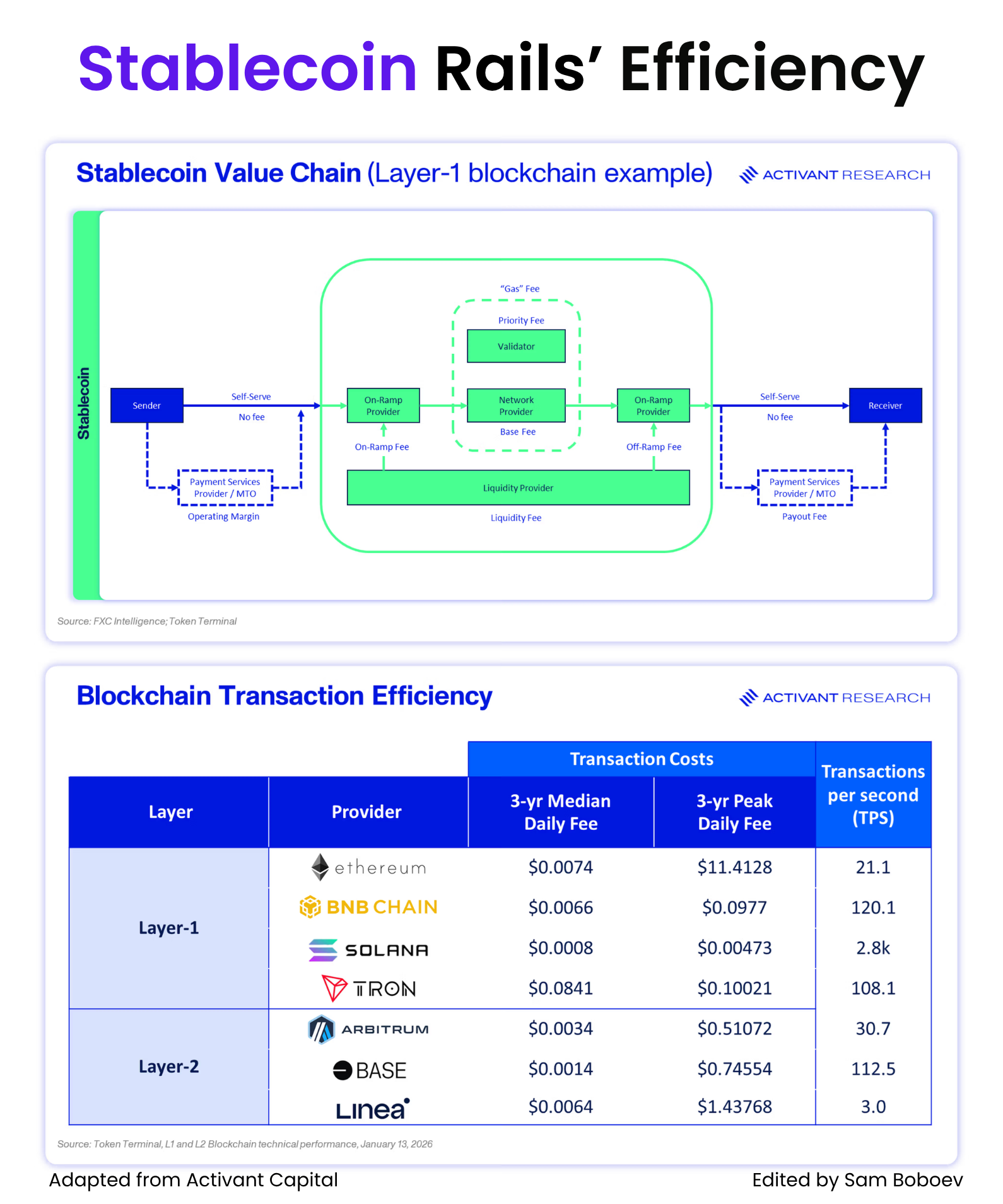

Not All Rails or Stablecoins are Equal

The “average of averages” is often misleading, especially in cross-border payments.

Stablecoins are typically fast (assuming no fiat on-/off-ramp dependencies), but not always cost-effective, with highly volatile pricing. Data from Token Terminal shows Ethereum’s average daily transaction fee over three years was $0.134, with peaks up to $29.58. The median was $0.0074, peaking at $13.093. The variability is significant.

Layer-2 stablecoins offer a different profile, with lower fees despite being built on layer-1s like Ethereum. Over the same period, Arbitrum One recorded an average fee of $0.0127, peaking at $0.7033, with a median of $0.0034 and peak of $0.51072.

The data shows Ethereum’s dominance is driven less by performance and more by liquidity and distribution. Importantly, these figures reflect only on-chain “gas” fees—composed of base and priority fees.

In reality, costs extend across the full value chain: on-/off-ramp fees (including AML/KYC and FX), liquidity provider fees, and PSP or MTO charges tied to transaction size. Additional fees may apply on payout. Users can reduce costs by transacting directly via wallets.

Keep reading with a 7-day free trial

Subscribe to Fintech Wrap Up to keep reading this post and get 7 days of free access to the full post archives.