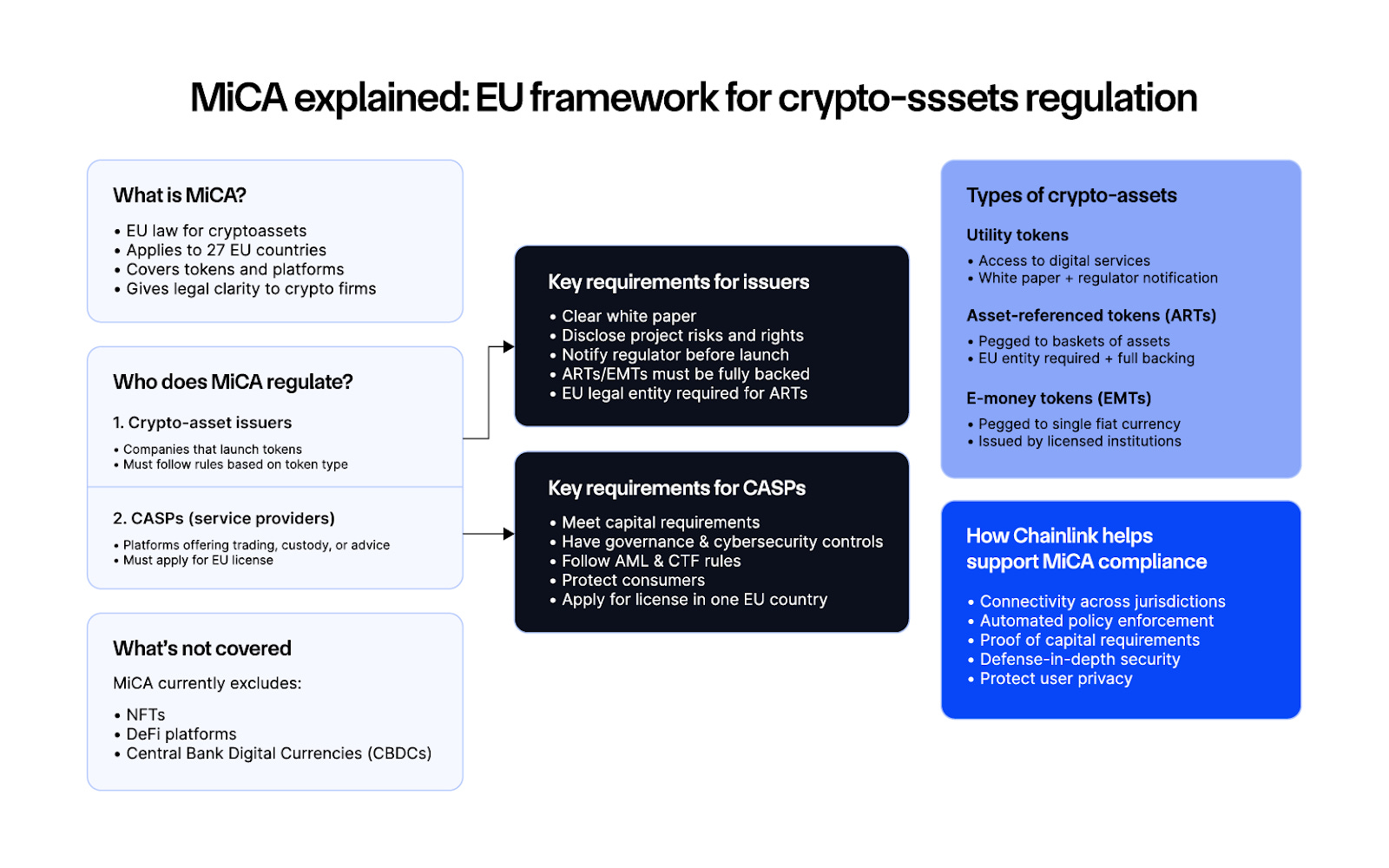

Deep Dive: A Definitive Strategic Guide to MiCA Compliance and Institutional Market Architecture

The transitional grandfathering window under Article 143(3) of the Markets in Crypto-Assets Regulation (MiCA) has officially expired across all 27 European Union (EU) and 30 European Economic Area (EEA) member states. This milestone marks the definitive end of the highly fragmented national Virtual Asset Service Provider (VASP) registries and establishes a single, harmonized authorization framework for Crypto-Asset Service Providers (CASPs). For fintech founders, payments strategists, and venture capitalists, this shift represents a hard boundary: any entity providing crypto-asset services to EU clients without full MiCA authorization is now operating in direct breach of EU law.

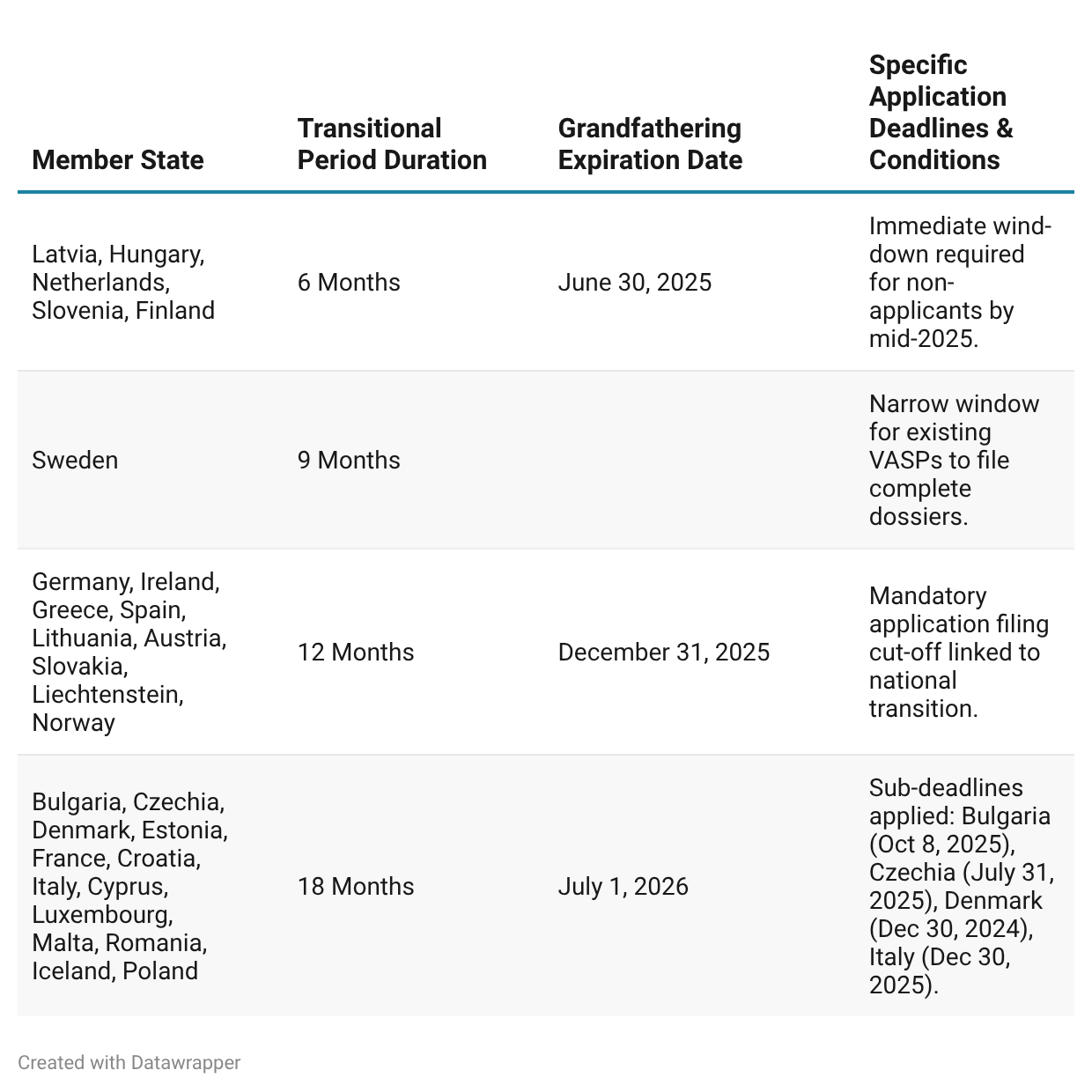

Prior to this enforcement milestone, the European digital asset landscape resembled a patchwork of disparate national standards. Member states exercised discretion over the duration and terms of their transitional timelines, leading to non-uniform grandfathering periods across the continent. While jurisdictions such as France, Malta, and Luxembourg elected the maximum 18-month transitional window expiring on July 1, 2026, others enforced significantly tighter timelines.

This chronological asymmetry created severe cross-border compliance mismatches. Entities passporting services from a jurisdiction with a longer transitional window into a state where the window had already closed found themselves in immediate technical breach, resulting in localized enforcement actions and platform geofencing. The regulatory consequences of operating without authorization are severe. Under MiCA Article 111, National Competent Authorities (NCAs) are empowered to levy administrative fines of up to €5 million or up to 12.5% of total annual turnover for legal entities. In tandem, regulators are executing mandatory wind-down protocols. Unauthorized platforms must immediately halt new user onboarding, cease all marketing and customer solicitation, and restrict their operational interfaces exclusively to asset liquidations, transfers, and account closures.

The transition has exposed a vast compliance deficit. Out of more than 1,200 legacy VASP entities registered nationally before MiCA, only approximately 200 to 213 platforms successfully transitioned to full CASP status by the close of the grandfathering window a successful conversion rate of less than 18%. This structural contraction is re-routing the competitive dynamics of the entire European fintech sector, separating fully compliant market players from those forced to execute orderly exits.

For clients and counterparties, remaining on unauthorized platforms introduces significant operational and financial risks. Unlicensed entities provide no guaranteed asset segregation, leaving customer funds vulnerable to pooling and loss within a bankruptcy estate. Clients face sudden asset freezes, withdrawal delays, and localized tax or legal complications as regulators coordinate cross-border enforcement. To mitigate these exposures, corporate treasurers and institutional allocators are actively auditing their transaction counterparty chains, verifying entries against the European Securities and Markets Authority (ESMA) register to ensure seamless liquidity routing.

Technical architecture for the unified European market

For digital asset development teams, payments strategists, and software engineers, compliance is no longer a localized legal review; it is a system-level architectural requirement. In the EU, MiCA does not operate in isolation but is tightly integrated with the recast Transfer of Funds Regulation (TFR - Regulation 2023/1113) and the Digital Operational Resilience Act (DORA - Regulation 2022/2554).

Keep reading with a 7-day free trial

Subscribe to Fintech Wrap Up to keep reading this post and get 7 days of free access to the full post archives.