Deep Dive: Open Banking Implementation Demystified

In this week’s deep dive edition of Fintech Wrap Up, we’re unraveling the complexities of Open Banking—what it is, how it’s transforming financial services, and why it’s a game-changer

TL;DR:

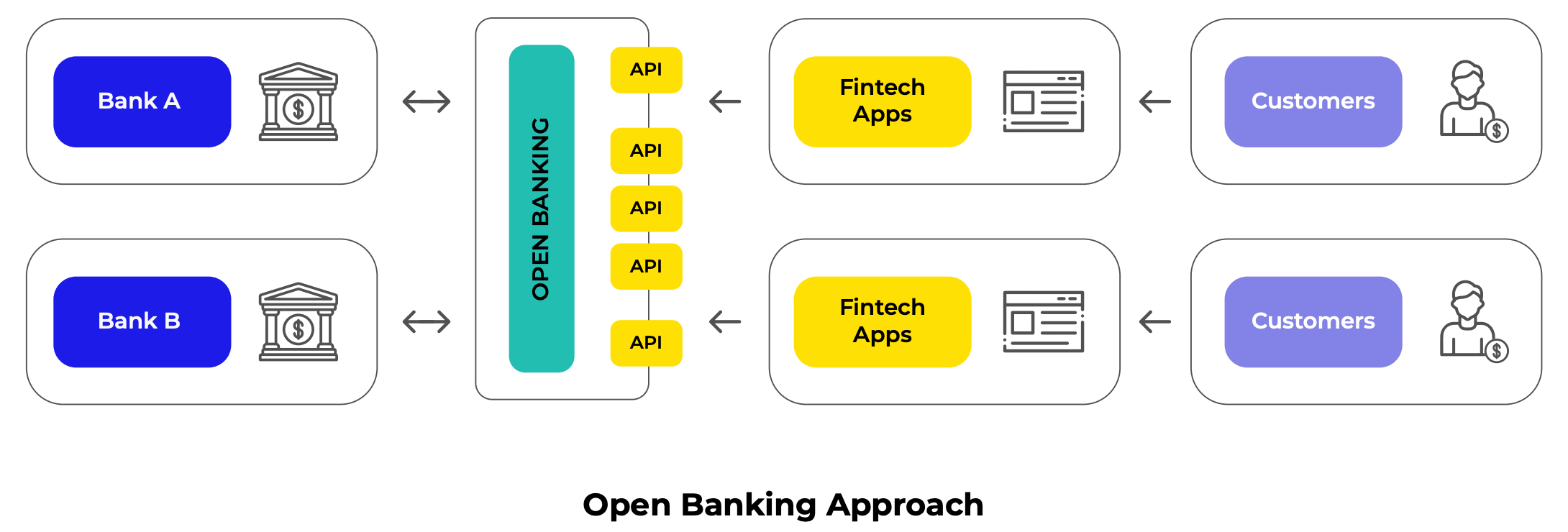

In this week’s deep dive edition of Fintech Wrap Up, we’re unraveling the complexities of Open Banking—what it is, and how it’s transforming financial services based on Blac Labs’s experience. Open Banking is essentially the evolution of API-based integrations, allowing fintechs and banks to securely exchange data and create innovative financial products. Unlike the old-school method of screen scraping (which came with serious security risks), Open Banking leverages regulated APIs, giving consumers more control over their financial data while enabling banks to offer smarter, more seamless services.

For consumers, this means easier account aggregation, better personal finance management, instant credit assessments, and even streamlined tax preparation. But it’s not just about convenience—banks also stand to benefit, gaining deeper insights into customer behavior and unlocking new revenue streams. However, implementing Open Banking isn’t as simple as flipping a switch. Banks need to adhere to strict API standards (like those from the Financial Data Exchange), overhaul their technical architecture, and prioritize security at every level.

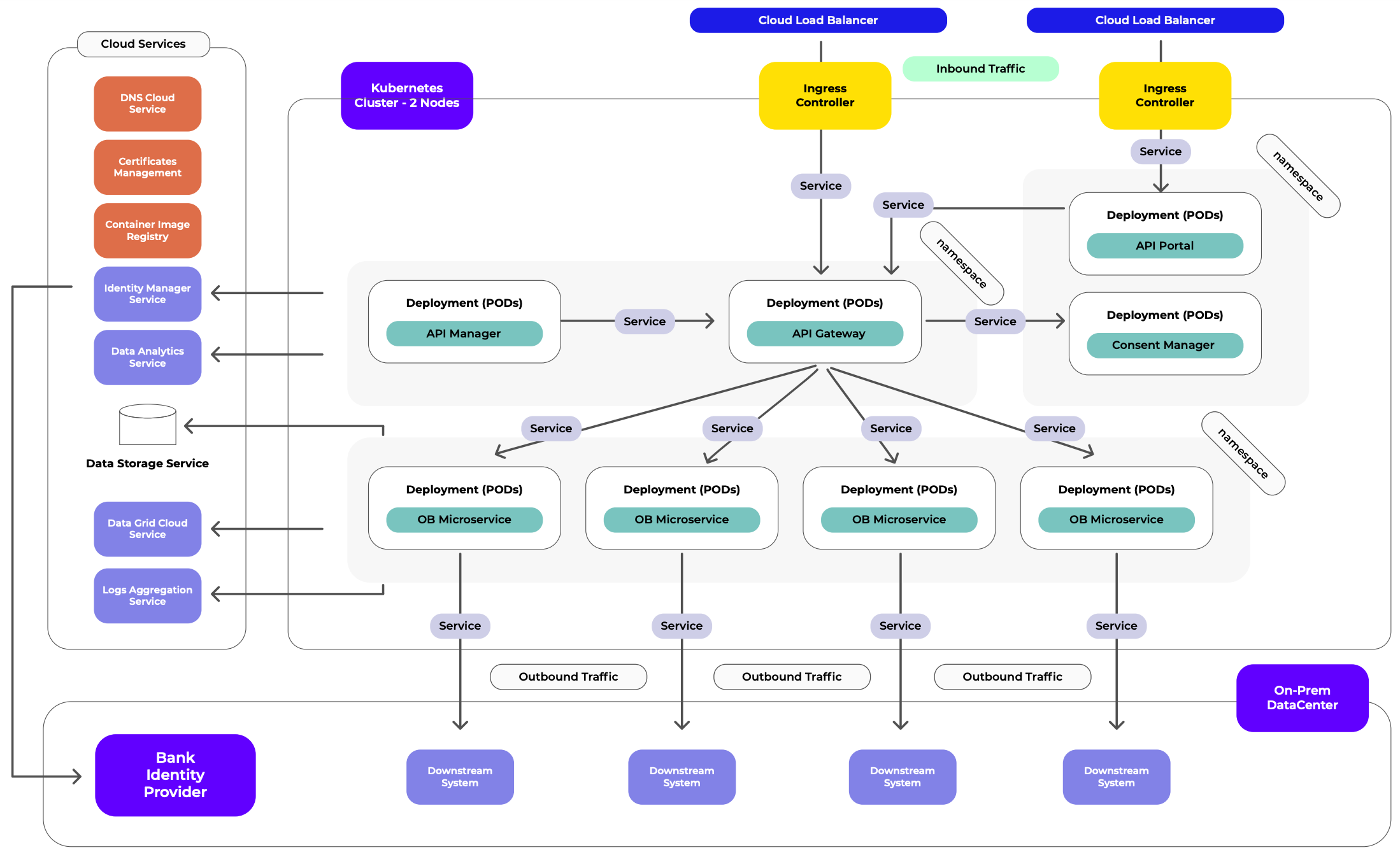

We also break down the core building blocks of Open Banking infrastructure, from API gateways and identity management to cloud infrastructure and microservices. Plus, we share best practices for fintechs and financial institutions looking to build Open Banking solutions—things like leveraging existing platforms, automating security scans, and ensuring architecture flexibility.

Open Banking is here to stay, and it’s reshaping how we interact with financial services. If you’re in fintech, payments, or banking, now’s the time to pay attention. Let’s dive in!

What is Open Banking?

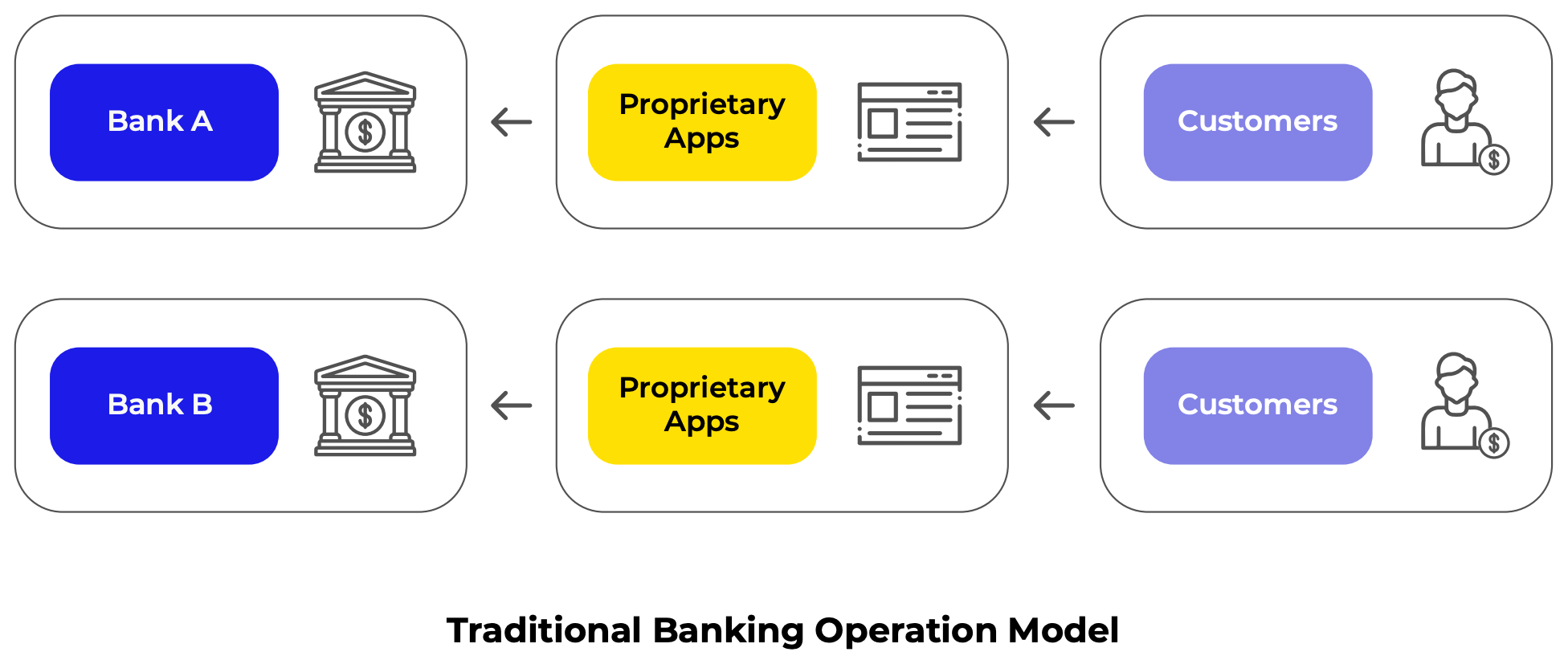

Traditional Banking Operation Model 04 Open Banking meets the modern demands of financial technology by unifying technical infrastructure and regulatory standards. It facilitates an innovative landscape for fintech companies to provide exciting new products that satisfy consumer needs. All these new products and services are exposed through API ecosystems, allowing third parties to integrate and provide a better customer experience. Simply put, Open Banking is “the evolution of the kind of API-based integrations that organizations have been building for decades.”

Traditional banking systems lack the capacity to provide users with holistic insight into their financial products across different banks, resulting in issues and complications when customers try to make informed decisions. In this digital age, it is increasingly important for banks to offer solutions which break down data silos and give an overview of a customer’s full financial profile.

With an emphasis on customer data centricity, financial institutions are seeing the benefit of offering customers the flexibility to securely move their information from one institution to another. This will ultimately give customers better control over their financial data. For FinTechs and banks, it will mean new financial products and opportunities for revenue generation.

While Open Banking presents new opportunities for Fintechs and financial institutions, it is not the first mechanism that the financial industry has put in place to extract or fetch financial information to be used by third party apps (TPPs). For many years, TPPs have been developing applications that rely on a technique called screen scraping—a problematic and potentially risky way to extract data.

Keep reading with a 7-day free trial

Subscribe to Fintech Wrap Up to keep reading this post and get 7 days of free access to the full post archives.