Deep Dive: How Bank of America Built a $40B Consumer Banking Machine

Bank of America’s consumer banking division is a massive, integrated machine that produces over $41 billion in annual revenue and $10.8 billion in net profit as of 2024, accounting for roughly 37% of the bank’s revenue. This operation spans everything from basic checking accounts and credit cards to digital platforms and wealth management tie-ins. What follows is a first-principles breakdown of how BofA’s consumer banking model works end-to-end, from gathering deposits and making loans to the technology stack, loyalty mechanics, and distribution strategy that bind it all together. We’ll also compare Bank of America’s approach to peers like JPMorgan Chase and Citibank, and tease out hidden fragilities and lessons for fintech operators and banking strategists.

Deposits: Low-Cost Funding Engine

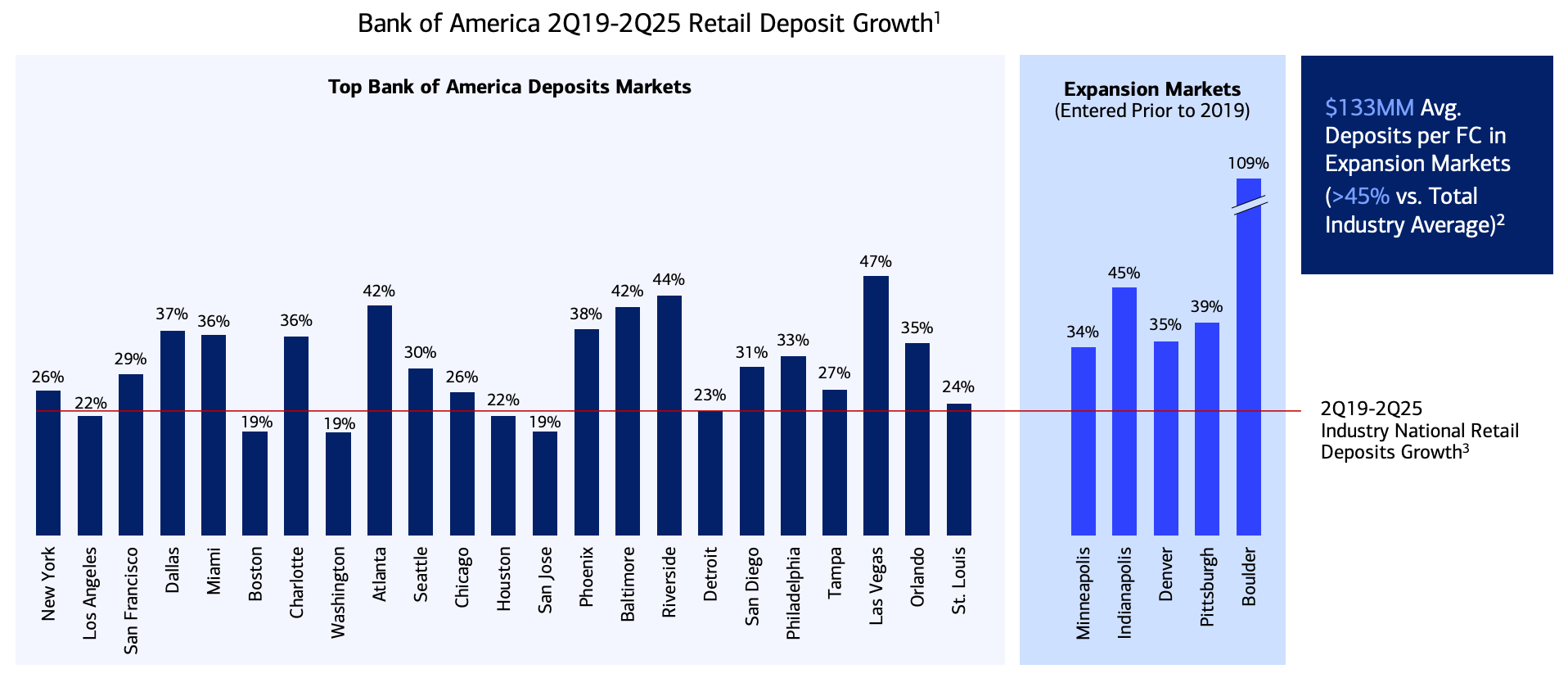

At the core of BofA’s consumer model is a gigantic base of deposits of nearly $949 billion in consumer deposits. These deposits are the lifeblood of the bank’s lending and investment activities, providing a stable, low-cost funding source. Bank of America claims to be the #1 U.S. bank in consumer deposit market share, edging out even JPMorgan in pure retail deposit rankings. This leadership comes from sheer scale (over 70 million consumer clients, by BofA’s count) and an emphasis on primary checking accounts. A huge proportion of BofA’s deposits sit in low or no-interest checking, a strategic advantage in terms of funding cost. In fact, the bank’s internal metrics show that a majority of consumer deposit balances pay minimal interest, which keeps the cost of deposits extremely low. This cheap funding was on full display in the recent rising rate environment: even as the Federal Funds rate climbed, Bank of America’s interest paid to retail depositors hardly budged, widening the spread it earns on those funds.

However, this strength comes with a caveat. Customer inertia is the linchpin many depositors sticking around despite higher yields advertised elsewhere, thanks to convenience and habit. If that inertia falters (say, in a prolonged high-rate scenario or due to aggressive fintech alternatives), BofA could face outflows or pressure to raise deposit rates. We already see hints of this in the numbers: consumer deposits grew only 1% year-on-year, while clients shifted more money into higher-yield investments (17% YoY growth in consumer investment assets). The lesson is that BofA’s deposit franchise is a well-oiled engine, but one that relies on maintaining primacy and trust. Peer contrast: Citi, by comparison, has a far smaller U.S. deposit franchise after scaling back branches, and relies more on rate-sensitive funding (e.g., brokerage CDs or higher-yield savings to attract customers). Fintech challengers like Neo-banks often tempt users with high APY promotions, but they lack the breadth of relationship and convenience that BofA uses to keep deposits “sticky.” In short, low-cost deposits are BofA’s moat, a structural advantage that fintech upstarts and even most big peers can’t easily replicate, but it must be defended by deep customer relationships to avoid becoming a source of fragility.

Lending: Credit Cards and Prudent Credit Portfolio

BofA channels its deposit base into a broad consumer lending portfolio of $322 billion, spanning credit cards, mortgages, auto loans, home equity lines, and small business credit. The jewel in the crown is credit cards, a high-yield lending business where BofA is a top player (though not #1). The bank has 39 million active credit card

Keep reading with a 7-day free trial

Subscribe to Fintech Wrap Up to keep reading this post and get 7 days of free access to the full post archives.