Deep Dive: The Emergence of the Bank Operating System

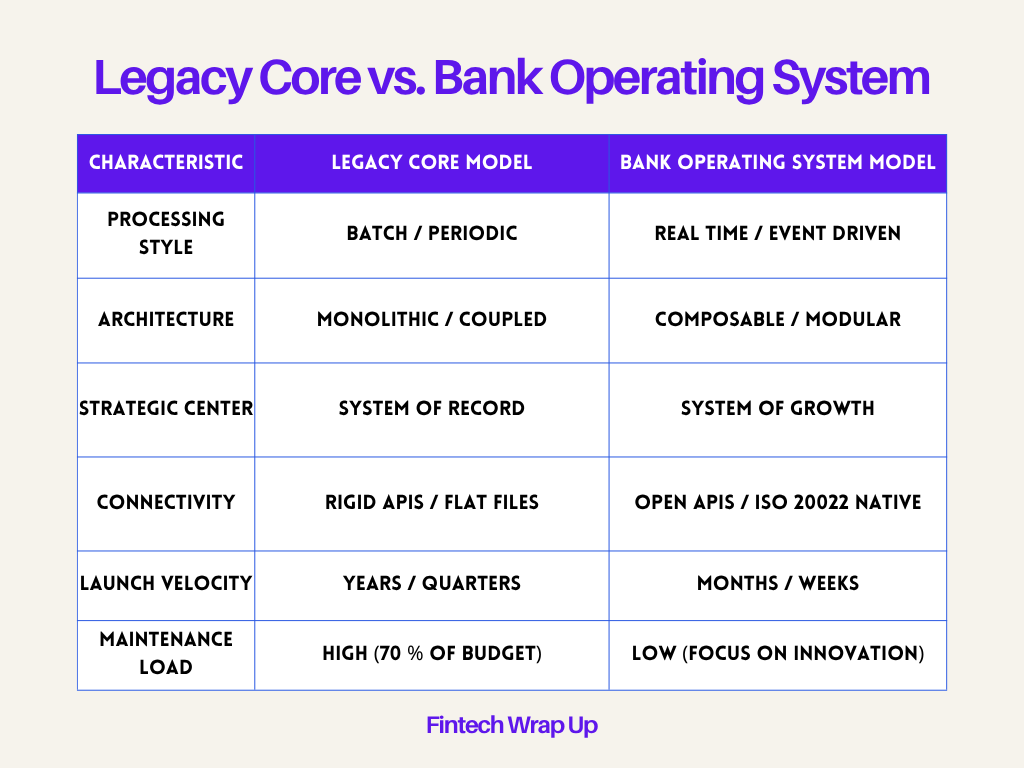

For decades, the financial industry has operated under the assumption that the core banking system is the sun around which all other technologies must orbit. This core-centric model was functional in an era of physical branches and daily batch cycles, but it has become a terminal constraint in the modern digital economy. The core is a monolithic system of record designed for stability over velocity. It was built to store data, not to orchestrate real-time commerce. In my analysis, the gravitational pull of these legacy cores is currently preventing banks from participating in the most lucrative segments of the fintech revolution.

Every modernization strategy over the last twenty years has been a variation of architectural accumulation. Banks add middleware to translate legacy code. They add point solutions to handle specific mobile features. They add third-party Banking as a Service platforms to enable fintech partnerships. The result is a surface-level digital experience that masks an underlying foundation of legacy debt. Smaller institutions that remain release cycle-bound, unable to launch a single feature without their vendor’s permission. Mid-sized banks are struggling with fragmented modernization and integration drag. Large banks are attempting in-house builds that are too expensive and slow to scale. These are different strategies, but they all suffer from the same friction.

What I see now is the formation of a new category: the Bank Operating System. This is a real-time, composable growth layer that repositions strategic control inside the bank. In this model, the core becomes the system of record while the operating system becomes the system of growth. This distinction is foundational. A real-time operating system layer helps banks launch revenue-generating products quickly, activates new payment rails without integration friction, and operates independently of core downtime.

The architectural debt crisis

90% of US banking core software is considered legacy. These systems were designed for a different era where batch processing and rigid architectures were the norm. In a batch environment, transactions are stored and processed in groups, usually overnight. This is incompatible with a world that demands instant payment confirmation and 24/7 availability.

The true cost of staying on these legacy systems is staggering. I have seen data indicating that universal banks allocate 70% of their IT budget to system maintenance, leaving only 30% for innovation. As the pool of COBOL and mainframe experts shrinks due to retirement, the cost of maintaining these systems escalates. Finding specialists who understand these decades-old systems is becoming difficult and expensive every year. When a bank’s primary technology is a black box that few people understand, the risk of a catastrophic failure increases every year.

Middleware was supposed to solve this problem by layering modern experiences on top of legacy cores. I believe this has only provided a temporary solution. Middleware is still mostly a connective tissue to the core and continues to depend on fragmented, older systems for functionality, which complicates integration and creates performance issues. Middleware does not solve the fundamental problem of siloed data and batch constraints. It merely hides them. Banks using this approach still suffer from fragmented experiences across mobile, web, and branch channels. Customers expect real-time visibility, and they are increasingly frustrated when a mobile app shows one balance while a branch teller sees another.

Defining the Bank Operating System category

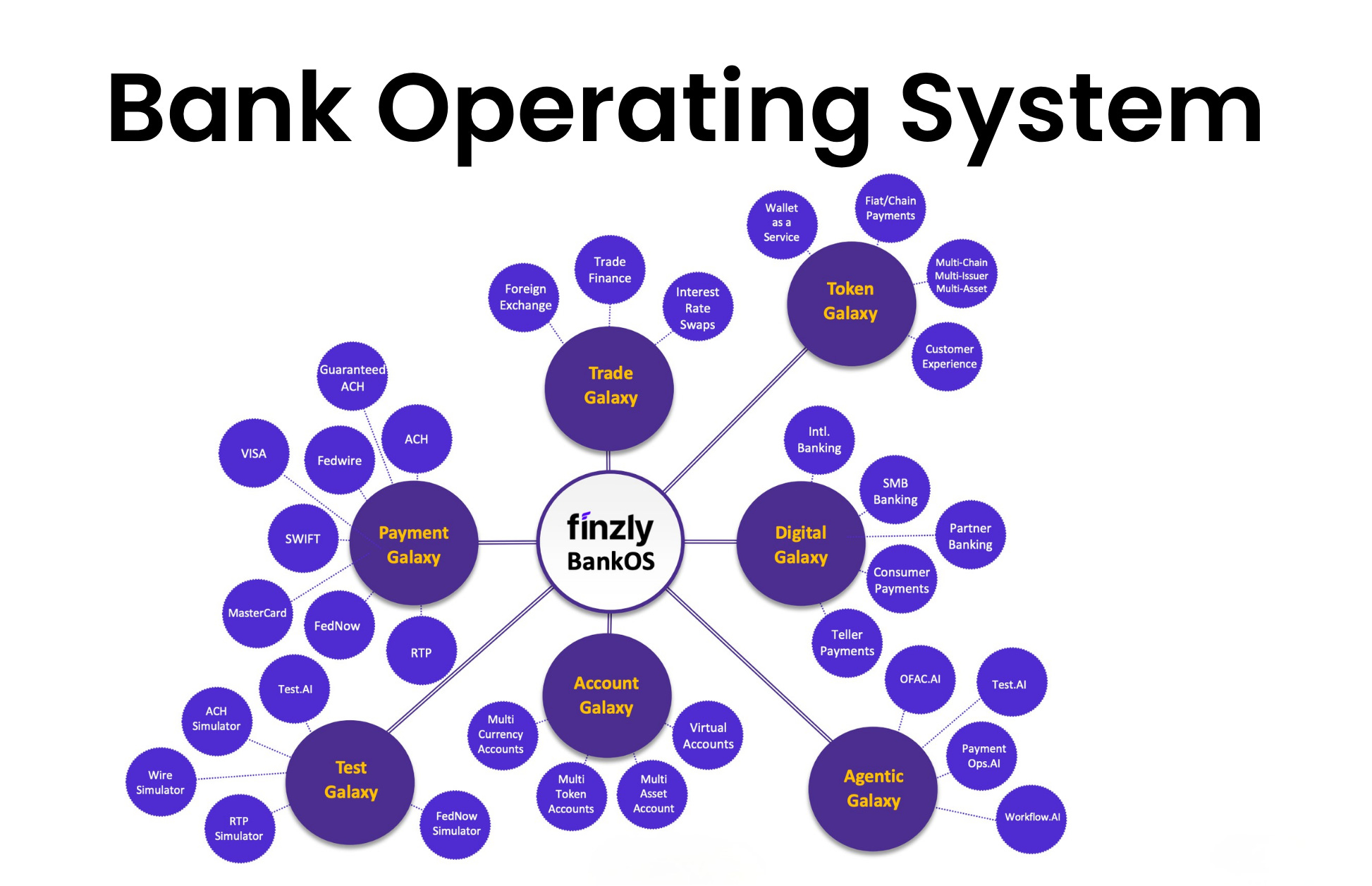

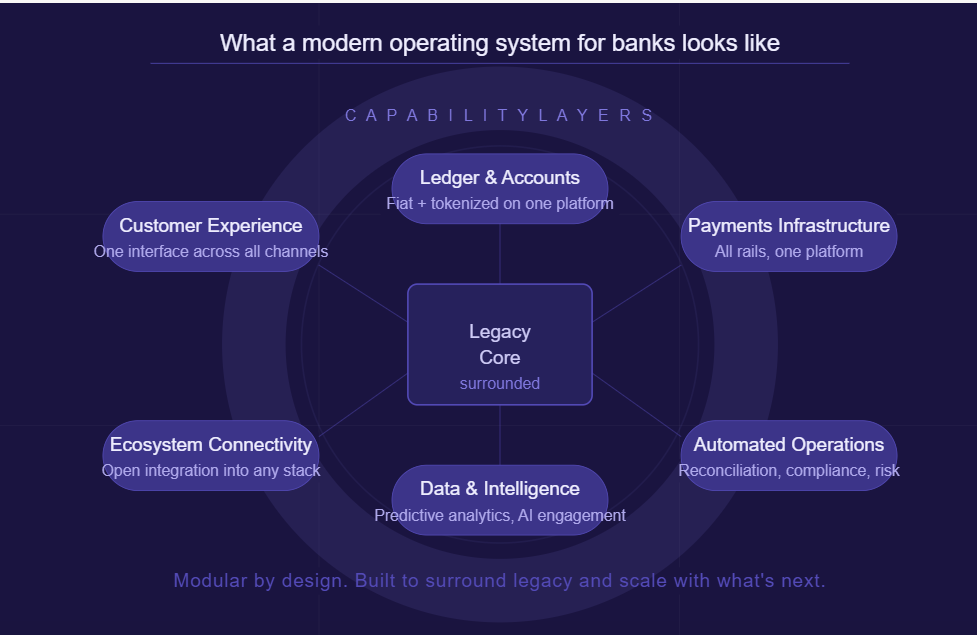

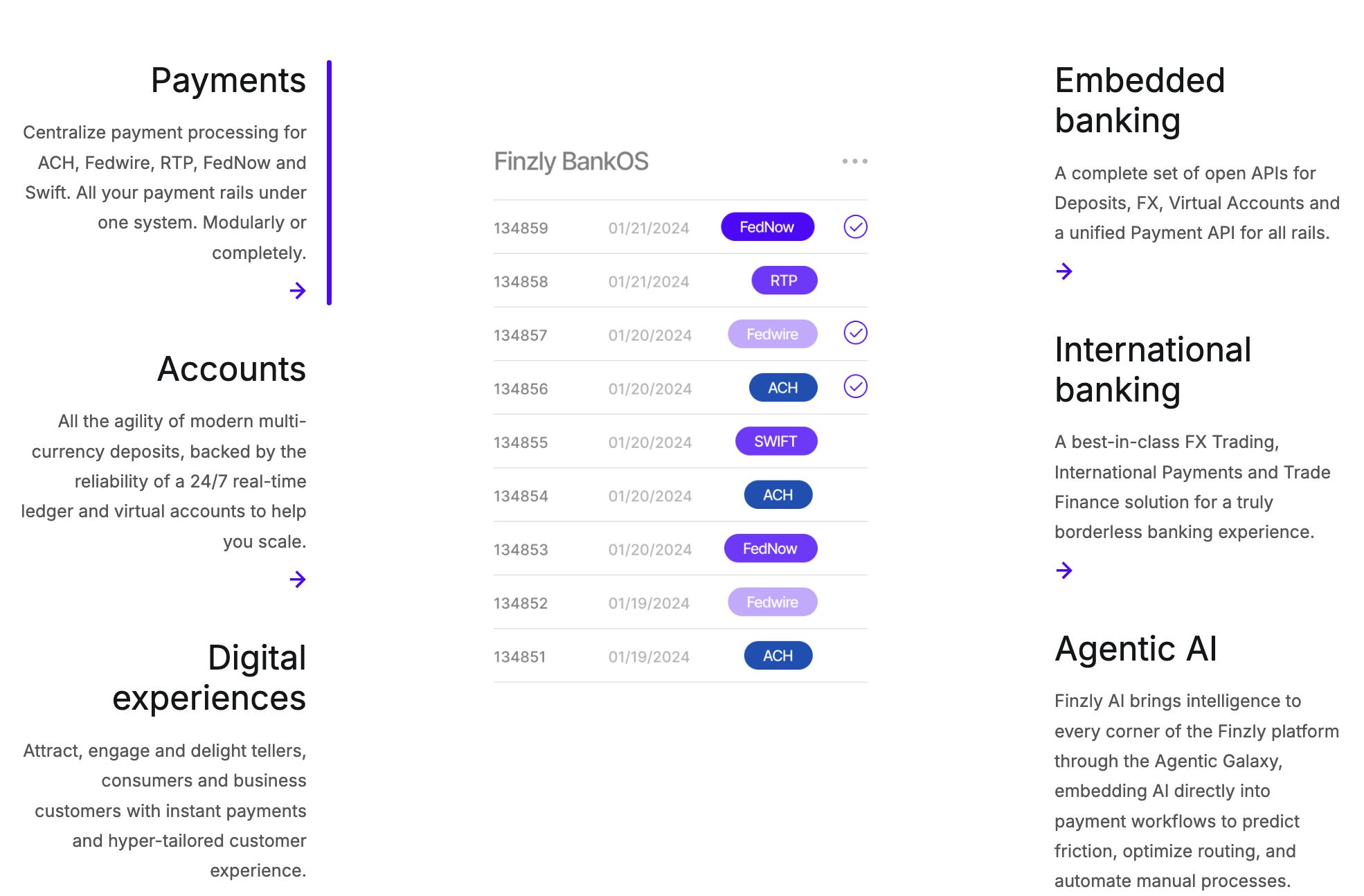

I define a modern bank operating system as a cloud native environment that surrounds legacy cores to unify all banking capabilities. It is a modular system that enables banks to innovate at the speed of fintech by leveraging modern, composable technology architecture alongside Artificial Intelligence. Unlike a traditional core, which is focused on the storage of accounting records, a bank operating system is focused on the execution of business logic and money movement. It serves as an innovation core that allows the bank to move fiat currency, tokenized deposits, and other digital assets across various networks from a single environment.

Six unified pillars form the foundation of a modern BankOS.

The first is Unified Banking, which uses a single modern ledger and a unified payments engine to handle both fiat and tokenized payments.

The second is Unified Experience, abstracting the complexity of underlying rails.

The third is Unified Payments, which consolidates ACH, Fedwire, RTP, FedNow, SWIFT, and Blockchain on one platform.

The fourth is Unified Operations, delivering a single view across channels, assets, and rails, with AI-driven reconciliation and compliance.

The fifth is Unified Integration, which is a layer that allows plug-and-play connectivity into any ecosystem.

Finally, Unified Intelligence provides predictive analytics and deep insights into customer behavior.

This architecture repositions the bank’s strategic control. Historically, innovation was gated by the release cycles of core vendors. Under a bank operating system model, the operating system becomes the control plane. This allows the bank to become an ecosystem participant rather than just a utility provider. It enables embedded banking and sponsor models through configuration instead of re-architecture. Transformation shifts from a high-risk infrastructure project to a revenue acceleration strategy.

The technical mechanics of the sidecar core

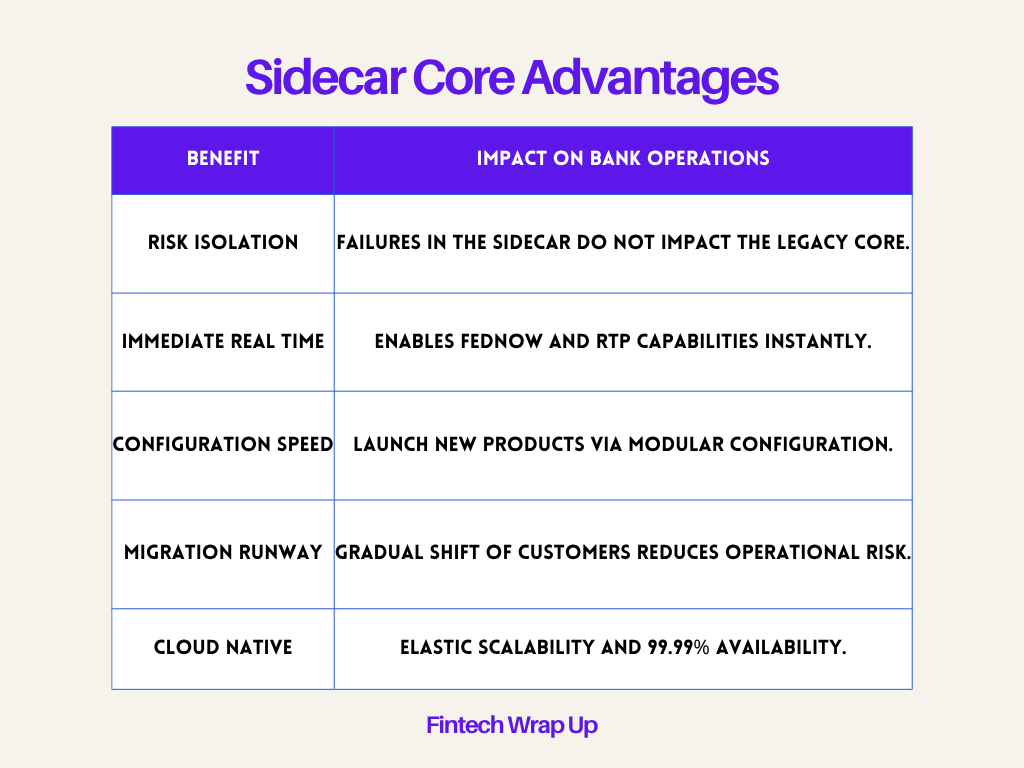

I am a proponent of the sidecar core strategy because it offers a low-risk path to modernization. A sidecar core is a separate, modern banking system that runs parallel to legacy infrastructure. It does not require a full replacement of the traditional core. Instead, it gradually takes over customer segments, products, or services, becoming the mainstream core and giving banks a clear exit from legacy systems. I have seen projections that 40% of global banks will pursue sidecar strategies by 2026, rising to 80% by 2028.

The technical architecture of a sidecar core, such as Finzly BankOS, relies on a smart next-gen parallel ledger. It connects to the legacy core and third-party systems using adapters and an extensive suite of APIs. I find that this approach allows for non-disruptive integration. The sidecar core handles the real-time demands of modern payments and deposits, while the legacy core continues to manage bulk operations for the existing customer base. This creates a migration runway where entire portfolios can shift naturally over months instead of years.

A sidecar core must be ISO 20022 native to be effective. ISO 20022 is the global messaging standard that enables data-rich transactions. Legacy cores typically rely on flat files and rigid schemas that truncate data. An ISO 20022 native bank operating system can ingest 24/7 transactions and overcome the batch constraints of the core. This is essential for participating in real-time networks like FedNow and RTP, which require millisecond journaling that old mainframes cannot achieve.

Real-time payments and the A2A imperative

I believe the proliferation of account-to-account payments and digital wallets is the most significant pressure vector forcing banks to adopt operating systems. Digital wallets are multiplying across geographies, and digital-first customers expect instant funds availability. Banks that cannot flexibly integrate A2A rails and wallet networks risk being disintermediated from payment flows they once controlled. Fragmented vendor stacks cannot keep pace with the velocity of this market.

A unified operating system allows a bank to activate new rails as configuration events. For example, a bank operating system can unify ACH, Fedwire, RTP, FedNow, SWIFT and even on-chain rails into a single payments processing platform. This provides total control and visibility across all processors from one API, one customer experience or one operational console. It eliminates the need for separate integrations for each payment type. This is critical for US instant payment rails like FedNow and RTP, which settle in real time 24/7. Legacy batch cores simply struggle to maintain balance accuracy in an always-on environment.

There is also a structural shift in how businesses manage liquidity. Digital adoption has increased the demand for real-time notifications and automated reconciliation. An operating system purpose-built for real-time operation enables continuous engagement and instant decision-making. This allows banks to compete with fintechs by offering instant payment confirmation and immediate settlement. Here, speed to value is a competitive metric that is now a balance sheet variable. The institutions that reduce time to market reduce their strategic risk.

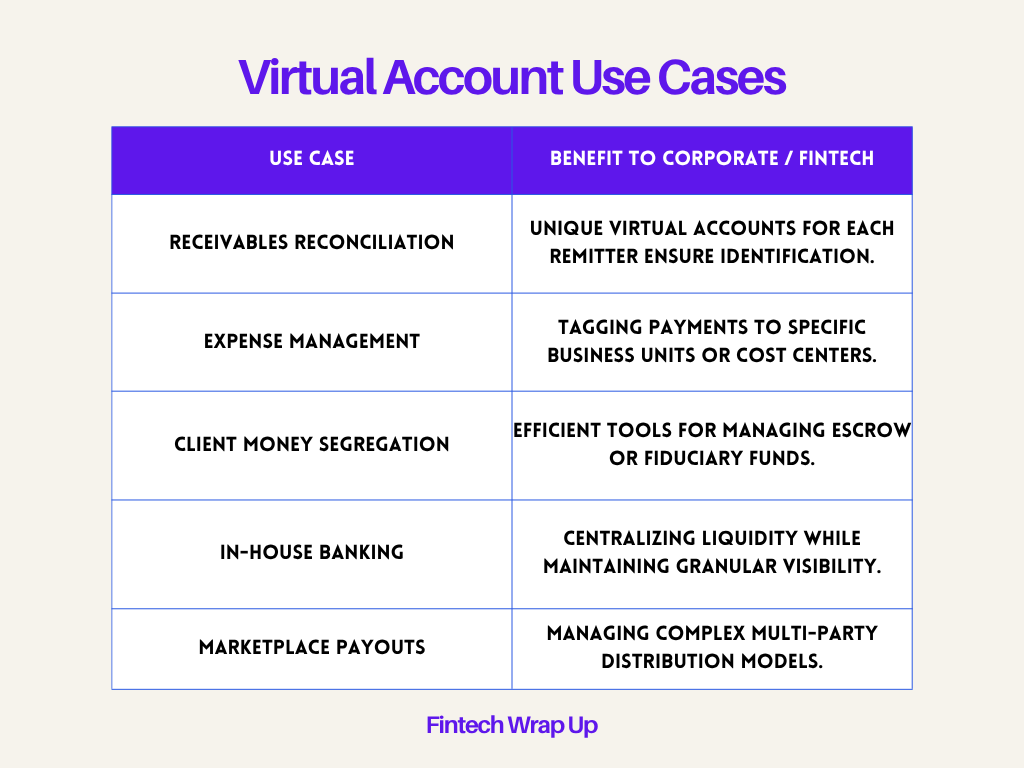

Virtual accounts and programmable liquidity

There is a clear demand for smarter, more flexible account structures. Modern financial ecosystems require virtual accounts layered over master accounts, multi-entity platform structures, and segmented balances for marketplaces. These are not edge cases; they are standard requirements for corporate clients today. The composable ledger on the bank operating system enables these programmable account hierarchies without forcing a core re-architecture. This unlocks new deposit models and monetizable partner offerings.

Technically, virtual accounts are non-real accounts used to redirect transactions to an underlying real account. They are off-balance sheet items from the bank’s perspective. I have seen how multiple virtual accounts can be mapped to a single real account to help a corporate client rationalize their cash positions. Composable virtual accounts support single-level or multi-level hierarchical structures. Transactions performed on any virtual account are automatically routed through the hierarchy in real time, while shadow entries are posted to the respective virtual accounts.

This structure is liberating for treasurers. It allows for the notional segregation of funds through shadow transaction postings, aiding in automated reconciliation. Corporations use these structures to mimic in-house banks or centralized payment factories. For banks, providing these capabilities through an operating system means they can onboard fintech partners at scale and manage complex ownership structures like escrow or IOLTA accounts without adding operational complexity to the legacy core.

The shift to agentic AI in banking

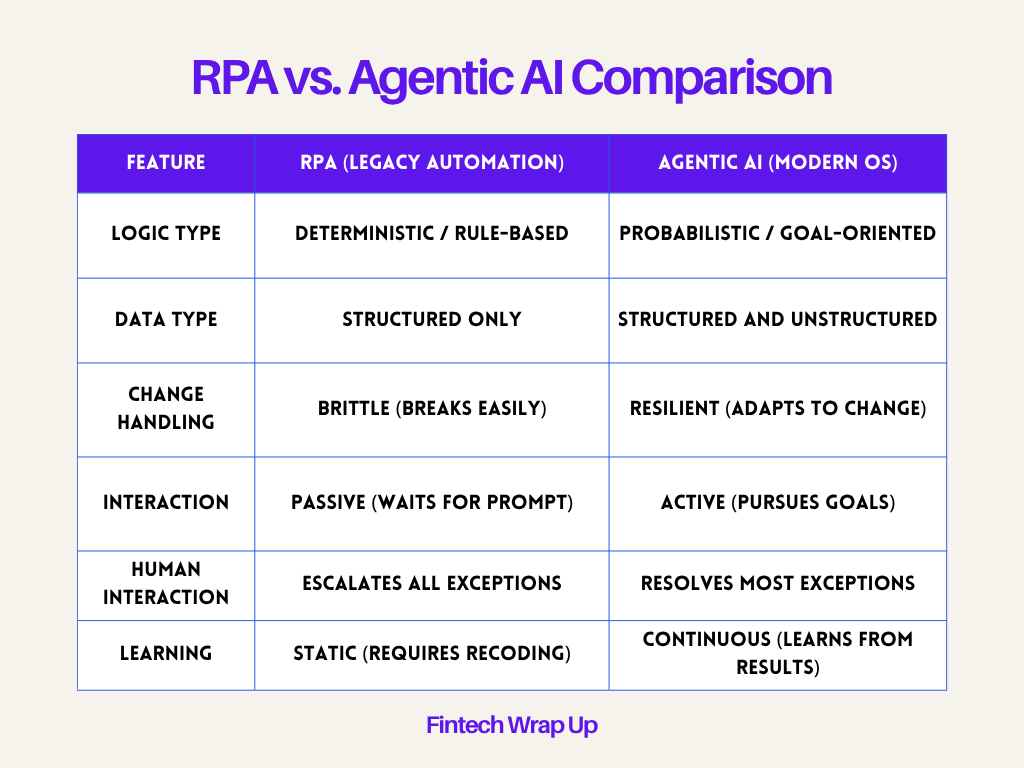

I want to distinguish between traditional automation and the new wave of Agentic AI. For years, banks have used Robotic Process Automation to handle repetitive, rule-based tasks. RPA is like an assembly line worker following exact instructions. It is deterministic and brittle. If a UI element moves or a label changes, the bot breaks. Agentic AI is fundamentally different. It is goal-driven and adaptive. It uses large language models and reasoning to pursue outcomes through strategic decision-making.

Unlike generative AI, which just creates content, Agentic AI takes action. I see agents that investigate transaction disputes, resolve exceptions autonomously, and coordinate multi-step workflows across disconnected systems - but always with human oversight to ensure safe decision-making in financial services. A modern operating system with agents can automate payment operations and compliance by embedding intelligence directly into the payment flow. For example, an AI agent can analyze a wire flag, pull context from account history and geographic data, and recommend a resolution in seconds.

I believe this shift from rule following to reasoning enables true end-to-end automation. AI agents do not break when vendor formats change or ERPs get upgraded. They adapt. Data suggests that AI agents can reduce operational costs by 30 to 40% by 2030. They free up human talent to focus on high-value advisory roles. In an operating system, the back office becomes a digital engine that supports efficiency and superior customer outcomes.

The tokenized economy

From my latest conversation, I am observing a significant strategic shift toward tokenized assets. The market for stablecoin issuance is projected to reach 1.9 trillion dollars by 2030. Banks face a choice: they can either participate in this ecosystem or watch as liquidity moves to fintech competitors. Tokenized deposits are digital representations of regulated bank liabilities that stay within the traditional banking system. Stablecoins, conversely, are typically issued by private entities and backed by reserves. Both are digital money tokens that operate on 24/7 rails with programmability.

A bank operating system provides the infrastructure to manage these assets without betting on a single blockchain. I see modules like Finzly’s Token Galaxy as a way to unify traditional and tokenized rails. This allows banks to move fiat, tokenized deposits, and stablecoins across networks through a multi-asset, multi-rail engine on the operating system, with operational oversight from a single dashboard. This interoperable infrastructure is essential for strategic freedom. It allows banks to connect to multiple blockchains and consortia simultaneously. It also enables advanced use cases like automatic payroll deposits into tokenized accounts.

The technical foundation of this tokenization layer must be robust. Multi-Party Computation secured wallets ensure enterprise-grade infrastructure with no single point of failure. Tokenized movements must meet the same rigorous KYC and AML standards as fiat systems. Composable workflows integrate compliance directly into event-driven, multi-asset money movement, providing real-time monitoring and a complete audit trail. This is a way for banks to retain deposits and prevent attrition to unregulated digital asset platforms.

Speed to value as a balance sheet variable

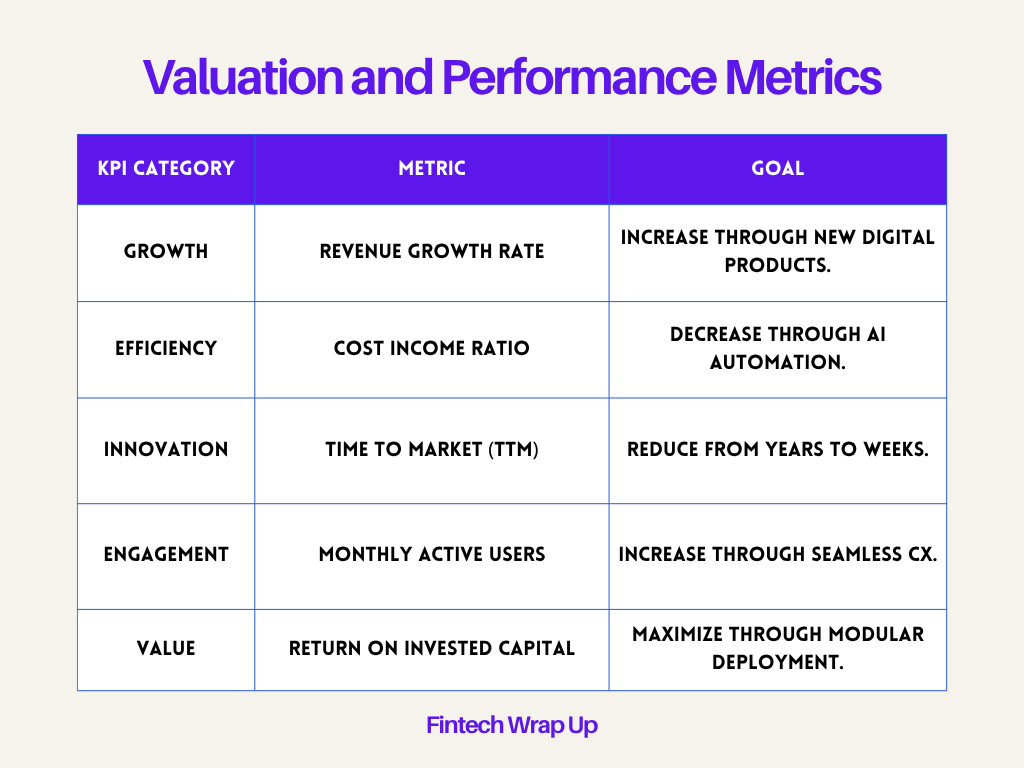

The primary metric for modern banking should be Speed to Value. Historically, banks have focused on Total Cost of Ownership, but this does not account for the opportunity cost of slow innovation. Speed to Value measures the velocity at which an institution can move from a business idea to revenue generation. In a dynamic market, the ability to launch a product in weeks rather than years is a significant competitive advantage. Cloud migration and low code adoption are key enablers of this velocity.

Modernizing infrastructure is no longer just about reducing IT costs; it is about revenue acceleration. The bank operating system model transforms the ROI calculations. Instead of multi-year infrastructure projects with uncertain outcomes, banks can deploy modular capabilities and measure immediate financial impact. For example, some institutions use sidecar cores to launch new digital channels and increase digital adoption by 80%. This is the ability to create capacity in previously constrained parts of the organization.

Also, Speed to Value has a direct impact on bank valuations. By improving EBITDA and increasing the growth multiple, digital transformation creates measurable enterprise value. Analysts are increasingly focusing on KPIs like customer acquisition cost, retention rate, and revenue growth rate. A bank operating system that enables rapid product iteration and superior customer experience directly influences these metrics. I believe the standard procurement and implementation cycle of 6 to 9 months is being replaced by a model that prioritizes iterative releases and continuous value realization.

The future of the bank operating system

I believe we are entering a phase where the core becomes invisible. In the future, the primary interface for both the bank and the customer will be the operating system. The modern bank operating system is evolving into a fully autonomous environment where AI agents handle the majority of operational tasks. This will lead to a touchless support model, still with human oversight, and fully automated customer data management. The competitive advantage will go to those who have the best data foundation and the most integrated systems.

The integration reality check is that while most firms have some digital adoption, few have full system integration. The firms with fully integrated systems report 10x better growth performance and ROI measured in weeks. The biggest barrier to AI effectiveness is fragmented data. The most successful firms focus on integration over addition. They connect their CRM with core banking, payments, and compliance tools to create a single source of truth. This is a foundational requirement for any bank that wants to survive the next decade.

I believe that the bank operating system is the structural shift that will define the next era of banking. It reframes modernization from a defensive move to an offensive revenue strategy. By decoupling the innovation cycle from the legacy core, banks can participate in the real-time, tokenized economy. Operating systems like Finzly BankOS are becoming the control plane for the future of finance, enabling banks to provide the personalized, instantaneous services that modern customers demand. The institutions that embrace this model will thrive; those that remain core-centric will obsolesce.

Sources:

BankOS Platform - Finzly, accessed April 5, 2026, https://finzly.com/platform/

How Banks Are Layering Modern Experiences on Top of Legacy Cores - Veriday, accessed April 5, 2026, https://veriday.com/modernizing-banking-experience-without-core-replacement/

Learn how progressive modernization enables banks to transform core systems without big bang risk. - Softjourn, accessed April 5, 2026, https://softjourn.com/insights/core-banking-modernization-in-5-steps

Balancing Cost and Risk with Growth and Revenue, accessed April 5, 2026, https://arizent.brightspotcdn.com/18/5b/080f452b482fa9a83fb774c2bde8/bank-modernization-ebook-v6.pdf

Legacy Banking Systems Explained: Why Modernization Matters - Archon Data Store, accessed April 5, 2026, https://www.archondatastore.com/blog/legacy-banking-system-modernization/

what is a modular bank? | Skaleet, accessed April 5, 2026, https://skaleet.com/en/blog/modular-bank-what-is-a-modular-bank

Banking Operating System: Core to Platform Guide - Backbase, accessed April 5, 2026, https://www.backbase.com/blog/banking-operating-system

Finzly BankOS.pdf

Tokenized Deposits & Stablecoins Platform for Banks | Finzly, accessed April 5, 2026, https://finzly.com/solutions/tokenized-deposits/

Finzly Unveils Token Galaxy: Unifying Money Movement for Traditional and Tokenized Banking - PR Newswire, accessed April 5, 2026, https://www.prnewswire.com/news-releases/finzly-unveils-token-galaxy-unifying-money-movement-for-traditional-and-tokenized-banking-302710960.html

Inside Finzly’s Vision: Rethinking Banking Infrastructure with AI and ..., accessed April 5, 2026, https://finzly.com/resources/blogs/inside-finzlys-vision-rethinking-banking-infrastructure-with-ai-and-tokenized-money/

Building on Bedrock: A Practical Guide to Core & Ledger Choices in Embedded Banking, accessed April 5, 2026, https://ingomoney.com/blogs/building-on-bedrock-a-practical-guide-to-core-ledger-choices-in-embedded-banking/

Sustainable Scaling: Why Modularity Makes Sense for LatAm Banks in 2026, accessed April 5, 2026, https://www.galileo-ft.com/blog/sustainable-scaling-why-modularity-makes-sense-for-latam-banks/

Stablecoins: Exploring the Future of Cross-Border Payments - Finzly, accessed April 5, 2026, https://finzly.com/resources/blogs/stablecoins-exploring-the-future-of-cross-border-payments/

Finzly India R&D is hiring Fullstack Developer job in Pune, Chennai | Cutshort, accessed April 5, 2026, https://cutshort.io/job/Fullstack-Developer-Pune-Chennai-Finzly-India-RD-LNmjTUP3

Low-code platforms deliver high rewards - KPMG International, accessed April 5, 2026, https://kpmg.com/pt/en/insights/2023/06/low-code-platforms-deliver-high-rewards.html

Accelerate Your Cloud Journey with Altimetrik, accessed April 5, 2026, https://www.altimetrik.com/blog/ai-first-cloud-journey-acceleration/

Virtual Accounts - Enabling lean treasuries - Whitepaper | Oracle, accessed April 5, 2026, https://www.oracle.com/a/ocom/docs/industries/financial-services/fs-vam-enabling-lean-treasuries-wp.pdf

Empowering Banks With Virtual Ledgers - Datos Insights, accessed April 5, 2026, https://datos-insights.com/reports/empowering-banks-with-virtual-ledgers/

Agentic AI vs RPA: Practical Differences, Real Use Cases, and How to Combine Them, accessed April 5, 2026, https://www.mywave.ai/blog/agentic-ai-vs-rpa

RPA vs. AI Agents for Accounting: Which is Better for Modern Finance Teams?, accessed April 5, 2026, https://blog.auditoria.ai/rpa-vs-ai-agents-for-accounting-finance

AI agents versus RPA: A guide for accountants - Thomson Reuters, accessed April 5, 2026, https://tax.thomsonreuters.com/blog/ai-agents-versus-rpa-a-guide-for-accountants-tri/

7 Use Cases For Agentic AI in Banking - Druid AI, accessed April 5, 2026, https://www.druidai.com/blog/7-use-cases-for-agentic-ai-in-banking

Finzly Announces Agentic AI-Powered Payments and Operations, accessed April 5, 2026, https://finzly.com/resources/press-releases/finzly-announces-agentic-ai-powered-payments-and-operations/

How Retail Banks Can Put Agentic AI to Work | BCG, accessed April 5, 2026, https://www.bcg.com/publications/2026/how-retail-banks-can-put-agentic-ai-to-work

How is Agentic AI different from RPA? - AutomationEdge, accessed April 5, 2026, https://automationedge.com/blogs/how-is-agentic-ai-different-from-rpa/

Tokenized Deposits vs. Stablecoins: A Practical Guide for Financial Institutions | Stablecore Blog, accessed April 5, 2026, https://stablecore.com/blog/tokenized-deposits-vs-stablecoins-a-practical-guide-for-financial-institutions

Stablecoins and tokenized deposits are poised to reshape global finance | Deloitte Canada, accessed April 5, 2026, https://www.deloitte.com/ca/en/Industries/financial-services/perspectives/tokenized-money-stablecoins.html

contest between central bank digital currencies, stablecoins, and tokenized deposits: Which will likely win, and why? | Capital Markets Law Journal | Oxford Academic, accessed April 5, 2026, https://academic.oup.com/cmlj/article/21/2/kmag012/8571935

Finzly Unveils Token Galaxy: Unifying Money Movement for Traditional and Tokenized Banking, accessed April 5, 2026, https://finzly.com/resources/press-releases/finzly-unveils-token-galaxy-unifying-money-movement-for-traditional-and-tokenized-banking/

Tech implementation sets your speed to value | Grant Thornton, accessed April 5, 2026, https://www.grantthornton.com/insights/articles/advisory/2024/tech-implementation-sets-your-speed-to-value

KPMG Elevate - Value Creation, accessed April 5, 2026, https://kpmg.com/cn/en/services/advisory/value-creation.html

Best financial services software for banks of March 2026 - FitGap, accessed April 5, 2026, https://us.fitgap.com/search/financial-services-software/banks

Commercial banking platforms for SMBs & mid-market 2024 - Backbase, accessed April 5, 2026, https://www.backbase.com/blog/top-commercial-banking-platform-providers

Modernizing the Banking Ledger: Powering Smarter Core Banking - Vacuumlabs, accessed April 5, 2026, https://vacuumlabs.com/articles/banking-ledger/

Top AI-native banking platform providers in 2026: a buyer’s guide - Backbase, accessed April 5, 2026, https://www.backbase.com/blog/top-ai-native-banking-platform-providers

Core Banking Platforms Compared: Features, Pricing, and Integration Ease | Gemba, accessed April 5, 2026, https://ge.mba/research/core-banking-platforms-compared-features-pricing-and-integration-ease

Agentic AI Integration: Business Process Automation Guide - Informatica, accessed April 5, 2026, https://www.informatica.com/resources/articles/agentic-ai-integration.html

HubSpot Asia Pacific | Singapore Finance Firms: Why Only 30% See ROI in Weeks From Digital Transformation, accessed April 5, 2026, https://www.hubspot.com/apac/newsroom/blog-singapore-financial-services-roi

Disclaimer:

Fintech Wrap Up aggregates publicly available information for informational purposes only. Portions of the content may be reproduced verbatim from the original source, and full credit is provided with a “Source: [Name]” attribution. All copyrights and trademarks remain the property of their respective owners. Fintech Wrap Up does not guarantee the accuracy, completeness, or reliability of the aggregated content; these are the responsibility of the original source providers. Links to the original sources may not always be included. For questions or concerns, please contact us at sam.boboev@fintechwrapup.com.

Strong take on how the “Bank Operating System” is shifting control from legacy cores to real-time orchestration. The point on speed to value impacting revenue is spot on.

We’re also seeing multi-rail orchestration via a single API layer, plus growing adoption of virtual IBANs and programmable wallets for cross-border use cases. Tokenized deposits and stablecoins are clearly pushing banks toward hybrid infrastructures.

Curious do you see BankOS evolving more as an internal control plane or an external embedded finance platform?

Open to connect if you’re exploring collaboration or want to exchange insights.

banks fighting to modernize their core when they should be building around it instead. really thorough breakdown.