Deep Dive: Visa’s Product Ecosystem and Strategy

From Visa’s groundbreaking innovations like Tap to Pay and Tokenization to its ambitious $200 trillion opportunity in new payment flows, this edition explores how Visa is transforming global commerce

TL;DR:

Hi there, and welcome to this edition of Fintech Wrap Up! Let’s dive into some exciting updates from the payments world. This week, the spotlight is on Visa, one of the leading names in digital payments. Since its inception in 1958, Visa has been a pioneer in facilitating seamless transactions globally. With operations spanning over 200 countries and territories, Visa continues to innovate through its advanced processing network, VisaNet, offering solutions that simplify and secure money movement for consumers, businesses, and governments.

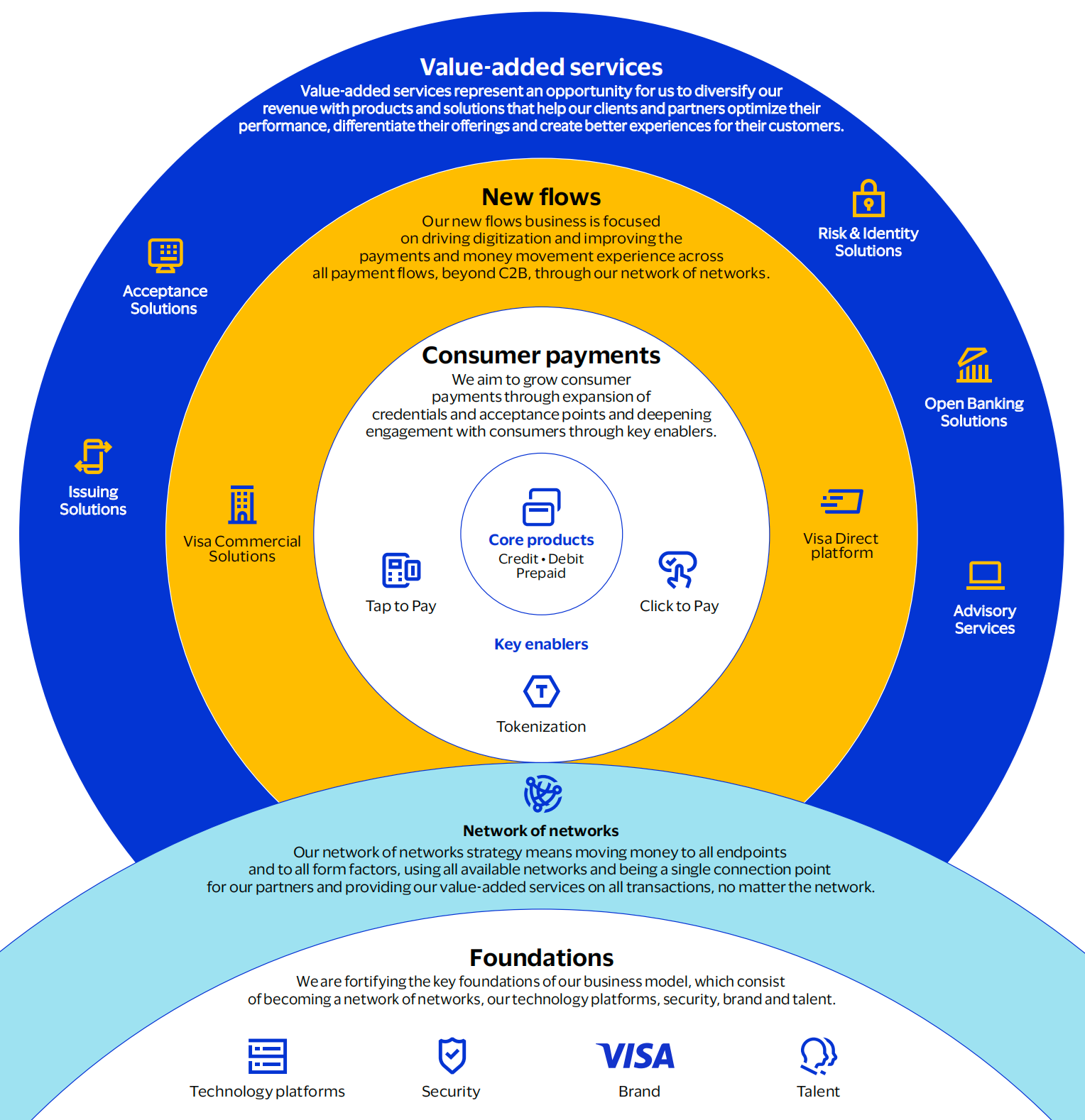

From core products like credit, debit, and prepaid cards to cutting-edge initiatives like Tap to Pay, Tokenization, and Click to Pay, Visa is shaping the future of payments. Did you know Tap to Pay is now the go-to payment method in nearly 60 countries, with over 90% penetration in face-to-face Visa transactions globally? Plus, Visa’s Tokenization Service has provisioned a staggering 11.5 billion network tokens, enhancing security for digital transactions.

Visa is also doubling down on new payment flows, like B2B, P2P, and G2C, representing a $200 trillion opportunity. With platforms like Visa Direct and B2B Connect, it’s redefining how businesses and individuals move money across borders. On the value-added services front, Visa’s suite spans fraud prevention, open banking with Tink, and advisory services through Visa Consulting and Analytics, all designed to empower partners and optimize customer experiences.

Whether it’s enabling small businesses with commercial solutions or scaling open banking in Europe and the U.S., Visa is setting the stage for a future of connected, efficient, and secure payments. Stay tuned for more updates in next week’s edition! These insights are reshared from Visa’s original publication, highlighting their vision and innovation in the payments space.

Visa’s Product Ecosystem and Strategy

Visa is one of the world’s leaders in digital payments. Visa's purpose is to uplift everyone, everywhere by being the best way to pay and be paid. Visa facilitates global commerce and money movement across more than 200 countries and territories among a global set of consumers, merchants, financial institutions and government entities through innovative technologies.

Since Visa’s early days in 1958, Visa has been in the business of facilitating payments between consumers and businesses. Visa is focused on extending, enhancing,and investing in Visa's proprietary advanced transaction processing network, VisaNet, to offer a single connection point for facilitating payment transactions to multiple endpoints through various form factors. As a network of networks enabling global movement of money through all available networks, Visa is working to provide payment solutions and services for everyone, everywhere.

Visa’s Core Business

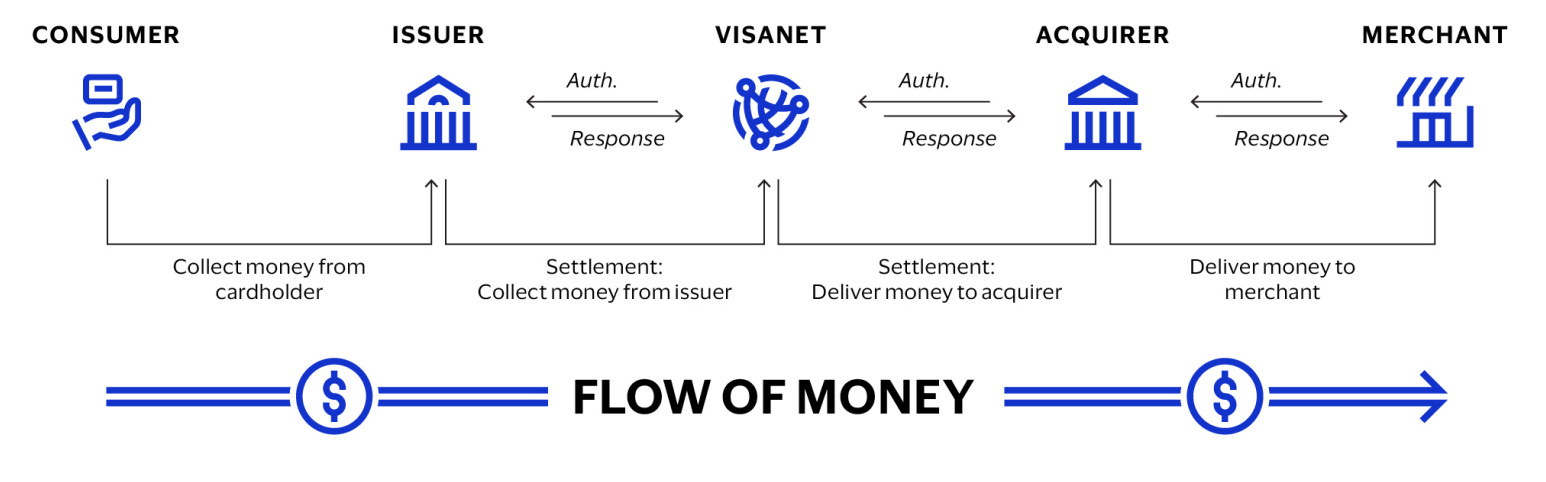

In a typical Visa C2B payment transaction, the consumer purchases goods or services from a merchant using a Visa card or payment product. The merchant presents the transaction data to an acquirer, usually a bank or third-party processing firm that supports acceptance of Visa cards or payment products, for verification and processing. Through VisaNet, the acquirer presents the transaction data to Visa, which in turn sends the transaction data to the issuer to check the account holder’s account balance or credit line for authorization. After the transaction is authorized, the issuer posts the transaction to the consumer’s account and effectively pays the acquirer an amount equal to the value of the transaction, minus the interchange reimbursement fee. The acquirer pays the amount of the purchase, minus the merchant discount rate (MDR), to the merchant.

Keep reading with a 7-day free trial

Subscribe to Fintech Wrap Up to keep reading this post and get 7 days of free access to the full post archives.