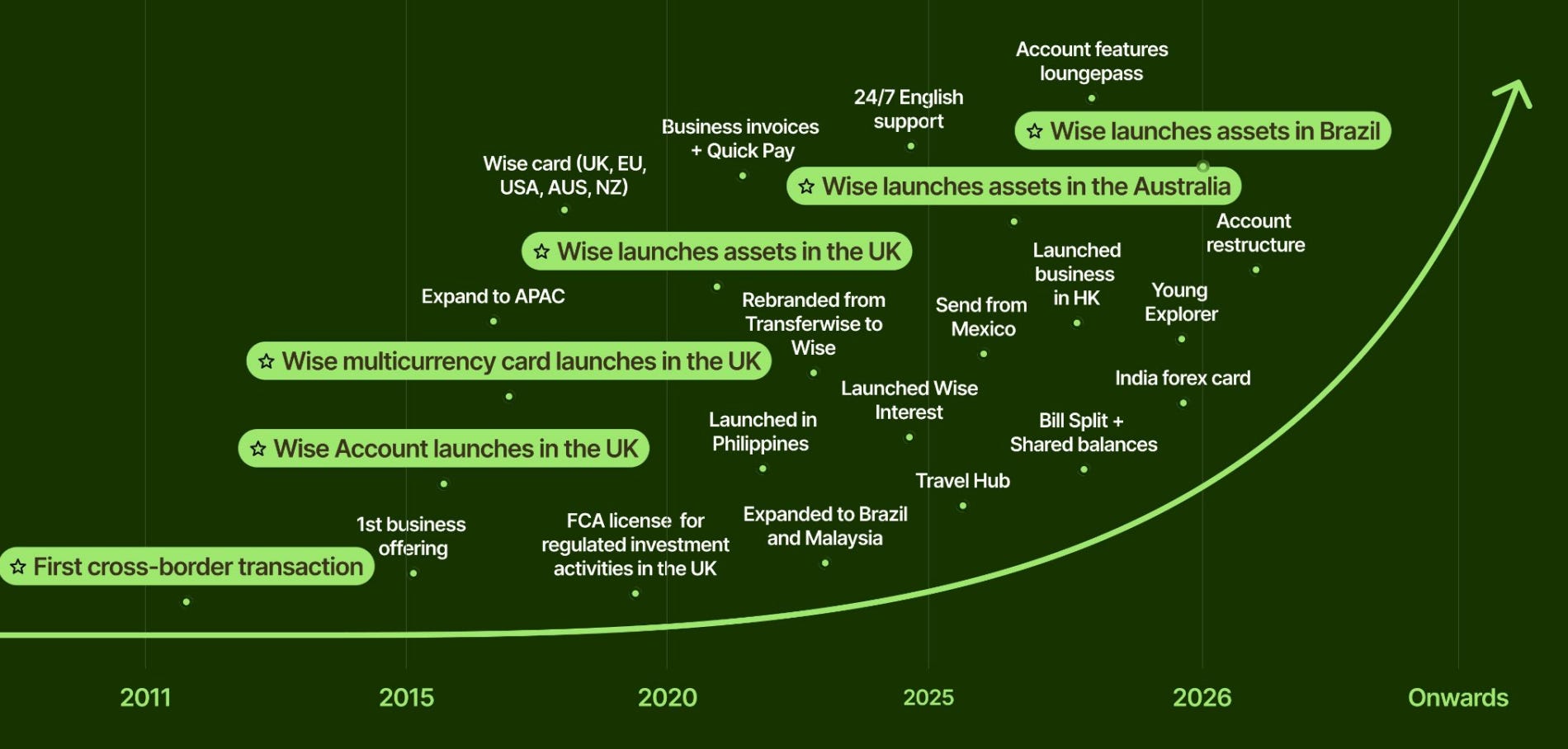

Deep Dive: Inside Wise’s Products, Licenses, Rails, and the Technology Stack

On May 11, 2026, Wise began trading on Nasdaq under the ticker WSE, a dual listing alongside its existing London Stock Exchange presence. The moment was symbolic. Wise isn’t just adding liquidity or broadening its investor base. The Nasdaq move signals something more deliberate: Wise is reframing itself not as a consumer fintech, but as financial infrastructure, the kind institutions and regulators think about differently than apps.

To understand why that framing matters, you have to understand what Wise has actually built over fifteen years, and where it’s now pointing that infrastructure.

The problem was never just fees

The conventional story about Wise is that it solved a pricing problem that it showed up, exposed the hidden FX markups banks were charging, and gave consumers a fair rate. That story is true, but it undersells what they actually did.

Traditional cross-border payments run on correspondent banking. When money moves from Australia to the US, it typically hops through two or three intermediary banks each converting currencies, each taking a cut. The sender faces an upfront fee, then pays again through FX markups at each conversion, often without seeing the full cost until it’s done. The result: roughly 3.5% in fees, and 2–5 business days in wait time.

Wise replaced that chain. Instead of routing money through Singapore and Hong Kong and then New York, it created a model where value is moved locally in each jurisdiction and netted internally. A sender in Australia puts money in; Wise pays out from its local holdings in the destination country. No international wire. No correspondent bank taking a margin.

This is harder than it sounds, and it’s the reason no one had done it cleanly before.

To execute that model globally requires three things that compound in difficulty: regulatory licenses to operate in each market, direct connections to local payment systems, and technology that can coordinate it all in real time. Wise now holds 80+ licenses across the globe, has direct participations in 8 domestic payment systems (UK Faster Payments, EU SEPA, Brazil Pix, Singapore FAST, Australia’s NPP, Hungary’s RPS, Japan’s Zengin, and the Philippines’ InstaPay), and runs a single global technology stack maintained by over 1,000 engineers across 20+ service locations.

The outcome: 75% of transfers delivered in under 20 seconds. An average take rate of just 52 basis points. 4.7 million transactions per day. 99.9%+ uptime. Those numbers are not marketing. They are the operating benchmarks of a payments network that has spent 15 years becoming structurally cheaper to run than the system it replaced.

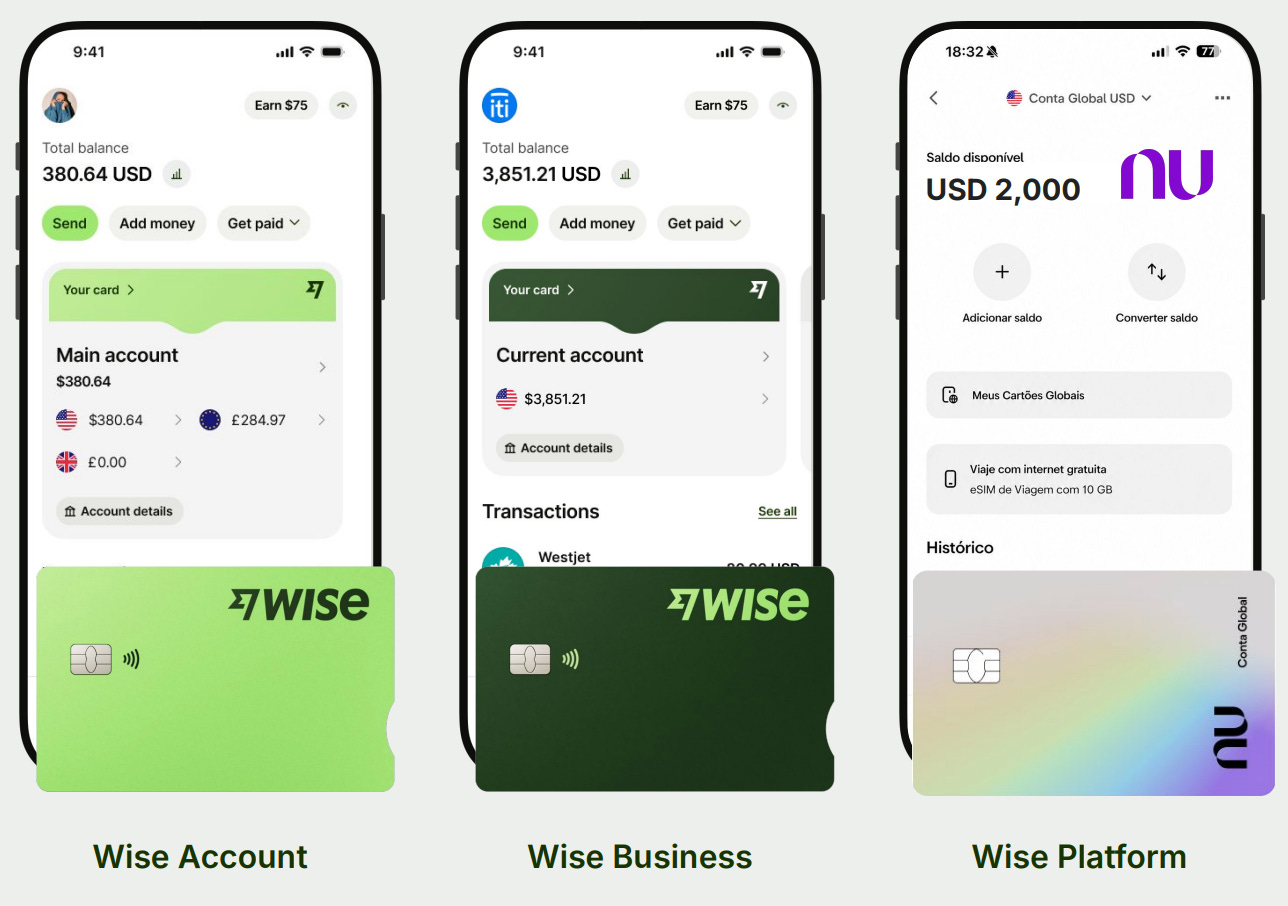

The three-product stack

Wise’s commercial surface area breaks into three products, each targeting a different customer tier while drawing from the same underlying infrastructure.

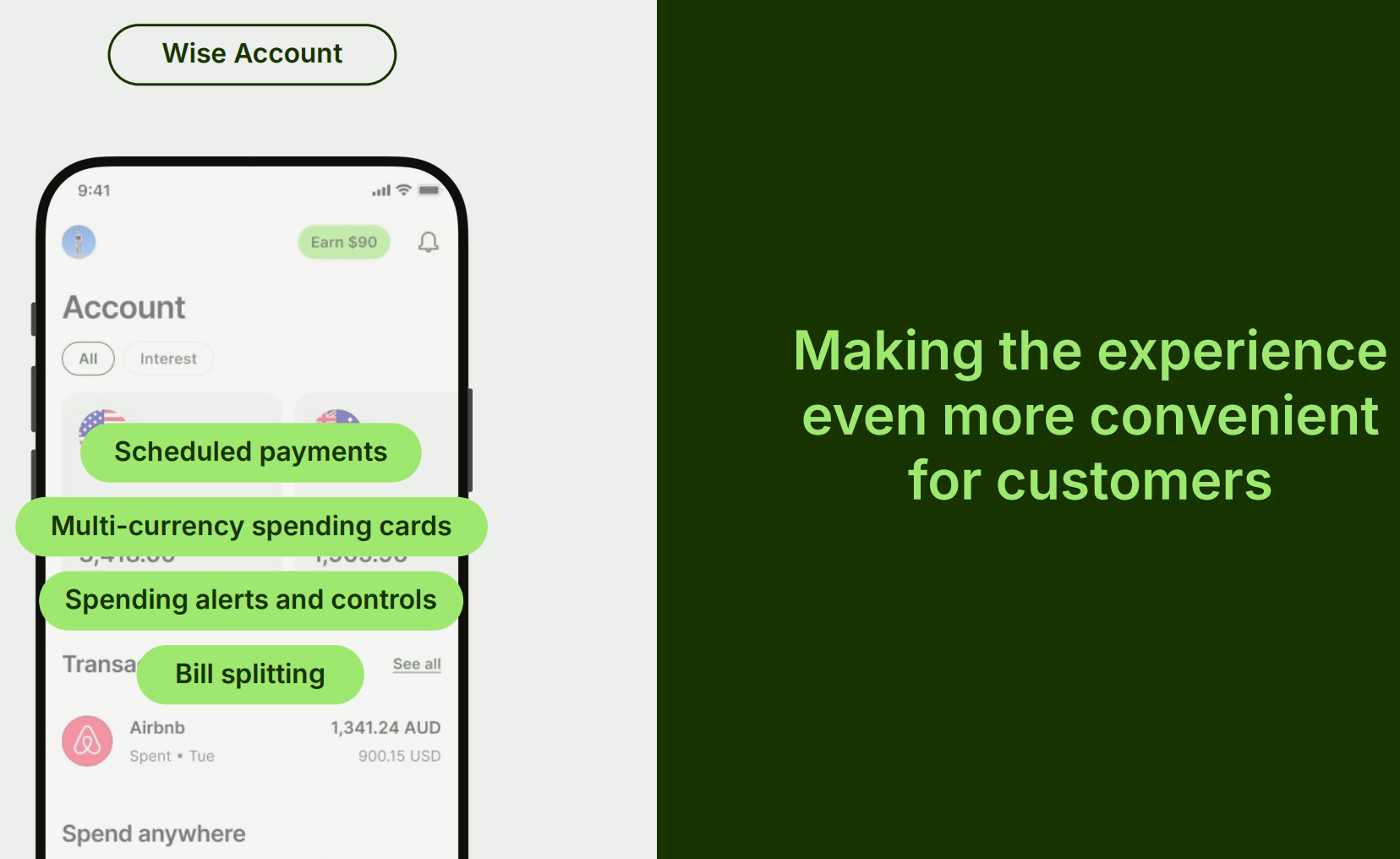

Wise account

The consumer product a multi-currency wallet that lets individuals hold 40+ currencies, send internationally at the mid-market rate, spend via a debit card, and earn yield through Wise Assets (money market funds and stock exposure). The newly launched UK current account integrates all of this and offers a yield of 3.26% on everyday balances versus 0% at most UK high street banks. The strategic intent is to make Wise the primary financial home for the globally mobile: travelers, digital nomads, expats, freelancers, remote workers. About 70% of customer growth comes from word of mouth

.

Keep reading with a 7-day free trial

Subscribe to Fintech Wrap Up to keep reading this post and get 7 days of free access to the full post archives.