Deep Dive: How to Add Data Intelligence to a Multi-PSP Payment Stack

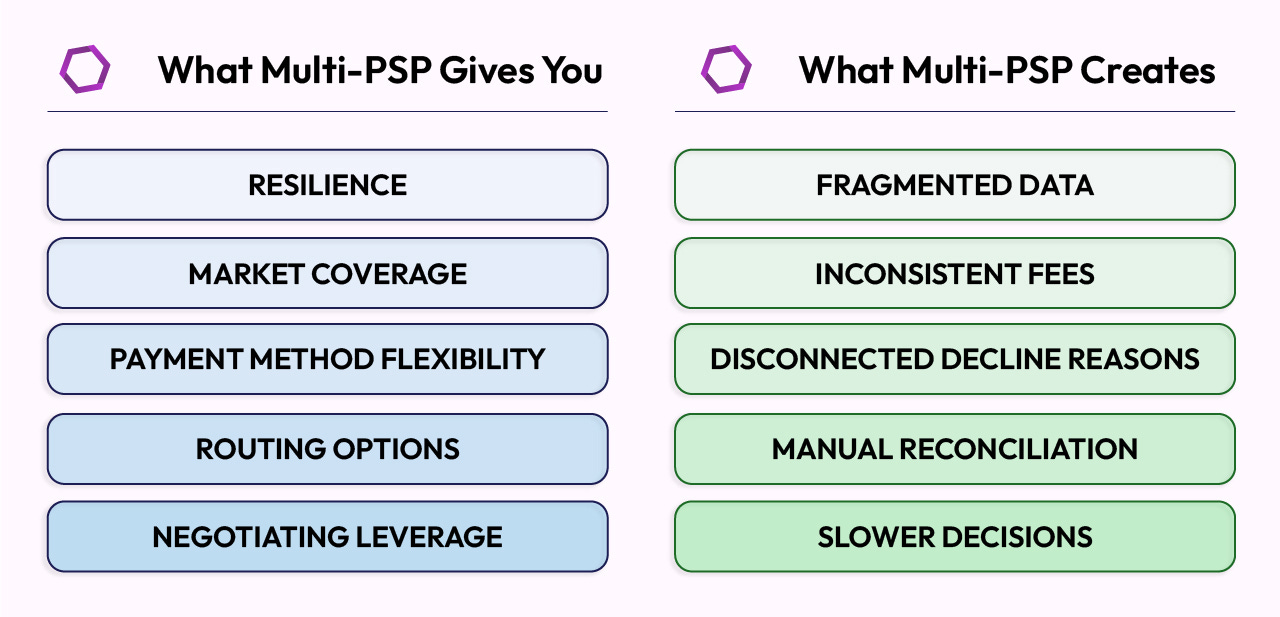

For the past decade, the global e-commerce and fintech sectors have operated under a singular directive: maximize payment optionality. Merchants have been instructed to expand their payment stacks by integrating multiple Payment Service Providers (PSPs), deploying redundant local acquirers, supporting diverse regional payment methods, and configuring dynamic routing paths. On the surface, this architecture of optionality has delivered significant operational value. It provides structural resilience against single-point-of-failure gateway downtime, secures broader geographic coverage across emerging markets, and optimizes baseline transaction approval rates.

However, this diversified payment stack introduces a major operational challenge: the fragmentation of transactional data. When an enterprise expands its processor footprint, it inevitably decentralizes its reporting architecture. Each integrated provider operates within its own closed ecosystem, generating isolated telemetry data characterized by proprietary APIs, unique database schemas, non-standardized decline reason codes, and distinct monthly settlement formats. Attempting to consolidate these disparate data streams into a single source of truth requires significant data engineering effort and often obscures clear data lineage and transformation logic.

This is the multi-PSP paradox: while adding payment gateways increases processing flexibility, it simultaneously degrades transaction visibility. In a multi-PSP environment, payment, finance, risk, and data teams must spend significant time and capital trying to reconcile inconsistent reporting formats manually. Without a unified mechanism to harmonize these data streams, merchants struggle to identify systemic processing errors, leaving them exposed to hidden margin erosion, elevated transaction costs, and transaction routing inefficiencies.

The scale of modern payment infrastructure highlights the necessity of resolving this paradox. Enterprise payment platforms, such as IXOPAY, orchestrated over $171 billion in transaction volume in 2025 alone, analyzing more than 850 million payment events using advanced machine learning models. Managing transactions at this scale requires a transition from basic payment routing to automated, centralized payments intelligence.

Deconstructing the technical gaps of decentralized stacks

The core issue of data fragmentation across a multi-PSP stack lies in how financial data is structured. When a merchant initiates direct integrations with independent processors, they ingest non-standardized raw telemetry streams. Each provider translates transaction events into its own schema, meaning a single decline event or settlement fee is classified differently depending on the gateway used. The resulting visibility gaps impact performance across several operational areas:

1. Authorization and Decline Telemetry

When transaction authorization rates fall, pinpointing the cause is difficult without unified data. A decline may stem from an issuer-side issue, a gateway timeout, an authentication failure within the 3D Secure (3DS) flow, or a misconfigured fraud ruleset.

Because different gateways categorize error codes differently (for example, one provider might label a transaction as a generic gateway error while another classifies it as an issuer-side card decline), payment operations teams often struggle to isolate the root cause. This classification mismatch leads to delayed troubleshooting and prolonged checkout abandonment.

2. Interchange, Scheme, and Acquirer Fee Complexity

To evaluate processing costs, merchants must track several distinct fee components: network interchange rates, scheme fees, gateway transaction charges, acquirer markup margins, and cross-border currency conversion (FX) rates.

These fees are often buried inside complex, inconsistent monthly settlement reports. Without a unified mechanism to normalize these variables across providers, merchants cannot easily determine their total cost of acceptance (TC A) at a transaction level.

To evaluate these costs systematically, the total cost of acceptance across N transaction events and M active processors can be modeled mathematically as:

where Ii is the variable interchange fee rate, Si is the card scheme fee rate, Mi is the acquirer markup, Gi is the gateway fee for transaction i, Vi represents the individual transaction volume, and Ffixed,j represents fixed monthly recurring fees across the active providers.

In a fragmented data environment, calculating this metric becomes highly inefficient, masking cost spikes and preventing data-driven provider negotiations.

3. Retry Mechanisms and Involuntary Churn

For subscription and recurring billing businesses, transaction recovery is critical to protecting revenue. When an initial subscription payment fails, merchants use automated retry chains to recover the transaction.

However, if these retry cascades are executed across multiple processors without a centralized tracking system, merchants cannot identify which retry chains successfully recover customer accounts and which simply generate redundant processing fees. This lack of coordinate-level tracking turns a recovery tool into an unexpected cost driver.

4. Fraud Risk, Disputes, and Network Compliance

Siloed fraud and risk monitoring systems make it difficult to detect emerging attack patterns. Indicators like first and second chargebacks, dispute win rates, and Visa Abuse Prevention Program (VAMP) exposure ratios are often tracked independently across distinct provider portals.

Consequently, risk teams struggle to build a unified view of fraud trends, delaying their response to vulnerabilities until after significant losses have occurred.

5. Post-Processing, Reconciliation, and Settlement Overhead

Because different payment methods generate data at varying frequencies and in different formats, manual financial reconciliation becomes a major operational bottleneck.

Finance and accounting teams are forced to manually cross-check transaction records with raw bank statements and gateway invoices to identify processing discrepancies, rounding errors, and unexpected conversion fees. This manual overhead consumes significant developer time and operational resources.

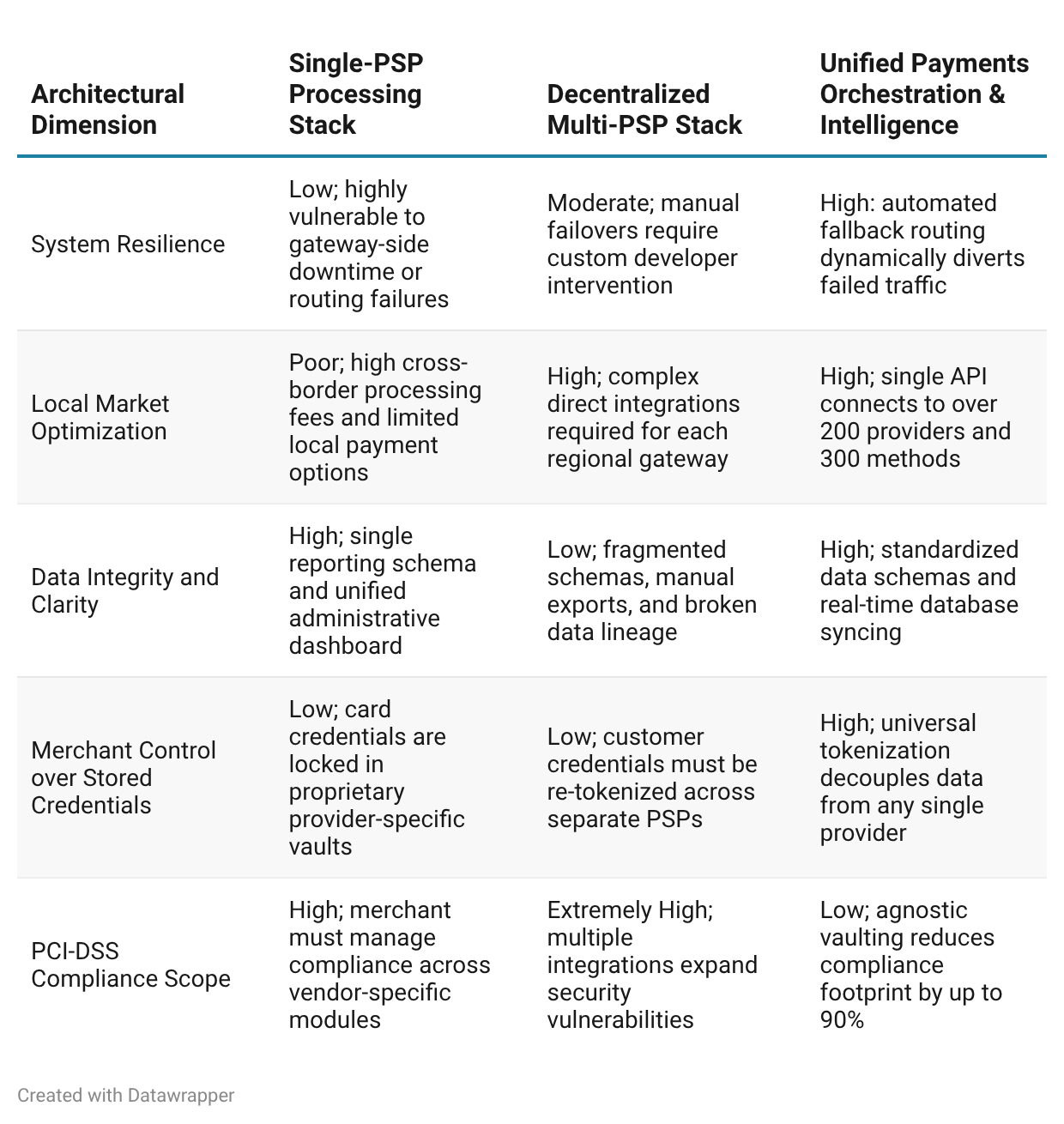

The limits of static gateway interfaces and internal BI engineering

To resolve these fragmentation issues, many organizations attempt to build custom payment dashboards using standard business intelligence (BI) systems. However, traditional BI systems and standard gateway interfaces have notable limitations.

Gateway-provided dashboards only display transactional activity within their own environment. They do not support multi-PSP data aggregation, automated anomaly detection, or direct API integration with external risk tools.

While in-house BI tools (such as Tableau, Looker, or Power BI) can ingest data from multiple sources, they lack native support for payment-specific schemas. They do not naturally parse complex transaction attributes like card BIN ranges, decline reason distributions, or Durbin-regulated transaction statuses.

Consequently, building and maintaining custom internal ETL (Extract, Transform, Load) pipelines to normalize payments data requires continuous engineering effort. Every time an integrated PSP updates its API version, changes its settlement file layout, or modifies a decline code, the internal data pipeline breaks.

This continuous maintenance diverts engineering resources away from the core product. Ultimately, manual database tracking remains retrospective. It tells the organization what failed yesterday, but it cannot actively identify or resolve processing errors as they occur.

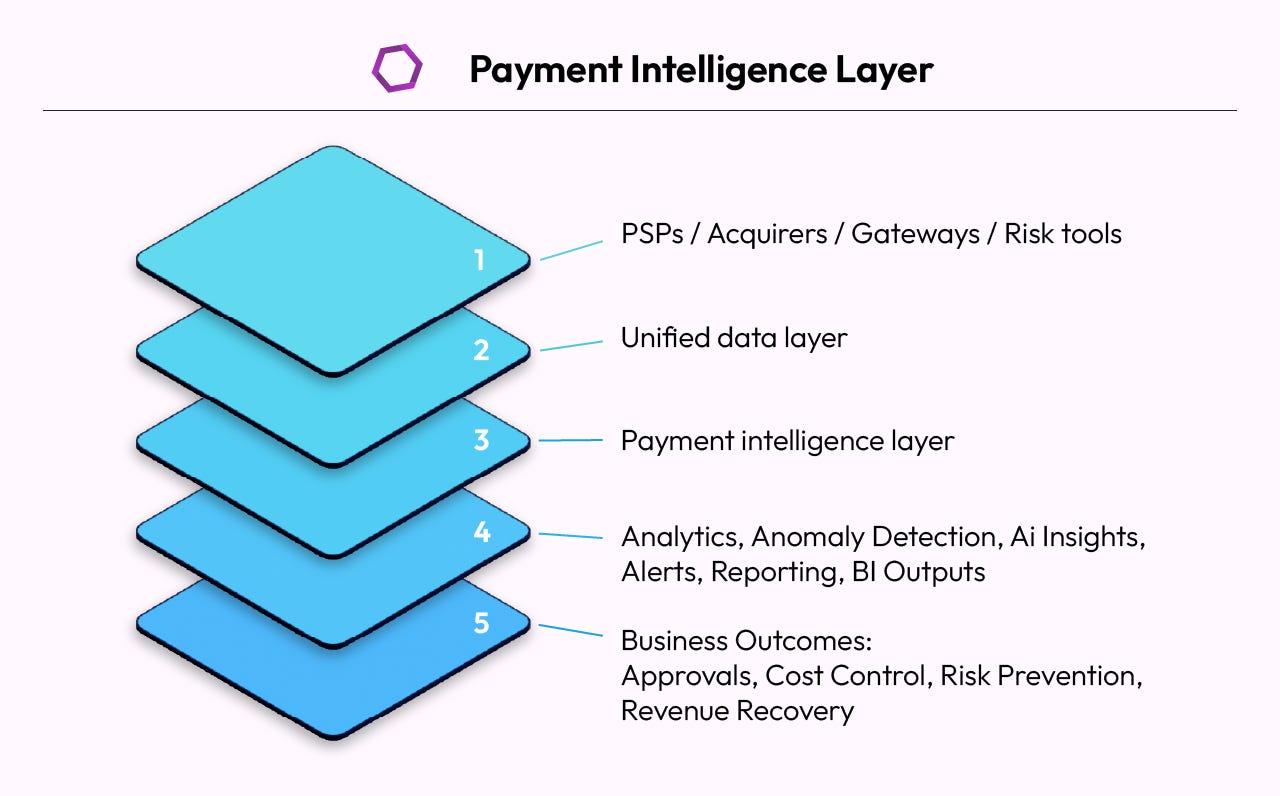

Designing a unified payments intelligence layer

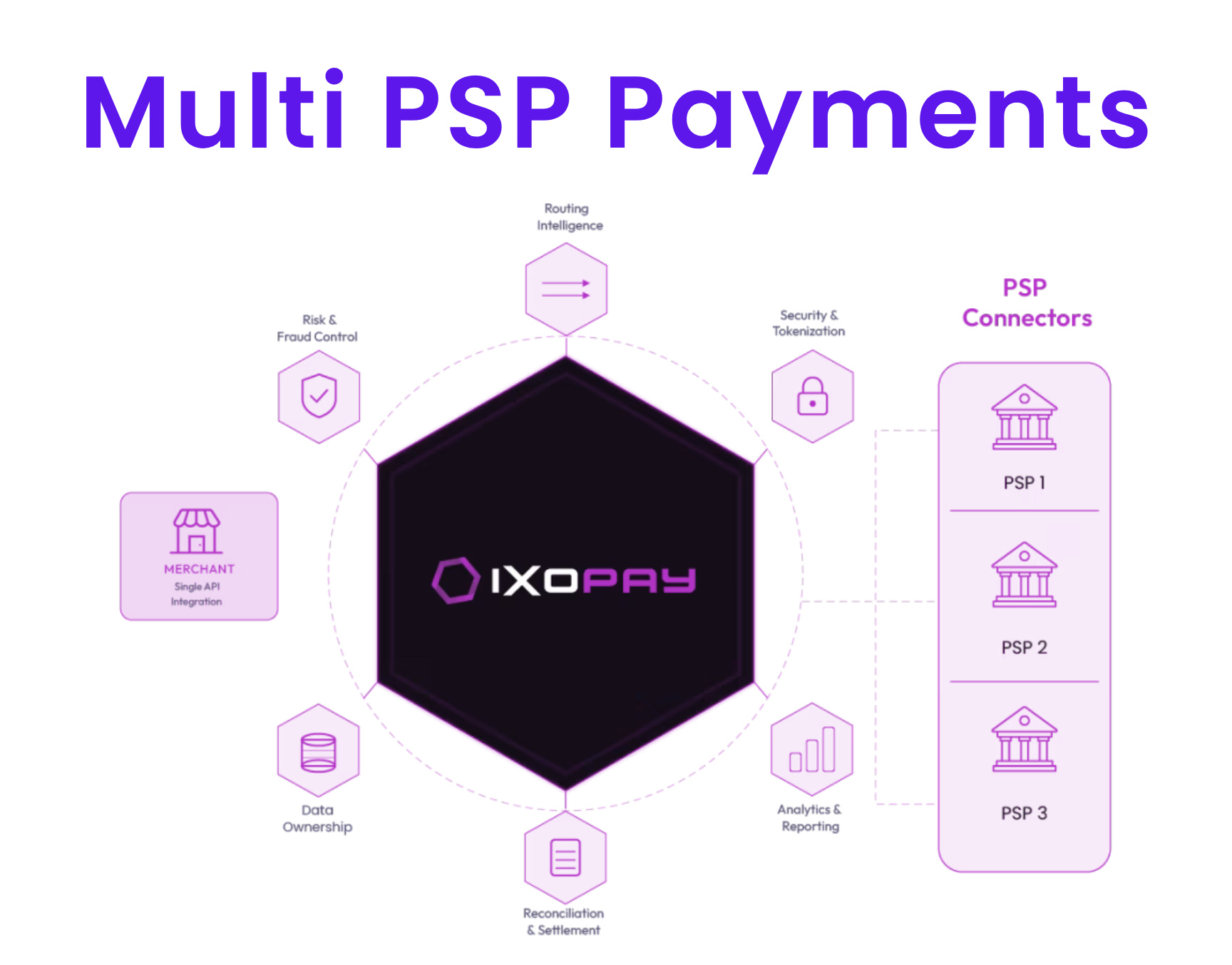

To bridge the gap between fragmented transaction data and actionable operations, payment architectures require a dedicated payments intelligence layer. Slipped between the payment routing engine and downstream analytical applications, this layer acts as an automated control center. It ingests raw transaction metadata, normalizes it into a consistent schema, and applies machine learning models to optimize processing decisions in real time.

According to the design principles defined by IXOPAY, a modern payments intelligence infrastructure is built around five core functional pillars:

1. Payments Analytics and Multi-PSP Normalization

The foundation of a payments intelligence strategy is the consolidation of scattered data points from gateways, acquirers, internal databases, and fraud engines into a single analytical environment.

This platform allows operations teams to slice performance metrics across multiple dimensions, including specific gateway accounts, card brands, BIN countries, and merchant identification numbers (MIDs) to track exactly how every transaction performs across different processing paths.

2. Conversational AI and Natural-Language Diagnostics (IXONav)

To reduce reliance on manual database queries, payments intelligence platforms integrate conversational AI assistants. For instance, IXOPAY’s IXONav functions as an automated payment analyst.

Using natural language, teams can query their transaction data directly (such as asking: “Did decline rates spike in the last 24 hours on credit card transactions in Europe?”), and the assistant will instantly return formatted visualizations, diagnostic breakdowns, and routing recommendations.

This interface is integrated directly into active team workspaces and communications channels like Slack, sending automated notifications when anomalies are detected.

3. Real-Time Anomaly Detection and Baseline Forecasting

Human analysts cannot manually monitor millions of transaction events for micro-shifts in processing performance.

Payments intelligence platforms resolve this by employing machine learning models that continuously scan transaction flows across more than 50 data dimensions. These systems evaluate the probability of transaction authorization based on a multi-dimensional feature vector:

where x is a feature vector containing variables like card brand, BIN country, issuer ID, transaction currency, time of day, and risk score, and w represents the model weights optimized across millions of historical payment events.

By comparing actual performance against predicted baselines, the anomaly detection engine identifies sudden temporal spikes (such as gateway-side timeouts) as well as gradual baseline drifts (where approval rates slowly degrade over several weeks).

When a deviation is flagged, the system estimates its financial impact in real terms (for example, identifying a 4% drop in Brazilian debit approvals costing $18,000 daily), allowing operations teams to act immediately.

4. Seamless Data Sharing and Warehouse Pipelines

To prevent transaction data from living in silos, the payments intelligence layer must integrate with downstream business environments.

By standardizing telemetry data across providers, the system pushes formatted transaction records directly to internal databases and data warehouses, featuring direct support for Snowflake integration.

This automated pipeline eliminates reporting discrepancies across departments and simplifies the ingestion of clean transaction data into internal ERP and BI environments.

5. Centralized Risk Monitoring and Pre-Chargeback Interception

A unified intelligence layer also serves to protect processing margins by centralizing dispute and risk management.

Through no-code integrations with early warning networks like Ethoca and Verifi (RDR/CDRN), the platform routes pre-chargeback alerts directly to a single dashboard.

This allows merchants to intercept disputes and issue refunds before formal chargebacks are filed, protecting their merchant processing history and avoiding network fines.

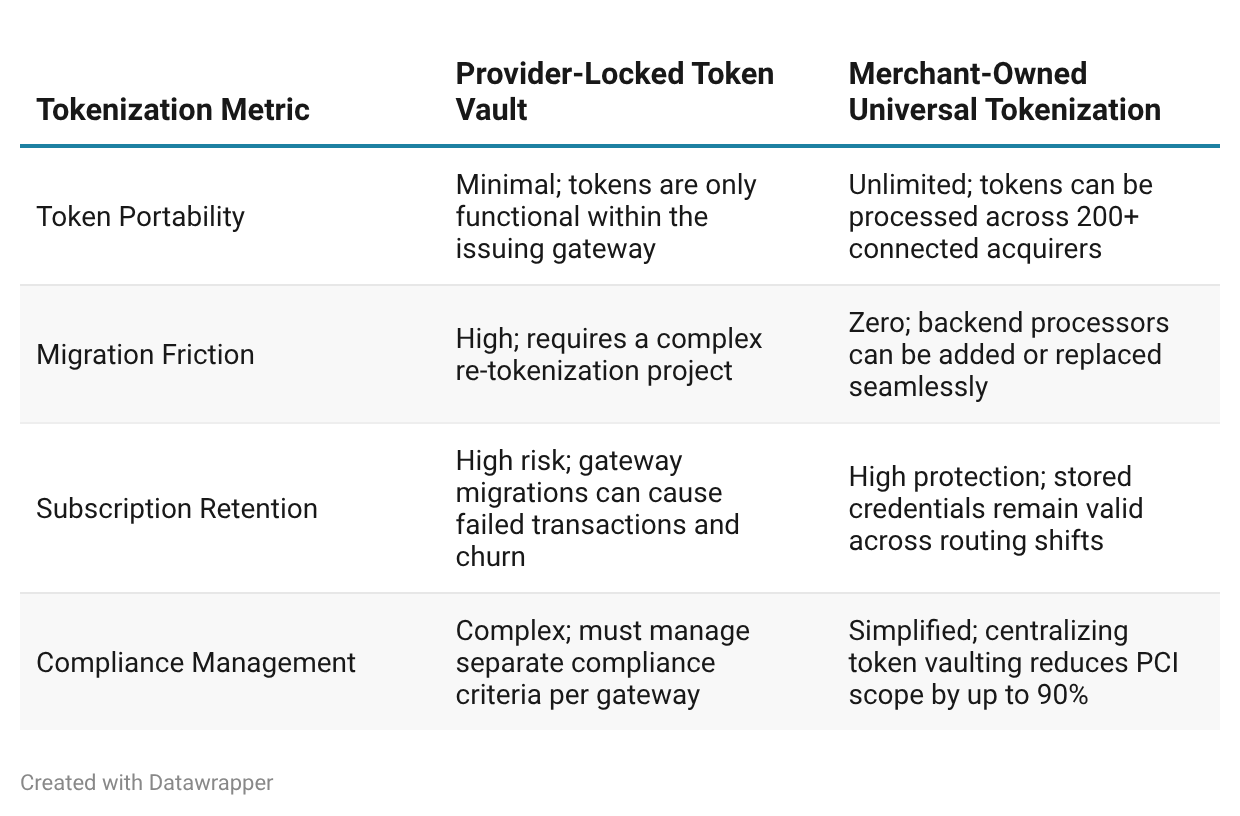

Merchant-owned tokenization and agnostic orchestration

A multi-PSP strategy cannot succeed without independent, merchant-owned tokenization. In a traditional gateway-locked setup, the processing provider generates proprietary payment tokens that are only functional within their own ecosystem.

This proprietary lock-in prevents the merchant from routing customer payment details to alternative gateways or acquirers, leaving them vulnerable to unilateral price increases and restricted geographic flexibility.

Decoupling tokenization from the processing layer resolves this architectural bottleneck. By storing card credentials in a secure, provider-agnostic token vault, merchants generate portable tokens that can be securely processed across any connected acquirer.

Once tokenization is centralized, payment orchestration platforms can optimize the entire transaction lifecycle:

Smart Routing Mechanics

Transactions are dynamically directed to the optimal processor based on real-time criteria like card brand, transaction value, geolocation, and risk scoring.

By routing transactions to localized regional acquirers, merchants consistently improve approval rates while minimizing cross-border processing fees.

Automatic Smart Retries (Fallback Routing)

If a primary payment provider experiences technical downtime or routes an unexpected decline, the smart routing engine automatically reroutes the transaction payload to a secondary processor.

This automatic fallback retry prevents checkout failures, protects transaction volume, and maintains high availability.

Load Balancing

Payment volumes can be distributed across multiple processors based on custom operational rules.

This load balancing optimizes processing commitments across vendor contracts, prevents merchants from exceeding transaction caps, and helps manage high-risk transaction volumes.

Post-Processing Reconciliation Engine

To simplify accounting workflows, the post-processing engine automatically retrieves and standardizes settlement statements across all connected gateways.

It compares this raw processor data with values in the internal transaction database, flags discrepancies (such as incorrectly calculated transaction fees or currency rounding errors), and exports formatted reconciliation logs directly to ERP systems like SAP or Microsoft Navision.

Trust orchestration in agentic commerce

The rapid development of autonomous systems is driving the next significant shift in payment processing. E-commerce is transitioning from standard, screen-based checkouts to machine-driven transaction execution.

In this agentic commerce landscape, AI-driven software agents act as autonomous delegators evaluating products, negotiating purchase terms, and completing checkouts on behalf of human users.

This evolution breaks the traditional four-party risk model (consumer, merchant, issuer, and acquirer), which was designed under the assumption of human-initiated transaction consent. When autonomous machines execute payments, merchants encounter unique technical and operational challenges:

1. Breakdown of Standard Fraud Detection

Traditional fraud prevention systems analyze human behavioral signals (such as mouse movements, browsing history, and device fingerprints) to verify transaction legitimacy.

Automated agent sessions, which are executed through virtual environments with automated metadata, mimic fraudulent patterns. According to an Accenture study, 78% of financial institution chief technology officers and payments heads expect fraud to increase significantly as agentic commerce scales, while 87% identify trust as the primary barrier to adoption.

2. Increased Dispute Exposure and Liability Shift

Without biometric human verification or standardized authentication patterns, proving transaction consent is difficult.

If a user claims their AI agent exceeded its spending limit or placed an incorrect order, the merchant bears the burden of proof. Without verified transaction trails, disputes can quickly lead to high chargeback rates.

3. High Protocol Fragmentation

As major technology ecosystems introduce proprietary transaction frameworks, payment platforms must remain protocol-agnostic.

Merchants need infrastructure capable of coordinating identity, intent, and value across competing AI protocols without building separate integrations for each system.

To manage these operational risks, tokenization must evolve from a security tool for card numbers into a programmable trust infrastructure.

Securing machine-driven transactions requires compiling multiple tokenized signals to establish a reliable transaction record:

Identity Tokens: Verify the specific AI agent, system, or machine initiating the transaction.

Intent Tokens: Preserve the user’s instructions (such as category constraints or maximum spending limits) directly within the transaction payload.

Consent Tokens: Store a signed digital record of the customer’s authorization of the purchase.

Payment Tokens: Represent the secure, portable account credentials used to execute the final transaction.

By combining these tokenized components, payment infrastructure can verify both payment details and authorization context, protecting the business against emerging chargeback risks.

This need for verifiable transaction context has led to industry initiatives like the Unified Trust Layer framework, co-developed by IXOPAY and Zip US. This open framework is designed to collect, evaluate, and route multidimensional trust signals across networks and protocols, preparing payment architectures for the requirements of automated commerce.

Strategic blueprint and executive recommendations

For fintech founders, product managers, and payments strategists, resolving the multi-PSP paradox requires implementing several key structural practices:

Consolidate Payment Telemetry

Deploy a provider-agnostic payments intelligence layer to unify transaction metadata across all active processors into a consistent schema.

Avoid relying on siloed gateway dashboards, and establish direct pipelines to downstream data platforms like Snowflake to support automated financial planning and operational oversight.

Establish Merchant Data Ownership

Separate token storage from the processing layer by utilizing a centralized, universal token vault.

This ensures complete portability of stored payment credentials, removes technical barriers to gateway migration, and reduces PCI compliance scope by up to 90%.

Deploy Automated Diagnostics

Implement machine learning-driven anomaly detection alongside automated pre-chargeback interception networks.

Configure custom alerts to monitor core performance metrics such as transaction approval rates, routing latency, and fee variances to resolve processing errors before they impact overall revenue.

Transition Payment Flows to Support Trust Architecture

Design the transaction environment to support programmable token structures that can capture identity, intent, and consent metadata alongside traditional card credentials.

Preparing the payment stack to verify and record machine-initiated checkouts will help secure transaction volume as agent-driven commerce scales.

Disclaimer:

Fintech Wrap Up aggregates publicly available information for informational purposes only. Portions of the content may be reproduced verbatim from the original source, and full credit is provided with a “Source: [Name]” attribution. All copyrights and trademarks remain the property of their respective owners. Fintech Wrap Up does not guarantee the accuracy, completeness, or reliability of the aggregated content; these are the responsibility of the original source providers. Links to the original sources may not always be included. AI is used to produce some pieces of this article. For questions or concerns, please contact us at sam.boboev@fintechwrapup.com.