Deep Dive: Programmable Payments Are Here: Building With Coinbase’s Commerce Protocol

So what exactly is this Commerce Payments Protocol?

Coinbase and Shopify have teamed up to launch the Commerce Payments Protocol, an open onchain payments standard designed for real-world commerce. Announced in mid-2025, this protocol brings sophisticated multi-step payment flows (think escrow, authorizations, captures, refunds) onto the blockchain, while preserving crypto’s core benefits of speed, low cost, and global reach. In plain terms, it bridges the promise of crypto with the nitty-gritty realities of everyday commerce. The protocol is live on Coinbase’s Base network and open-source for all developers. It’s already powering Shopify’s new USDC payment option, rolling out to millions of Shopify merchants worldwide who can now seamlessly accept stablecoin payments on Base. This marks one of the first large-scale rollouts of crypto payments in mainstream online retail – without users needing to wrestle with volatility or clunky crypto addresses.

So what exactly is this Commerce Payments Protocol? At its core, it’s a set of smart contracts and APIs that replicate the “authorize, then capture” dance of traditional payment networks, but onchain. Coinbase Commerce (Coinbase’s merchant payments arm) has rebuilt its checkout on top of this protocol, making onchain payments more plug-and-play. The protocol is open-source, so any payment provider or platform can integrate it or even run their own instance. (Yes, Coinbase wants this to be a standard, not just their proprietary sauce.) By leveraging Base – Coinbase’s Ethereum L2 – the protocol promises near-instant settlement (we’re talking sub-second, ~200ms in optimal cases) with transaction fees around a penny. And because it’s crypto, it works 24/7, across borders, no bank middlemen required. In short, Coinbase and Shopify just opened the door for stablecoins (like USDC) to move from crypto niche to everyday e-commerce.

Why does this matter?

If you’ve been around the fintech block, you know crypto payments in theory have always been touted as faster, cheaper, and more global than card networks. Stablecoins alone hit $30 trillion in settlements last year – growing 3× year-over-year – showing huge demand for moving value onchain. But in practice, using crypto at the online checkout has been clunky at best. Aside from the famous Bitcoin pizza (15 years ago someone paid 10,000 BTC for two Papa John’s pizzas), crypto commerce hasn’t evolved much beyond one-off novelties. Why? Because buying a latte with crypto exposed you to price swings, manual address entry, and “Did I send the right amount?” anxiety. Traditional online payments have decades of tooling to handle things like holds, partial captures, refunds, fraud checks – whereas crypto payments until now were basically “send coin, hope it works out.” That’s a non-starter for large-scale commerce.

Enter the Commerce Payments Protocol. Coinbase’s solution essentially mimics the credit card payment flow onchain. In traditional finance, when you pay online, there’s often an authorization hold (funds reserved on your card) and later a capture (merchant actually takes the money) once the item is shipped. This two-step dance gives merchants and buyers flexibility – you can cancel an order before it ships, adjust for out-of-stock items, etc., and merchants only get charged fees on settled transactions. Until now, crypto lacked this nuance. The new protocol brings that same authorize-and-capture model to crypto payments, using smart contracts as the adjudicator.

How does it work?

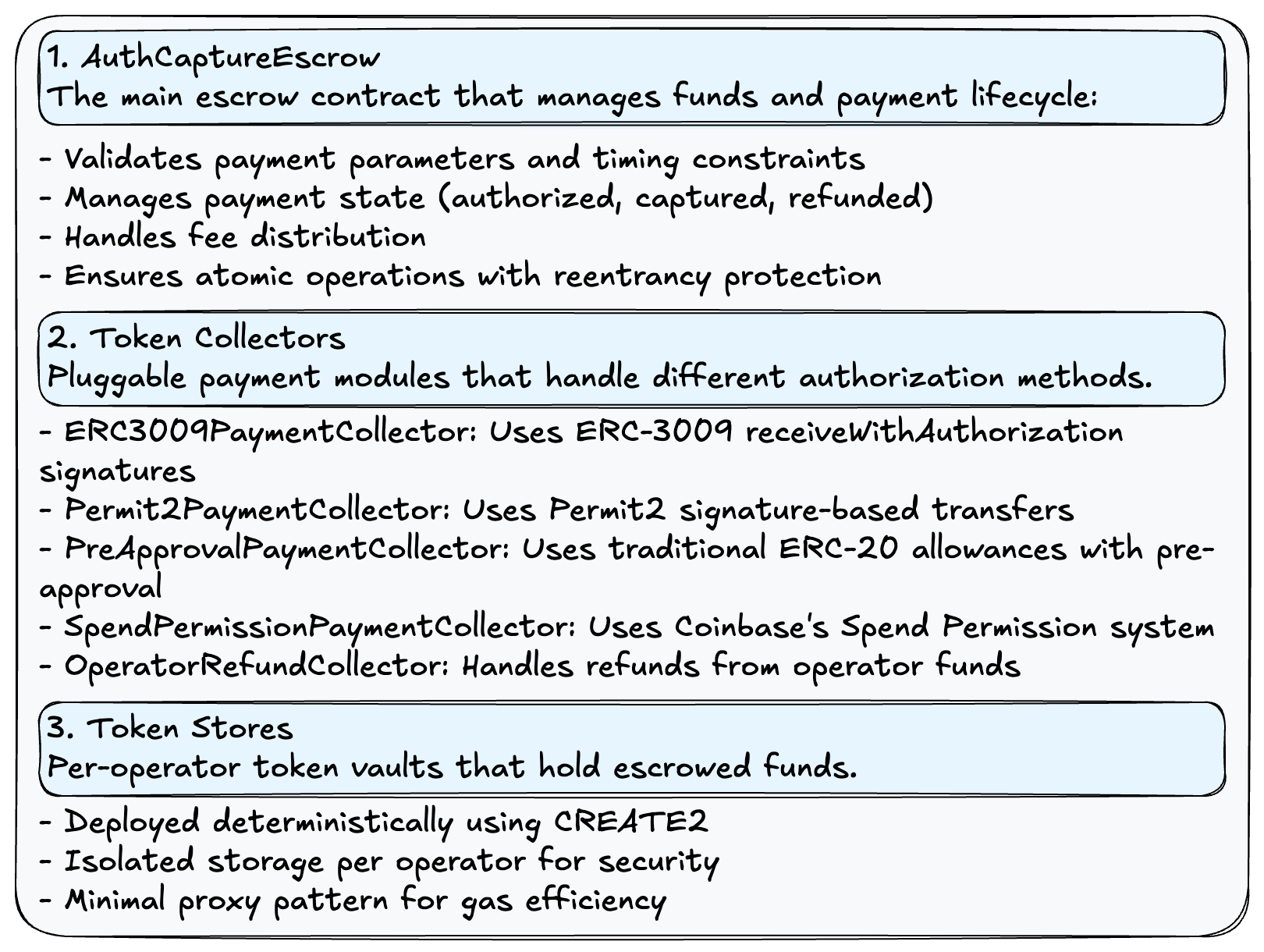

The protocol introduces a non-custodial escrow contract that sits between the customer (payer) and merchant (receiver). When a buyer initiates a purchase, instead of immediately transferring tokens to the merchant, the buyer first signs a payment intent – basically a structured message saying “I agree to pay X amount of USDC to merchant Y, using token Z from my wallet, before time T.” This signed intent is sent to an Operator service (more on that in a second), which then moves the funds into the escrow contract onchain (that’s the authorize step). The money is now held securely in the smart contract, on behalf of the merchant. The merchant can later trigger a capture to finalize the sale – which moves the USDC (or whatever the merchant opted to receive) from escrow to the merchant’s wallet. If something goes wrong or the order is canceled, the merchant (or even the buyer in some cases) can void the payment, releasing the funds back to the buyer from escrow instead.

Keep reading with a 7-day free trial

Subscribe to Fintech Wrap Up to keep reading this post and get 7 days of free access to the full post archives.